Marubeni (TSE:8002) shares have held steady recently as investors look for cues on the direction of Japan’s trading houses in an evolving global market. The stock’s performance has sparked discussion on valuation compared to peers.

Marubeni’s share price has surged over 70% year-to-date, with recent momentum evident in strong short-term returns. Its one-year total shareholder return of nearly 84% highlights growing confidence in the group's long-term prospects amid changing global dynamics.

With such a remarkable run-up in Marubeni’s share price, investors are now weighing whether the stock remains undervalued or if recent gains mean future growth is already fully reflected in the price.

Advertisement

Price-to-Earnings of 11.7x: Is it justified?

Marubeni shares trade at a price-to-earnings (P/E) ratio of 11.7x, positioning them as more attractively valued than the average stock in the Japanese market and among peer companies.

The P/E ratio measures what investors are willing to pay for each yen of the company’s earnings. In trading houses like Marubeni, a low multiple can indicate that the market is not fully pricing in future earnings potential or sees risks in the business outlook.

Compared to the peer average P/E of 14.1x, Marubeni looks inexpensive. This suggests investors could view it as undervalued relative to its direct competitors. Its P/E is also well below the estimated fair price-to-earnings ratio of 21x, which may indicate room for a market re-rating if profit fundamentals remain strong.

However, global economic uncertainty and slowing revenue growth could quickly challenge the optimistic outlook reflected in Marubeni’s recent share price gains.

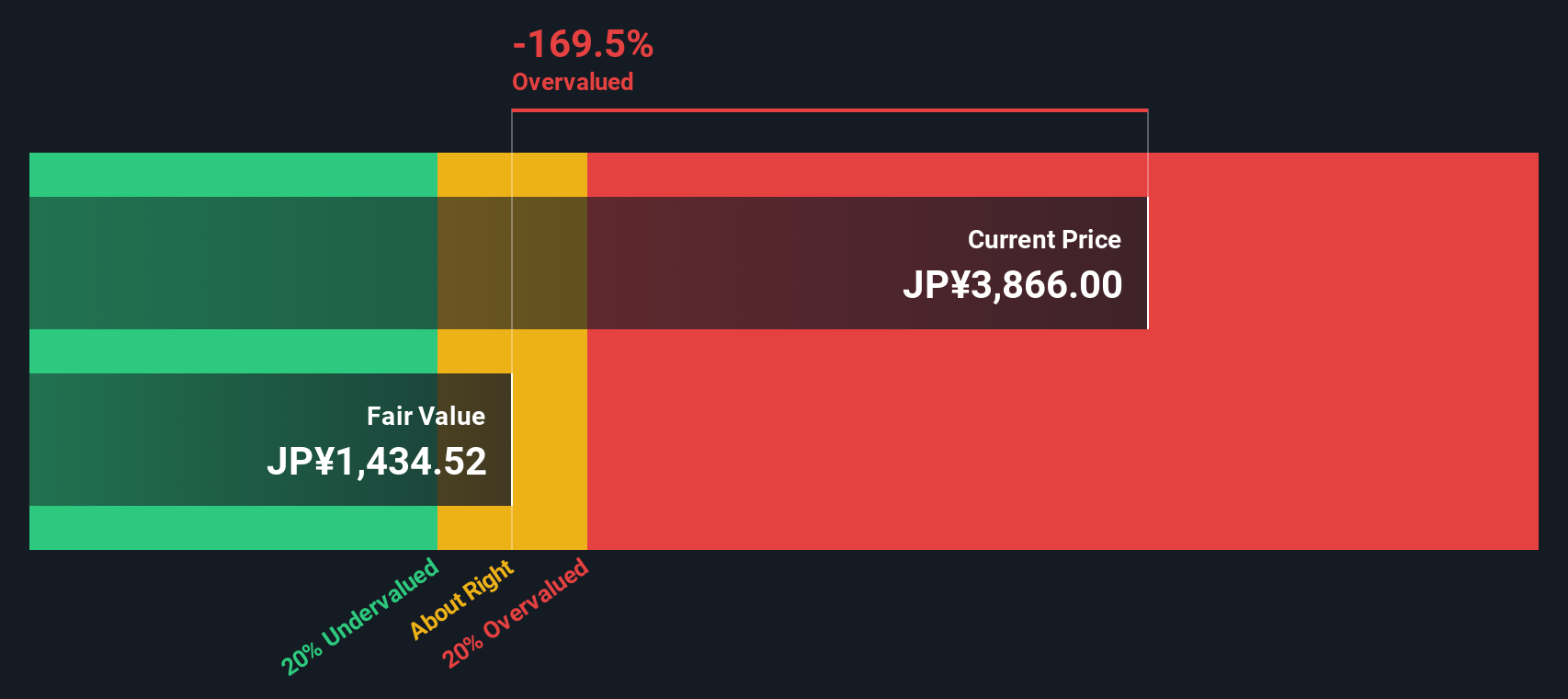

Another View: SWS DCF Model Suggests Overvaluation

While Marubeni’s earnings multiple points to a bargain, the SWS DCF model presents a different perspective. According to this method, Marubeni is trading above its estimated fair value, which challenges the notion that the stock is truly undervalued. Could the market be pricing in too much optimism?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Marubeni for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 927 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Marubeni Narrative

If you have your own take on Marubeni or want to run the numbers yourself, creating a custom view takes just a few minutes here: Do it your way

Make your next move count by using the Simply Wall Street Screener to target emerging opportunities and strong market trends before others catch on.

Capture steady income growth by tapping into these 15 dividend stocks with yields > 3%, which offers yields over 3 percent and features resilient financials in today’s volatile market.

Spot early movers in the quantum computing revolution by tracking these 27 quantum computing stocks, which is making breakthroughs in technology and innovation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks