Advertisement

- Japan

- /

- Construction

- /

- TSE:1860

Toda Corporation (TSE:1860): Examining Valuation After Upgraded Outlook and Dividend Increase

Simply Wall St

Reviewed by Simply Wall St

Toda (TSE:1860) just raised its full-year earnings outlook, citing stronger margins in domestic construction, increased profits from real estate sales, and successful divestments. The company also raised its interim dividend, reflecting greater confidence in its outlook.

See our latest analysis for Toda.

Toda’s upbeat guidance and dividend hike have caught investors’ attention, with the stock jumping 10.6% over the past month and notching a 25.8% share price return year-to-date. Combining these moves, the company’s one-year total shareholder return stands at a strong 30.7%, and its five-year total return is an impressive 124%. These are clear signs that investor optimism is building as management delivers on profitability and balance sheet improvements.

If positive momentum like Toda’s has you wondering what else could surprise, this is an ideal time to broaden your horizons and discover fast growing stocks with high insider ownership

Yet with the share price surging and forecasts upgraded, investors may wonder if Toda’s value is still ahead of fundamentals or if the market has already priced in its future growth, leaving little room for a bargain opportunity.

Price-to-Earnings of 11.7x: Is it justified?

Toda trades at a price-to-earnings (P/E) ratio of 11.7x, putting it just below industry peers and the broader market. This suggests some value relative to the sector standard.

The price-to-earnings ratio compares a company's current share price to its per-share earnings, giving investors a sense of what they are paying for each yen of profit. For construction firms like Toda, the P/E is a practical tool for evaluating profitability against similar businesses. It may reveal whether the market is forecasting further earnings growth or pricing in headwinds.

Looking deeper, Toda’s P/E ratio is almost identical to the Japanese construction industry average (11.8x). This indicates investors are valuing its earnings in line with sector norms. Against the peer group average (16.5x), Toda looks even cheaper. However, compared to the estimated “fair” P/E based on financial modeling (11.6x), Toda sits right above that threshold. This suggests limited margin for further outperformance unless the company’s trends improve.

Explore the SWS fair ratio for Toda

Result: Price-to-Earnings of 11.7x (ABOUT RIGHT)

However, risks remain as annual net income has dipped and shares now trade just above fair value, which leaves little room for further disappointment.

Find out about the key risks to this Toda narrative.

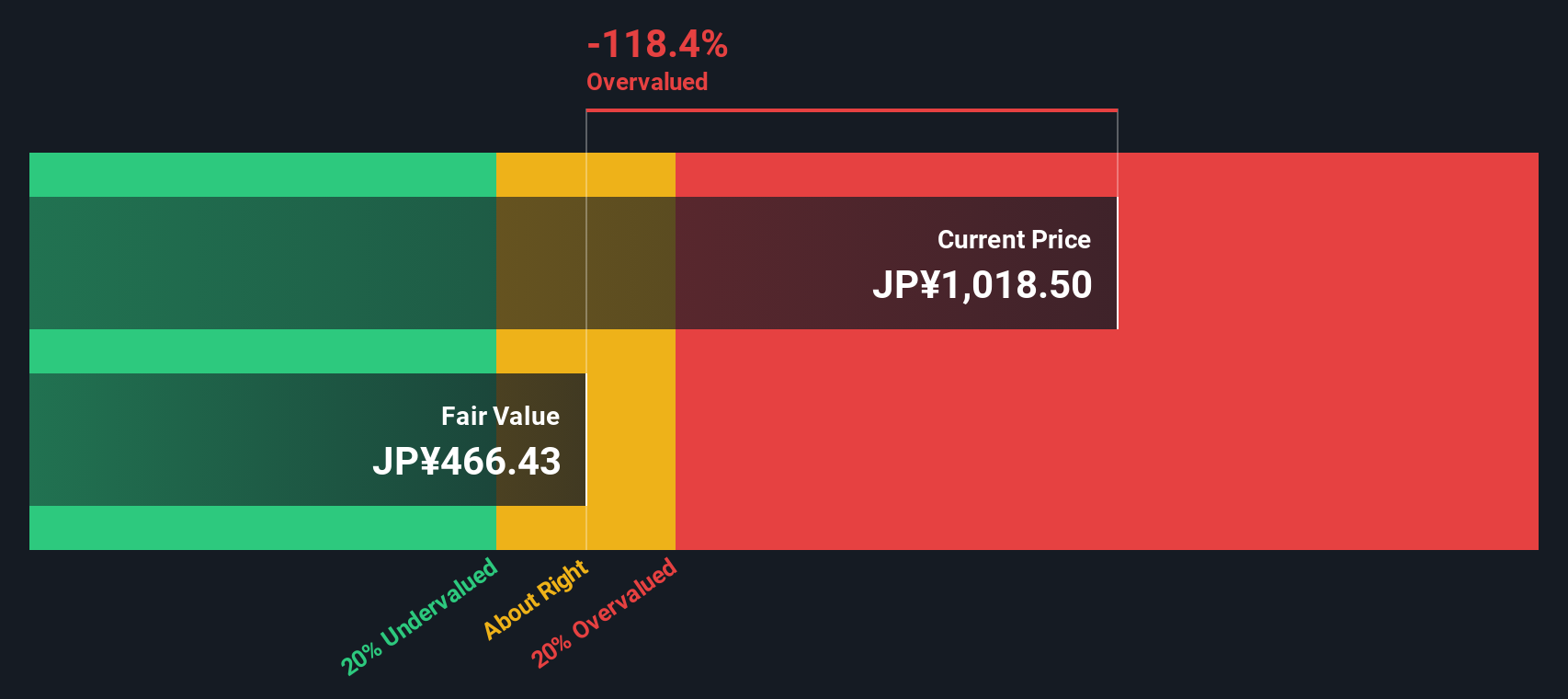

Another View: Discounted Cash Flow Tells a Different Story

The SWS DCF model paints a less optimistic picture and suggests Toda’s shares may be trading well above fair value. While multiples show near-market pricing, the DCF estimate values the stock much lower. Could the market’s confidence be running ahead of longer-term fundamentals?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Toda for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 928 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Toda Narrative

Of course, if you see things differently or want to take a hands-on approach, building your own view takes just a few minutes. Do it your way

A great starting point for your Toda research is our analysis highlighting 2 key rewards and 4 important warning signs that could impact your investment decision.

Ready to Unlock Your Next Opportunity?

Smart investors never settle for just one idea. Expand your horizon and spot the next winner by tapping into hand-picked opportunities across new and rising sectors.

- Tap into the future of healthcare by uncovering high-potential companies driving medical innovation in these 30 healthcare AI stocks.

- Maximize income potential by targeting dependable yields from these 15 dividend stocks with yields > 3% that go above the market average.

- Jump on breakthroughs in digital finance and blockchain by tracking emerging players within these 81 cryptocurrency and blockchain stocks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Toda might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:1860

Toda

Primarily engages in the construction and civil engineering businesses in Japan and internationally.

Proven track record with slight risk.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8147.4% undervalued

8 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

AU

AuCA on Nova Ljubljanska Banka d.d ·

Nova Ljubljanska Banka d.d will expect a 11.2% revenue boost driving future growth

Fair Value:€20916.5% undervalued

23 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

89 followersusers have followed this narrative

11 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

926 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative