Advertisement

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Taisei Oncho Co., Ltd. (TSE:1904) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first step when considering a company's debt levels is to consider its cash and debt together.

What Is Taisei Oncho's Net Debt?

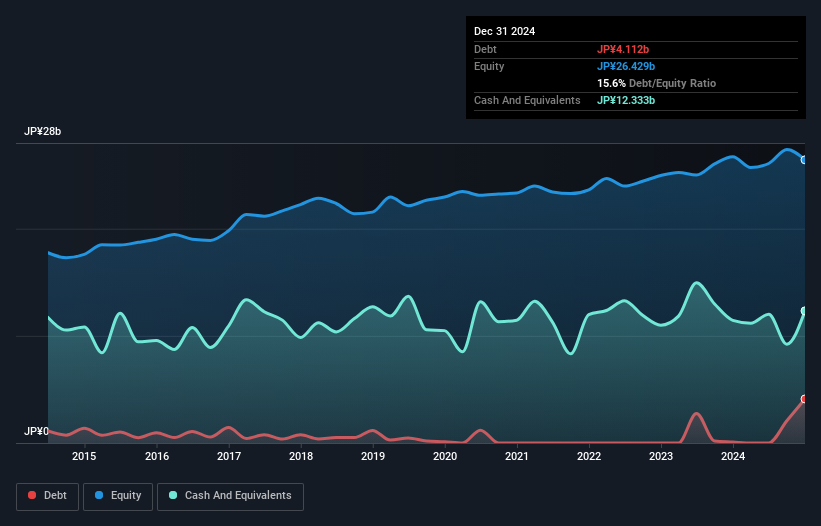

You can click the graphic below for the historical numbers, but it shows that as of December 2024 Taisei Oncho had JP¥4.11b of debt, an increase on JP¥90.0m, over one year. But on the other hand it also has JP¥12.3b in cash, leading to a JP¥8.22b net cash position.

How Healthy Is Taisei Oncho's Balance Sheet?

The latest balance sheet data shows that Taisei Oncho had liabilities of JP¥17.3b due within a year, and liabilities of JP¥546.0m falling due after that. Offsetting this, it had JP¥12.3b in cash and JP¥16.1b in receivables that were due within 12 months. So it actually has JP¥10.5b more liquid assets than total liabilities.

This luscious liquidity implies that Taisei Oncho's balance sheet is sturdy like a giant sequoia tree. On this view, lenders should feel as safe as the beloved of a black-belt karate master. Simply put, the fact that Taisei Oncho has more cash than debt is arguably a good indication that it can manage its debt safely.

See our latest analysis for Taisei Oncho

In addition to that, we're happy to report that Taisei Oncho has boosted its EBIT by 37%, thus reducing the spectre of future debt repayments. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Taisei Oncho will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend .

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. While Taisei Oncho has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. In the last three years, Taisei Oncho created free cash flow amounting to 9.0% of its EBIT, an uninspiring performance. For us, cash conversion that low sparks a little paranoia about is ability to extinguish debt.

Summing Up

While it is always sensible to investigate a company's debt, in this case Taisei Oncho has JP¥8.22b in net cash and a decent-looking balance sheet. And we liked the look of last year's 37% year-on-year EBIT growth. So we don't think Taisei Oncho's use of debt is risky. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. For instance, we've identified 1 warning sign for Taisei Oncho that you should be aware of.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Valuation is complex, but we're here to simplify it.

Discover if Taisei Oncho might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:1904

Taisei Oncho

Engages in the design and construction of air conditioning, water supply/drainage sanitary, and electrical equipment systems in Japan.

Solid track record with excellent balance sheet and pays a dividend.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|31.9% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|22.1% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|36.0% overvalued

DA

Community Contributor