Advertisement

TOTO (TSE:5332): Evaluating Valuation Following Recent Share Price Momentum

Simply Wall St

Reviewed by Simply Wall St

TOTO (TSE:5332) has shown steady performance lately, and investors may be curious about how recent trends could impact the company's stock. With its long-standing presence in bathroom and kitchen fixtures, the stock's progress remains a point of interest.

See our latest analysis for TOTO.

TOTO's shares have quietly rebounded, with a 9.4% year-to-date share price return suggesting renewed optimism among investors. Meanwhile, the 1-year total shareholder return of 3.9% reflects a more measured long-term climb. Momentum appears to be building this year as the stock outpaces its recent performance history.

If you're curious about what other established names might be trending in manufacturing, it's a great moment to broaden your search and discover See the full list for free.

The key question now is whether TOTO’s current momentum signals an undervalued opportunity for investors, or if the market is already fully reflecting its future growth potential in the stock price.

Price-to-Sales Ratio of 0.9x: Is it justified?

TOTO is currently trading at a price-to-sales ratio of 0.9x, which is higher than the JP Building industry average of 0.5x. This suggests the market is placing a premium on TOTO compared to its sector peers, despite recent share price momentum.

The price-to-sales (P/S) ratio measures how much investors are paying for each unit of sales. For companies like TOTO, which operate in manufacturing with relatively stable revenues, the P/S ratio can reveal whether a stock is seen as a growth leader, a steady performer, or valued mainly for its assets.

At 0.9x, TOTO's P/S multiple is not only higher than the industry average, but also stands out when compared to the peer average of 1.9x. Interestingly, this multiple is below the estimated fair price-to-sales ratio of 1.6x. This level is one the market could eventually move toward if growth expectations are met or exceeded. This provides context for investors weighing whether the premium is warranted, especially if future growth or margin improvements materialize.

Explore the SWS fair ratio for TOTO

Result: Price-to-Sales of 0.9x (ABOUT RIGHT)

However, slowing revenue growth or a pullback in net income gains could weigh on sentiment and challenge the current momentum in TOTO shares.

Find out about the key risks to this TOTO narrative.

Another View: What Does the SWS DCF Model Suggest?

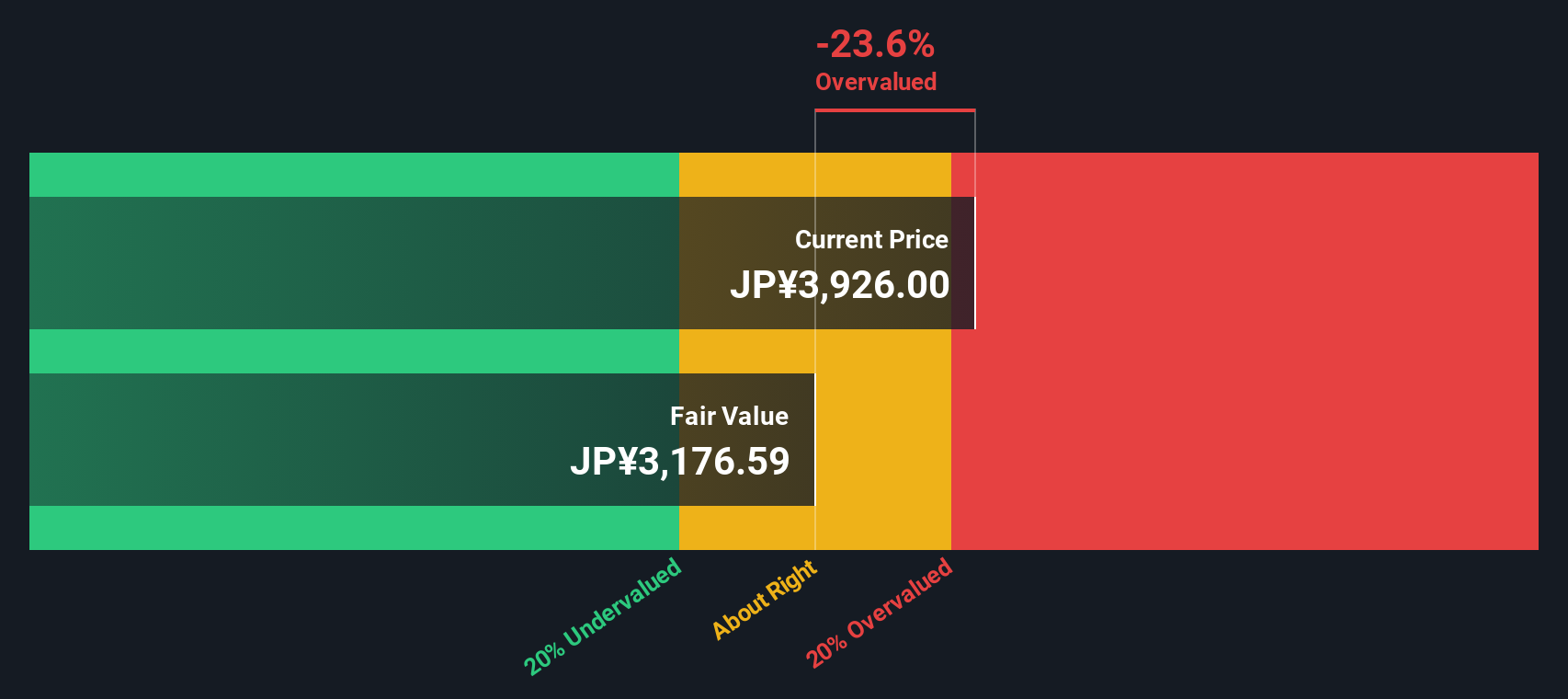

Looking at TOTO from a different angle, the SWS DCF model estimates the company’s fair value at ¥3,509, while shares currently trade at ¥4,084. This suggests the stock may be overvalued, although the price-to-sales ratio points to reasonable value. Could this gap signal downside risk, or is the market pricing in future optimism?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out TOTO for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 920 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own TOTO Narrative

If you think a different perspective is worth exploring or want to dive into your own research, you can draft your own narrative in just a few minutes: Do it your way

A great starting point for your TOTO research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Don't limit your strategy to just one stock. Smart investors stay ahead by tapping into new trends and hidden gems before they heat up. Here’s a shortcut to more market-shaping opportunities:

- Capitalize on early-stage growth by checking out these 3573 penny stocks with strong financials gaining momentum among savvy investors.

- Unlock future potential with these 15 dividend stocks with yields > 3% that offer reliable income streams and financial resilience in any market environment.

- Position yourself for the next wave of innovation by scanning these 81 cryptocurrency and blockchain stocks transforming the digital finance landscape.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if TOTO might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:5332

TOTO

Manufactures and sells bathroom and kitchen plumbing fixtures worldwide.

Flawless balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7924.0% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative