Advertisement

- China

- /

- Metals and Mining

- /

- SHSE:601168

3 Asian Dividend Stocks To Consider With Yields Up To 4.1%

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate through a landscape marked by economic uncertainties and evolving monetary policies, Asian markets have shown resilience, with indices like Japan's Nikkei 225 and China's CSI 300 posting gains amid investor optimism in technology and artificial intelligence sectors. In this context, dividend stocks can offer investors a blend of income stability and potential growth, making them an attractive option for those looking to capitalize on the current market dynamics.

Top 10 Dividend Stocks In Asia

| Name | Dividend Yield | Dividend Rating |

| Wuliangye YibinLtd (SZSE:000858) | 5.39% | ★★★★★★ |

| Tsubakimoto Chain (TSE:6371) | 3.63% | ★★★★★★ |

| Torigoe (TSE:2009) | 3.89% | ★★★★★★ |

| NCD (TSE:4783) | 4.58% | ★★★★★★ |

| Kyoritsu Electric (TSE:6874) | 3.69% | ★★★★★★ |

| HUAYU Automotive Systems (SHSE:600741) | 4.09% | ★★★★★★ |

| GakkyushaLtd (TSE:9769) | 4.57% | ★★★★★★ |

| Changjiang Publishing & MediaLtd (SHSE:600757) | 4.51% | ★★★★★★ |

| Business Brain Showa-Ota (TSE:9658) | 3.83% | ★★★★★★ |

| Binggrae (KOSE:A005180) | 4.56% | ★★★★★★ |

Click here to see the full list of 1037 stocks from our Top Asian Dividend Stocks screener.

Let's explore several standout options from the results in the screener.

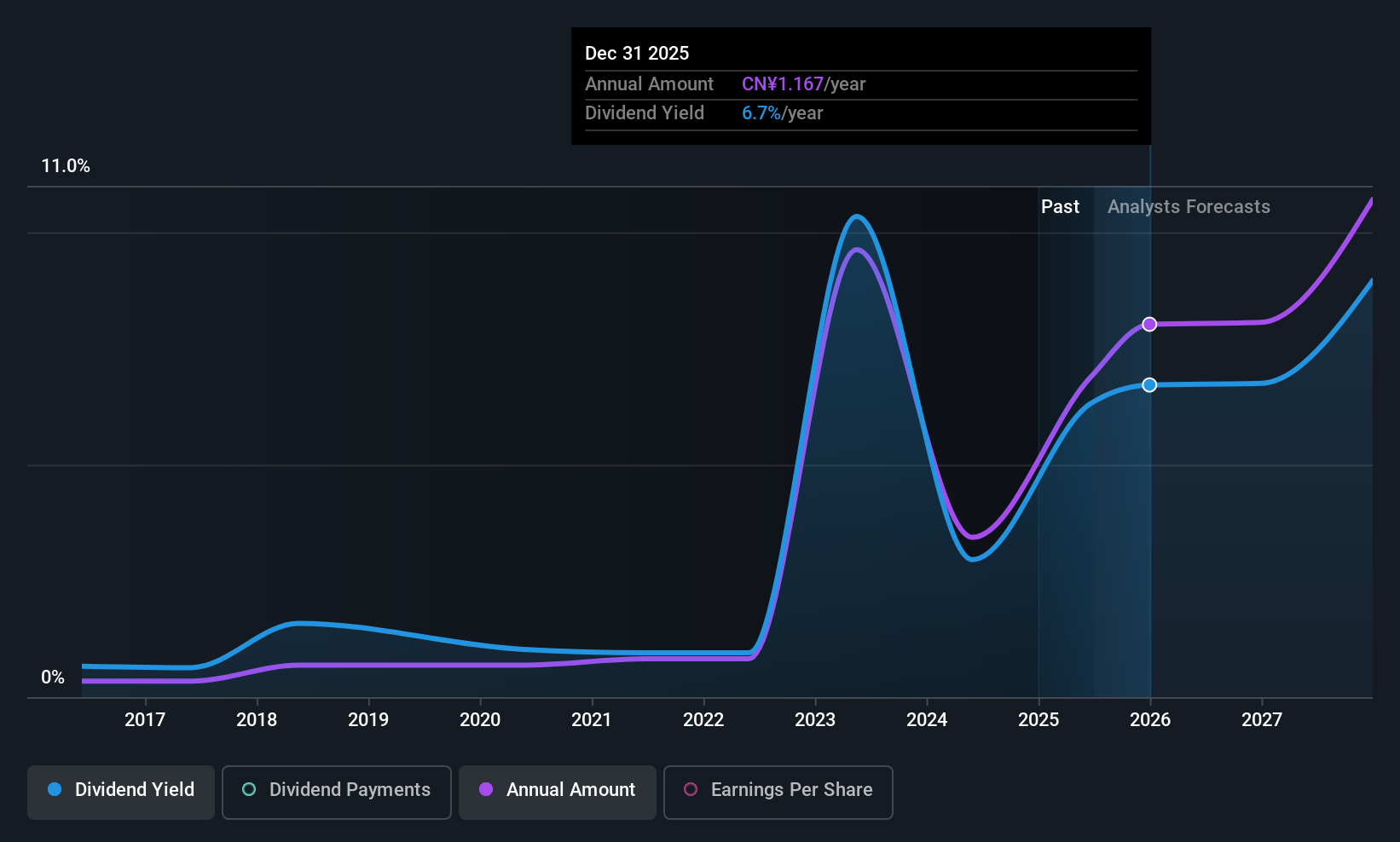

Western MiningLtd (SHSE:601168)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Western Mining Co., Ltd., with a market cap of CN¥57.43 billion, operates in the mining, smelting, and trading of metals both in Mainland China and internationally through its subsidiaries.

Operations: Western Mining Co., Ltd. generates revenue through its operations in mining, smelting, and metal trading activities both domestically in Mainland China and on an international scale.

Dividend Yield: 4.1%

Western Mining Ltd. offers a compelling dividend yield of 4.15%, ranking in the top 25% of CN market payers, although its dividend history has been volatile and unreliable over the past decade. Despite this, dividends are well-covered by cash flows with a payout ratio of 42.7%, suggesting sustainability alongside earnings coverage at 75.8%. Recent financials show strong revenue growth to CNY 48.44 billion, indicating potential for future stability in dividend payments.

- Unlock comprehensive insights into our analysis of Western MiningLtd stock in this dividend report.

- Our valuation report here indicates Western MiningLtd may be undervalued.

