Advertisement

Intesa Sanpaolo (BIT:ISP): Valuation Insights Following Moody’s Rating Upgrade and Renewed Investor Focus

Simply Wall St

Reviewed by Simply Wall St

Moody's recently upgraded Intesa Sanpaolo (BIT:ISP)'s long-term senior preferred unsecured rating to A3, citing a stable outlook and solid creditworthiness. Moves like this often capture the attention of both investors and analysts.

See our latest analysis for Intesa Sanpaolo.

After Moody's upgrade, market sentiment around Intesa Sanpaolo has leaned positive, with the share price recently closing at $5.586. While there have been some short-term fluctuations, the bank’s momentum stands out. Its year-to-date share price return is 45.09%, and the total shareholder return over the last year is an impressive 64.95%. Those longer-term numbers, including a 241% total return for shareholders over three years and 322% over five years, put recent moves and fresh optimism about credit quality in strong context.

If this kind of sustained outperformance makes you wonder what else is possible, now’s an ideal time to broaden your search and discover fast growing stocks with high insider ownership

Despite these standout gains, a critical question remains for investors: is Intesa Sanpaolo’s current share price truly a bargain, or has the market already factored in all of the bank’s future growth potential?

Most Popular Narrative: 9.5% Undervalued

According to the most popular narrative, Intesa Sanpaolo’s fair value sits noticeably above the recent close. Market participants are weighing continued earnings strength and future efficiency. Fresh analyst consensus reflects a gap between perceived value and what investors are currently willing to pay.

Strong asset quality and disciplined capital management support high shareholder returns and flexibility for future growth investments. Heavy dependence on Italy, rising fintech competition, and tightening regulations threaten Intesa Sanpaolo's profitability, margin stability, and long-term earnings growth.

Want to know the full story behind this valuation? The narrative is grounded in bold projections about future profit margins, shrinking shares, and earnings momentum. Intrigued by the tension between these numbers and current market sentiment? Dive into the details to see which financial levers could reshape the share price outlook.

Result: Fair Value of $6.17 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, structural challenges in Italy or a reversal in the bank’s asset quality could quickly undermine the current positive outlook and share price momentum.

Find out about the key risks to this Intesa Sanpaolo narrative.

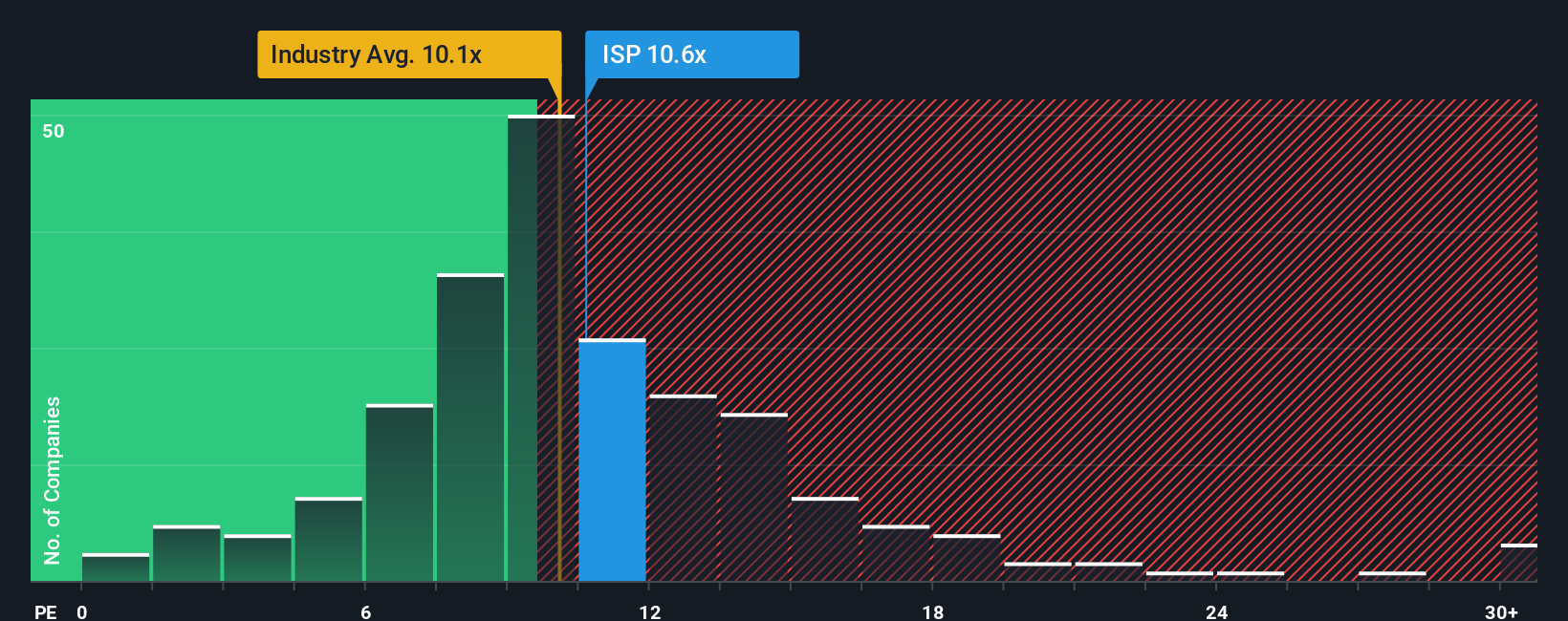

Another View: Valuation Through Market Comparisons

Looking at Intesa Sanpaolo from a price-to-earnings perspective, the shares currently trade at 10.7 times earnings. This figure is higher than the European banks average of 10.1 but below the peer average of 11.3. Compared to its fair ratio of 11, there is limited room for the market to re-rate higher without a shift in fundamentals. Is this tight margin a sign of hidden value or a warning for upside risk?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Intesa Sanpaolo Narrative

If you see the story differently or want to dig into the numbers yourself, you can build your own narrative in just a few minutes. Do it your way

A great starting point for your Intesa Sanpaolo research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Don’t just stop with Intesa Sanpaolo. Great investments are often found where others aren’t looking. Seize new opportunities now using these powerful screens below.

- Spot high-growth upstarts before the crowd by checking out these 3570 penny stocks with strong financials with strong financial momentum and big upside potential.

- Unlock the latest trends in artificial intelligence by seeing these 25 AI penny stocks powering breakthroughs in automation, data, and innovation.

- Maximize your returns by finding these 15 dividend stocks with yields > 3% that deliver both income and long-term stability, perfect for building a resilient portfolio.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About BIT:ISP

Intesa Sanpaolo

Provides various financial products and services in Italy, Central/Eastern Europe, the Middle East, and North Africa.

Established dividend payer with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

139 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

931 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative