Advertisement

- Israel

- /

- Renewable Energy

- /

- TASE:ENRG

Does Energix - Renewable Energies (TLV:ENRG) Have A Healthy Balance Sheet?

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Energix - Renewable Energies Ltd. (TLV:ENRG) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Energix - Renewable Energies's Debt?

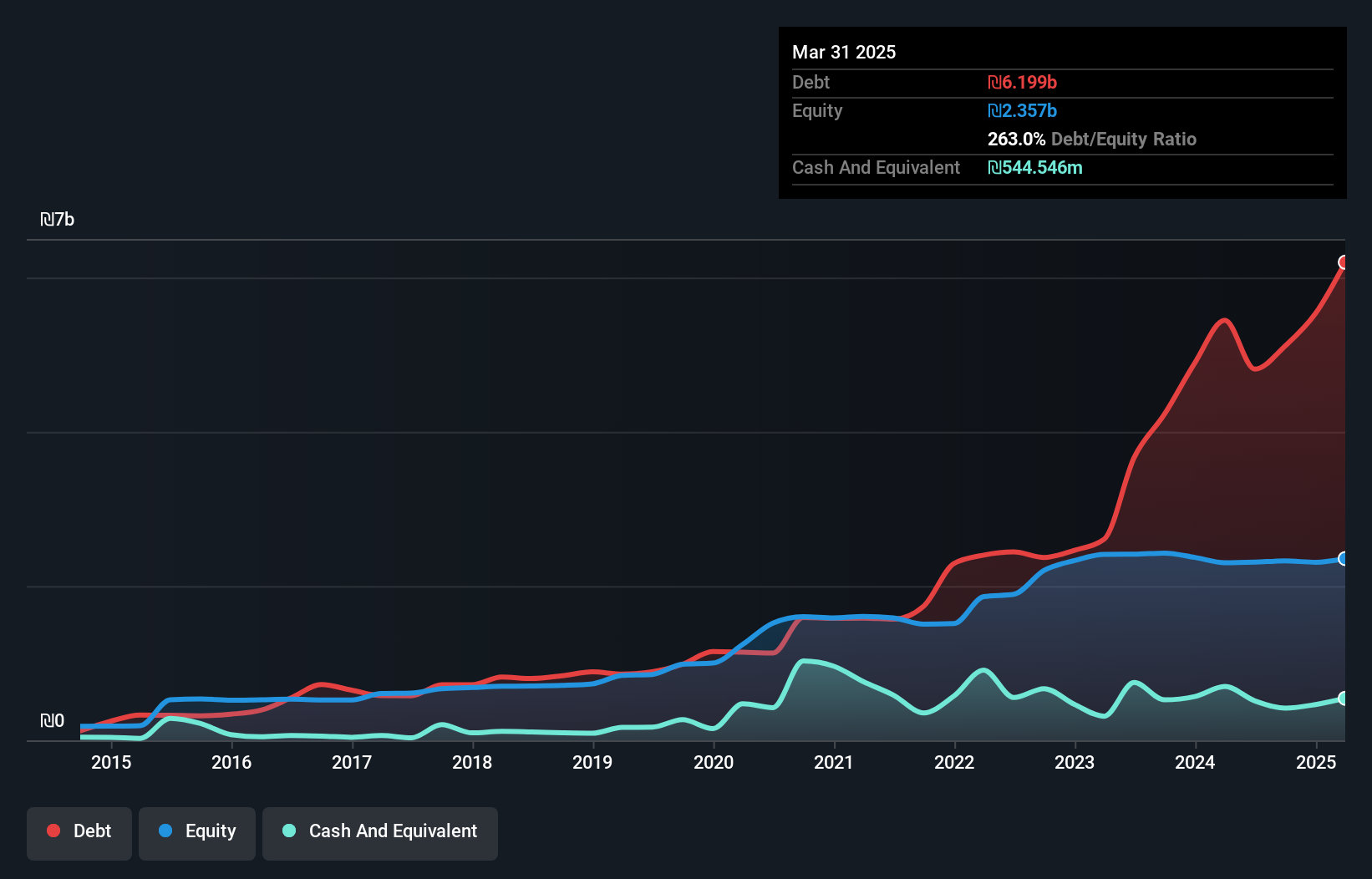

The image below, which you can click on for greater detail, shows that at March 2025 Energix - Renewable Energies had debt of ₪6.20b, up from ₪5.45b in one year. However, because it has a cash reserve of ₪544.5m, its net debt is less, at about ₪5.65b.

How Healthy Is Energix - Renewable Energies' Balance Sheet?

According to the last reported balance sheet, Energix - Renewable Energies had liabilities of ₪2.01b due within 12 months, and liabilities of ₪7.59b due beyond 12 months. On the other hand, it had cash of ₪544.5m and ₪220.5m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by ₪8.83b.

Given this deficit is actually higher than the company's market capitalization of ₪7.41b, we think shareholders really should watch Energix - Renewable Energies's debt levels, like a parent watching their child ride a bike for the first time. Hypothetically, extremely heavy dilution would be required if the company were forced to pay down its liabilities by raising capital at the current share price.

Check out our latest analysis for Energix - Renewable Energies

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Energix - Renewable Energies shareholders face the double whammy of a high net debt to EBITDA ratio (11.3), and fairly weak interest coverage, since EBIT is just 2.1 times the interest expense. The debt burden here is substantial. Looking on the bright side, Energix - Renewable Energies boosted its EBIT by a silky 36% in the last year. Like a mother's loving embrace of a newborn that sort of growth builds resilience, putting the company in a stronger position to manage its debt. There's no doubt that we learn most about debt from the balance sheet. But it is Energix - Renewable Energies's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the last three years, Energix - Renewable Energies saw substantial negative free cash flow, in total. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Our View

To be frank both Energix - Renewable Energies's net debt to EBITDA and its track record of converting EBIT to free cash flow make us rather uncomfortable with its debt levels. But at least it's pretty decent at growing its EBIT; that's encouraging. We're quite clear that we consider Energix - Renewable Energies to be really rather risky, as a result of its balance sheet health. For this reason we're pretty cautious about the stock, and we think shareholders should keep a close eye on its liquidity. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 3 warning signs for Energix - Renewable Energies you should be aware of, and 2 of them can't be ignored.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Valuation is complex, but we're here to simplify it.

Discover if Energix - Renewable Energies might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TASE:ENRG

Energix - Renewable Energies

Through its subsidiaries, engages in the initiation, development, financing, establishing, construction, management, and operation of facilities for the production, storage, and sale of electricity from renewable energy sources in Israel, Poland, Lithuania, and the United States.

Slight risk and overvalued.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|8.5% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|24.6% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.1% undervalued

LI

Community Contributor