Advertisement

Sumitomo Mitsui (TSE:8316) EPS Surge Tests Bullish Growth Narrative Despite Margin Slippage

Simply Wall St

Reviewed by Simply Wall St

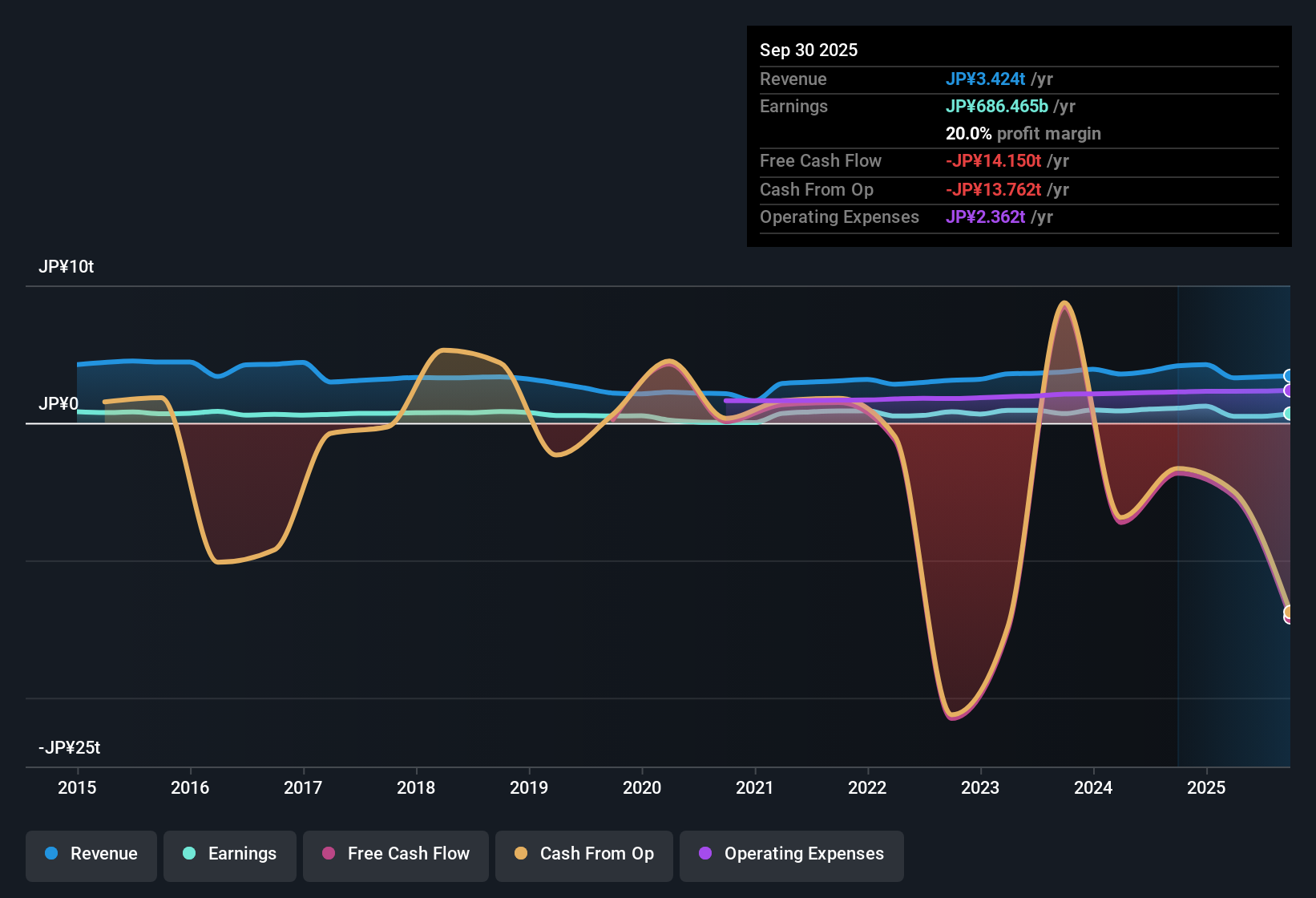

Sumitomo Mitsui Financial Group (TSE:8316) just posted a punchy Q2 2026 print, with revenue of ¥1.6 trillion and EPS of ¥144.69, while trailing 12 month revenue sits at about ¥3.4 trillion alongside EPS of ¥177.26 as the broader earnings picture continues to evolve. The company has seen revenue move from ¥1.54 trillion in Q2 2025 to ¥1.61 trillion in Q2 2026 and EPS shift from ¥90.39 to ¥144.69 over the same period, setting up this quarter as a clean read on how its profit engine is holding up. With trailing net profit margins easing off last year’s levels, investors will be watching these results closely to see whether the latest momentum is enough to steady the margin story.

See our full analysis for Sumitomo Mitsui Financial Group.With the headline numbers on the table, the next step is to line them up against the dominant narratives around Sumitomo Mitsui Financial Group to see which stories the latest quarter actually backs and which ones start to look a bit stretched.

Curious how numbers become stories that shape markets? Explore Community Narratives

Net income climbs to ¥556.6 billion despite softer margin backdrop

- Q2 2026 net income excluding extra items was ¥556,607 million, up from ¥376,898 million in Q1 2026 and from ¥353,817 million in Q2 2025, even though the trailing net profit margin has eased to 20% from 25.8% a year earlier.

- Consensus narrative around a gradually improving franchise is partly challenged here, because:

- Sequential profit growth from roughly ¥377.0 billion to ¥556.6 billion occurs alongside that margin step down from 25.8% to 20%, showing that higher absolute earnings are being generated on a less profitable base.

- Trailing twelve month EPS of ¥177.26 sits well below the stronger periods implied by earlier TTM figures like ¥309.89, so the latest jump needs to be seen in the context of a more volatile earnings run rate.

Loan book growth comes with higher non performing exposures

- Total loans rose from ¥109.6 trillion in Q2 2025 to ¥118.4 trillion in Q1 2026, while non performing loans increased from ¥896,522 million to ¥1,014,100 million and the allowance for bad loans over the last year covered 93% of those problem assets.

- Bears argue that credit risk is a key overhang, and the data gives them some support because:

- Non performing loans have grown by more than ¥100 billion over the last year while the allowance ratio sits below 100%, so a portion of problem credit is not fully covered by reserves.

- Quarterly net income of ¥556.6 billion and a 20% trailing net margin could come under pressure if additional provisions are needed to lift that 93% coverage closer to full protection.

Rich 27.7x P E contrasts with DCF upside and 3.19 percent yield

- The shares trade on a trailing P E of 27.7 times versus 11.4 times for JP banks and 15.8 times for peers, yet a DCF fair value of ¥7,550.62 sits about 34.5% above the current ¥4,949 share price and investors receive a 3.19% dividend yield.

- Bulls point to a favorable risk reward mix, and the valuation and payout metrics give that case some numerical backing because:

- Forecast earnings growth of 16.4% per year and revenue growth of 8.2% per year are both above broader JP market expectations, which helps explain why a premium multiple might be sustained even if margins are lower than last year.

- The gap between the current price and DCF fair value, combined with a 3.19% income stream, offers potential total return that can offset concerns about the 20% trailing net margin drifting down from 25.8% previously.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Sumitomo Mitsui Financial Group's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Despite the headline profit jump, Sumitomo Mitsui Financial Group is wrestling with thinner margins and rising non performing loans that leave credit risk uncomfortably exposed.

If growing problem assets and incomplete reserve coverage make you uneasy, move your attention to solid balance sheet and fundamentals stocks screener (1941 results) to focus on businesses with sturdier buffers and cleaner financial health.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:8316

Sumitomo Mitsui Financial Group

Provides banking, leasing, securities, consumer finance, and other services in Japan, the Americas, Europe, the Middle East, Asia, and Oceania.

Excellent balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

51 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

MO

mo7md on ADNOC Gas ·

ADNOC Gas future shines with a 21.4% revenue surge

Fair Value:د.إ3.728.9% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IN

IncomeAssets on Pulse Seismic ·

Watch Pulse Seismic Outperform with 13.6% Revenue Growth in the Coming Years

Fair Value:CA$4.4727.3% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$481.5% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

957 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

51 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative