Advertisement

NSK (TSE:6471) Valuation in Focus After Guidance Upgrade and Subsidiary Consolidation Boost

Simply Wall St

Reviewed by Simply Wall St

NSK (TSE:6471) raised its full-year sales and profit outlook after reporting stronger automotive production, increased demand in China, tighter cost management, and currency tailwinds. The consolidation of NSK Steering & Control Co. also boosted reported earnings.

See our latest analysis for NSK.

NSK’s share price has surged recently, posting a remarkable 20% return over the past month and an impressive 35.9% gain year-to-date, as investors responded positively to robust guidance upgrades and successful integration of new businesses. With a one-year total shareholder return of 42%, momentum appears to be building around the company’s growth and profitability story.

If you’re interested in what’s driving other automakers, this is an ideal moment to explore See the full list for free.

With shares already up sharply this year, investors now face a crucial question: is the recent surge simply catching up with fundamentals, or has the market already factored in all of NSK’s future growth potential?Most Popular Narrative: 20.8% Overvalued

NSK’s latest narrative price target stands at ¥758.33, which is notably below its last close of ¥915.9. This makes the current premium hard to ignore. The detailed narrative examines structural reform, industrial expansion, and digital initiatives that are meant to support this value call.

Structural reforms, including downsizing and restructuring production in Europe and Japan and exiting some non-core businesses, are projected to lead to a ¥9 billion improvement in profitability by 2026, positively impacting net margins.

Want to know what fuels this bold view? The narrative is built around a transformation roadmap with aggressive profit targets and ambitious margin improvement strategies. Curious about the actual growth and profitability assumptions at the heart of this pricing model? Dive deeper to uncover the unknowns driving this valuation.

Result: Fair Value of ¥758.33 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, weaker automotive output and lingering demand uncertainty in key regions could unexpectedly dampen NSK’s impressive earnings trajectory and challenge current growth assumptions.

Find out about the key risks to this NSK narrative.

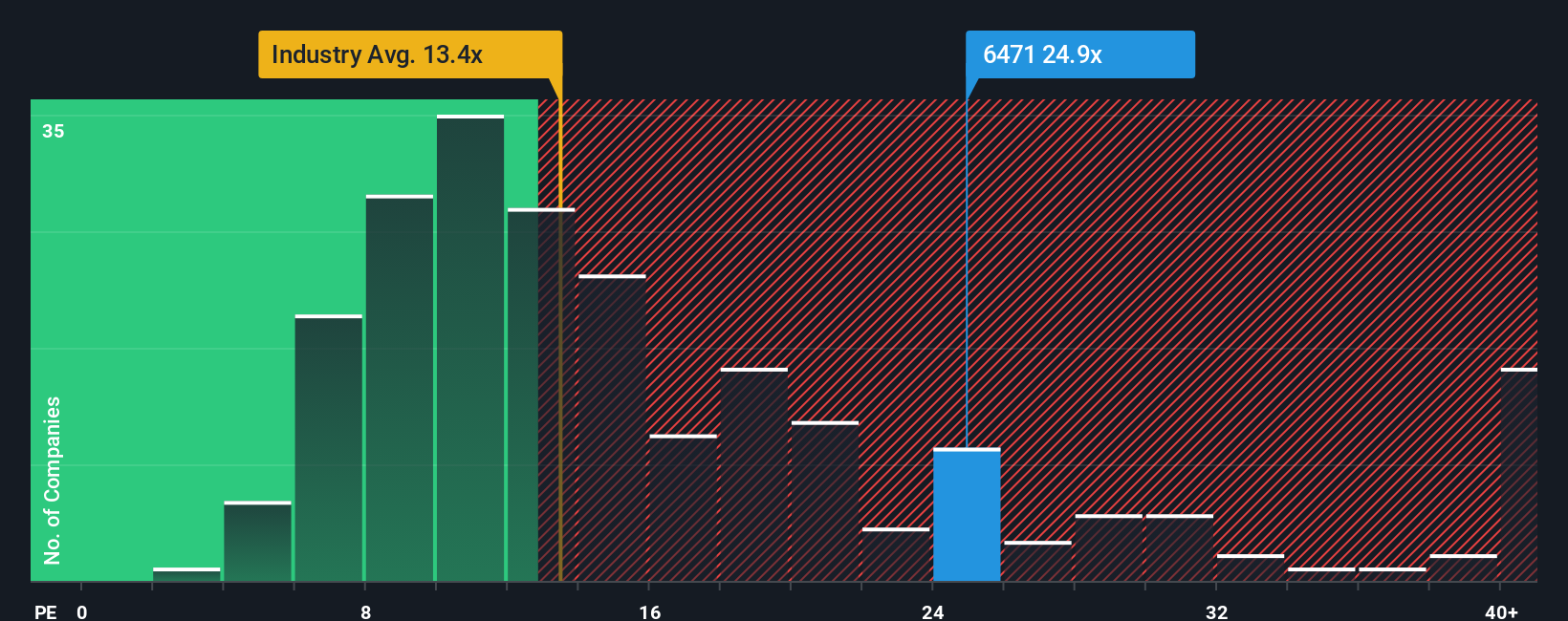

Another View: What Do Earnings Multiples Say?

Looking at earnings-based valuation, NSK trades at 24.9 times earnings, which is much higher than its peers at 66.9 times, but also above what is considered a fair ratio for the business, set at 20 times. This gap signals that while the stock looks like a bargain next to competitors, investors may face downside if the market shifts toward the lower fair ratio. How much weight should you give to this method when balancing risk and opportunity?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own NSK Narrative

If you find yourself seeing the story differently or want to dive into the numbers yourself, creating your own take takes just a few minutes. Do it your way

A great starting point for your NSK research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Smart Investment Ideas?

You’re not limited to just one opportunity. Make your next investing decision with confidence by checking out high-potential stocks selected for different strategies below.

- Boost your portfolio’s yield by tapping into these 16 dividend stocks with yields > 3%, known for reliable payouts above 3% and consistent shareholder rewards.

- Jump on the AI momentum and benefit from rapid innovation by exploring these 24 AI penny stocks, featuring companies at the forefront of artificial intelligence breakthroughs.

- Secure opportunities trading below their worth and maximize future returns with these 863 undervalued stocks based on cash flows, based on rigorous cash flow analytics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if NSK might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:6471

NSK

Manufactures and sells industrial machinery bearings, automotive products, and precision machinery and parts worldwide.

Flawless balance sheet with solid track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|66.7% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|4.8% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.5% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$26.69|18.6% undervalued

BE

Community Contributor