Advertisement

- India

- /

- Auto Components

- /

- NSEI:BHARATSE

Bharat Seats Limited's (NSE:BHARATSE) Stock Has Been Sliding But Fundamentals Look Strong: Is The Market Wrong?

With its stock down 17% over the past month, it is easy to disregard Bharat Seats (NSE:BHARATSE). However, a closer look at its sound financials might cause you to think again. Given that fundamentals usually drive long-term market outcomes, the company is worth looking at. Particularly, we will be paying attention to Bharat Seats' ROE today.

Return on equity or ROE is a key measure used to assess how efficiently a company's management is utilizing the company's capital. Put another way, it reveals the company's success at turning shareholder investments into profits.

How Do You Calculate Return On Equity?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Bharat Seats is:

18% = ₹381m ÷ ₹2.1b (Based on the trailing twelve months to September 2025).

The 'return' refers to a company's earnings over the last year. Another way to think of that is that for every ₹1 worth of equity, the company was able to earn ₹0.18 in profit.

View our latest analysis for Bharat Seats

What Has ROE Got To Do With Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

Bharat Seats' Earnings Growth And 18% ROE

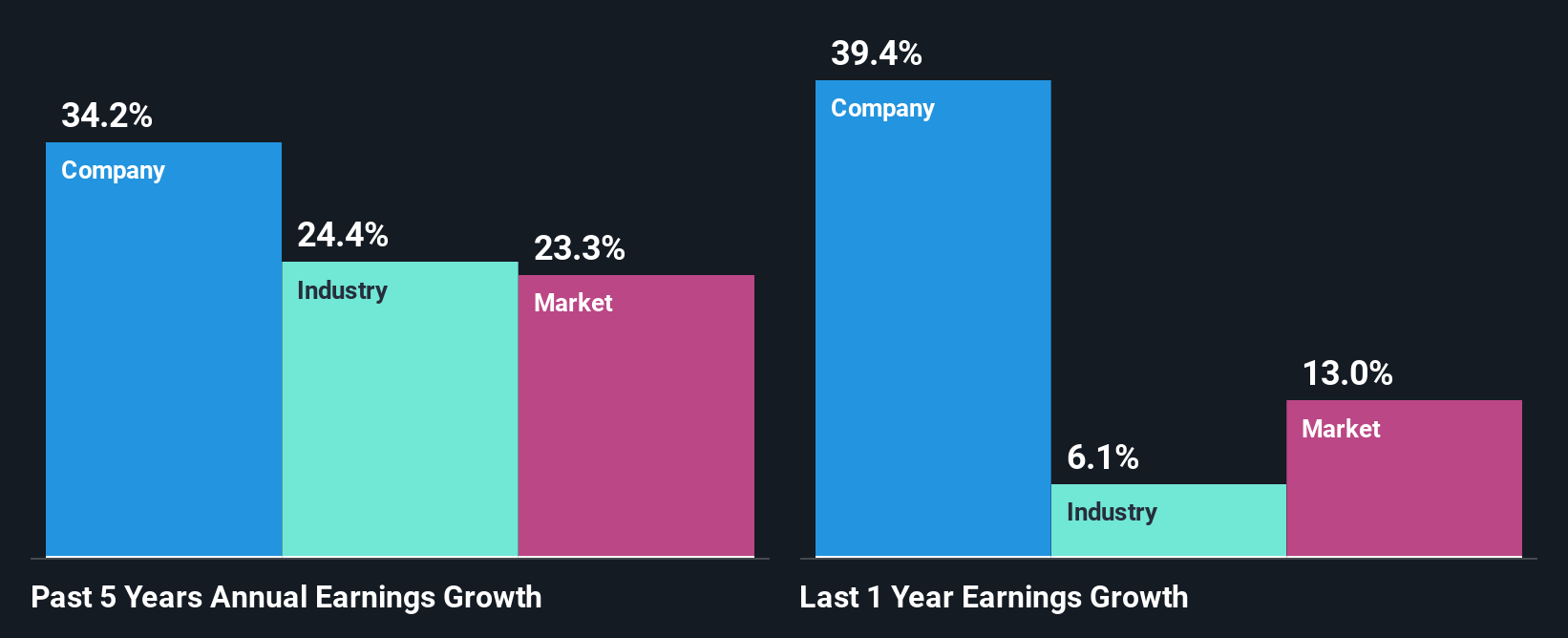

At first glance, Bharat Seats seems to have a decent ROE. Further, the company's ROE compares quite favorably to the industry average of 10%. This probably laid the ground for Bharat Seats' significant 34% net income growth seen over the past five years. However, there could also be other causes behind this growth. Such as - high earnings retention or an efficient management in place.

Next, on comparing with the industry net income growth, we found that Bharat Seats' growth is quite high when compared to the industry average growth of 24% in the same period, which is great to see.

Earnings growth is a huge factor in stock valuation. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). This then helps them determine if the stock is placed for a bright or bleak future. If you're wondering about Bharat Seats''s valuation, check out this gauge of its price-to-earnings ratio, as compared to its industry.

Is Bharat Seats Making Efficient Use Of Its Profits?

Bharat Seats' three-year median payout ratio to shareholders is 20%, which is quite low. This implies that the company is retaining 80% of its profits. So it looks like Bharat Seats is reinvesting profits heavily to grow its business, which shows in its earnings growth.

Moreover, Bharat Seats is determined to keep sharing its profits with shareholders which we infer from its long history of paying a dividend for at least ten years.

Summary

Overall, we are quite pleased with Bharat Seats' performance. Particularly, we like that the company is reinvesting heavily into its business, and at a high rate of return. Unsurprisingly, this has led to an impressive earnings growth. If the company continues to grow its earnings the way it has, that could have a positive impact on its share price given how earnings per share influence long-term share prices. Not to forget, share price outcomes are also dependent on the potential risks a company may face. So it is important for investors to be aware of the risks involved in the business. You can see the 2 risks we have identified for Bharat Seats by visiting our risks dashboard for free on our platform here.

Valuation is complex, but we're here to simplify it.

Discover if Bharat Seats might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:BHARATSE

Bharat Seats

Manufactures and sells seating systems and interior components for the automotive and surface transport industries in India.

Excellent balance sheet, good value and pays a dividend.

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

71 followersusers have followed this narrative

7 commentsusers have commented on this narrative

20 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$123.9% undervalued

12 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$245.0% overvalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

RE

RedhawkCC on Prime Medicine ·

PRME remains a long shot but publication in the New England Journal of Medicine helps.

Fair Value:US$0.0469.1k% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RA

RacerBVN on iShares Trust - iShares Preferred and Income Securities ETF ·

This one is all about the tax benefits

Fair Value:US$54.5543.4% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FA

FatPie on SoFi Technologies ·

Estimated Share Price is $79.54 using the Buffett Value Calculation

Fair Value:US$79.5465.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

118 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3925.9% undervalued

961 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

71 followersusers have followed this narrative

7 commentsusers have commented on this narrative

20 likesusers have liked this narrative