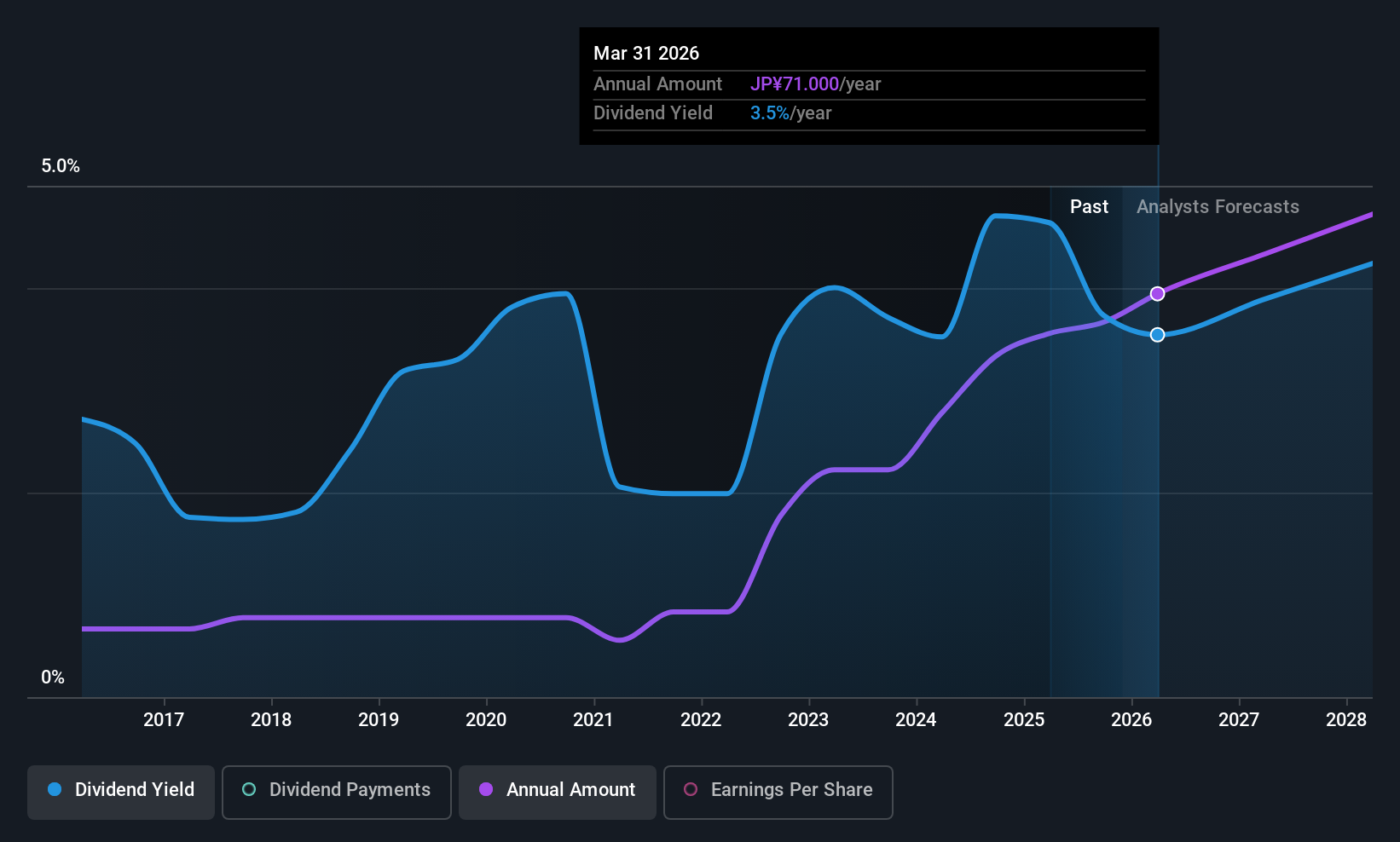

FUJIKURA COMPOSITES (TSE:5121)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: FUJIKURA COMPOSITES Inc. manufactures and sells industrial rubber components across Japan, the United States, China, and internationally with a market cap of ¥38.90 billion.

Operations: FUJIKURA COMPOSITES Inc. generates revenue from several segments, including Industrial Materials at ¥23.53 billion, Sporting Goods at ¥13.85 billion, and Fabric Processed Products at ¥3.65 billion.

Dividend Yield: 3.3%

FUJIKURA COMPOSITES' dividend payments are well-covered by earnings and cash flows, with payout ratios of 32.4% and 46.8%, respectively, despite a history of volatility over the past decade. The recent increase to JPY 33 per share suggests a commitment to shareholder returns, though the yield remains below Japan's top tier at 3.25%. Earnings growth of 18.4% last year and an optimistic forecast support potential future stability in dividends.

- Click here and access our complete dividend analysis report to understand the dynamics of FUJIKURA COMPOSITES.

- Our comprehensive valuation report raises the possibility that FUJIKURA COMPOSITES is priced lower than what may be justified by its financials.

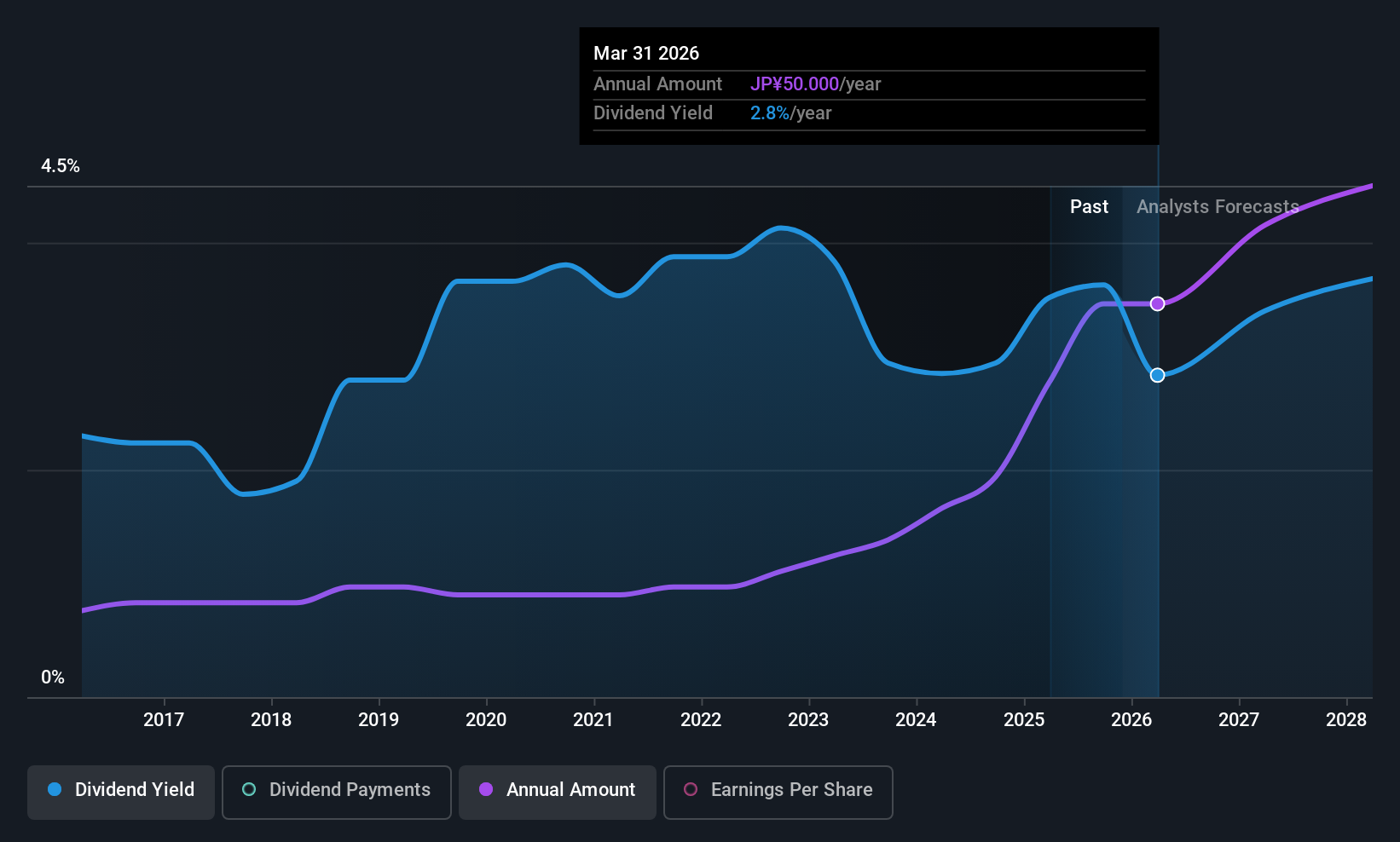

Gunma Bank (TSE:8334)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: The Gunma Bank, Ltd. offers a range of banking and financial services in Japan with a market cap of ¥678.65 billion.

Operations: Gunma Bank generates revenue through its diverse banking and financial services operations in Japan.

Dividend Yield: 3.3%

Gunma Bank's dividend reliability is underscored by a stable and growing payout history over the past decade, with recent increases to ¥30 per share. The bank's payout ratio of 43% indicates dividends are well-covered by earnings. Despite a dividend yield of 3.35%, which trails Japan's top-tier payers, Gunma Bank's earnings growth and upward revision in profit guidance suggest potential for sustained dividends. Recent buybacks totaling ¥5.99 billion further highlight shareholder value focus.

- Click to explore a detailed breakdown of our findings in Gunma Bank's dividend report.

- Our valuation report unveils the possibility Gunma Bank's shares may be trading at a premium.

Summing It All Up

- Gain an insight into the universe of 1037 Top Asian Dividend Stocks by clicking here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Western MiningLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:601168

Western MiningLtd

Engages in the mining, smelting, and trading of metals in Mainland China and internationally.

Undervalued established dividend payer.

Similar Companies

Market Insights

Advertisement

Weekly Picks

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

109 followersusers have followed this narrative

10 commentsusers have commented on this narrative

21 likesusers have liked this narrative

TI

TibiT on Canadian National Railway ·

The Indispensable Artery for a New North American Economy

Fair Value:CA$132.870.7% overvalued

20 followersusers have followed this narrative

4 commentsusers have commented on this narrative

3 likesusers have liked this narrative

RE

RecMag on Agfa-Gevaert ·

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Fair Value:€5.3988.2% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

NI

niteco on Texas Instruments ·

Engineered for Stability. Positioned for Growth.

Fair Value:US$314.4446.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$28.1829.5% undervalued

46 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BE

Bejgal on Fiverr International ·

Fiverr International will transform the freelance industry with AI-powered growth

Fair Value:US$36.8143.1% undervalued

79 followersusers have followed this narrative

7 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

109 followersusers have followed this narrative

10 commentsusers have commented on this narrative

21 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

939 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

145 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative