Advertisement

DMG Mori Completes Share Buyback Might Change the Case for Investing in DMG Mori (TSE:6141)

Simply Wall St

Reviewed by Sasha Jovanovic

- Between October 30 and November 13, 2025, DMG Mori completed the repurchase of 2,500,000 shares, representing 1.76% of its outstanding shares, for ¥6,626.97 million as part of a previously announced buyback program.

- This move highlights management’s willingness to allocate capital toward returning value to shareholders, a decision that often garners positive attention from investors.

- We’ll explore how the completion of this buyback reflects DMG Mori’s approach to capital allocation and its impact on the investment case.

The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

What Is DMG Mori's Investment Narrative?

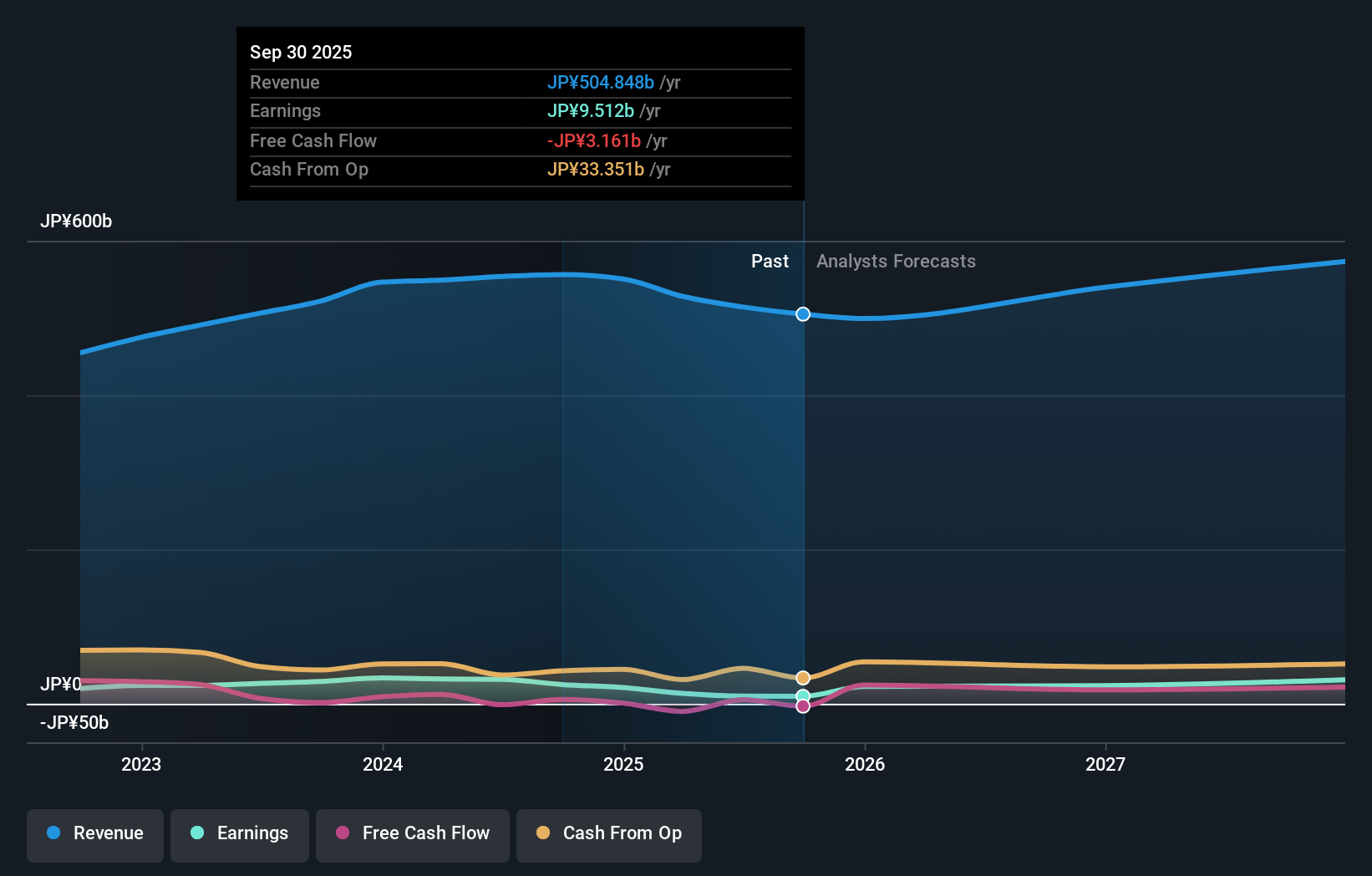

To be a shareholder in DMG Mori, I’d want conviction in the business’s ability to balance steady growth with disciplined capital management. After a turbulent few months for the share price, the completed buyback signals management’s commitment to shareholder returns, but it doesn’t fundamentally change the most pressing short-term catalysts or risks. Earnings forecasts still call for moderate revenue expansion and strong profit growth, but with a high price-to-earnings ratio and relatively low margins compared to peers, the stock remains sensitive to sentiment shifts and earnings surprises. Meanwhile, the machinery sector’s muted outlook and DMG Mori’s weaker return on equity keep business execution and cost control firmly in focus. The buyback adds support, but doesn’t remove the need to monitor profitability risks, cash flow coverage for dividends, and ongoing earnings volatility. However, the high price-to-earnings ratio remains a key risk investors should not ignore.

DMG Mori's shares have been on the rise but are still potentially undervalued by 30%. Find out what it's worth.Exploring Other Perspectives

Explore 2 other fair value estimates on DMG Mori - why the stock might be worth 35% less than the current price!

Build Your Own DMG Mori Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your DMG Mori research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free DMG Mori research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate DMG Mori's overall financial health at a glance.

Interested In Other Possibilities?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Find companies with promising cash flow potential yet trading below their fair value.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 35 best rare earth metal stocks of the very few that mine this essential strategic resource.

- These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:6141

Excellent balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

JO

JohnJ on Worldline ·

No miracle in sight

Fair Value:€7.0178.0% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k2.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

79 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

90 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

927 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative