Advertisement

Ayalon Insurance (TASE:AYAL) Margin Improvement Reinforces Bullish Quality Narrative Despite Volatile Share Price

Simply Wall St

Reviewed by Simply Wall St

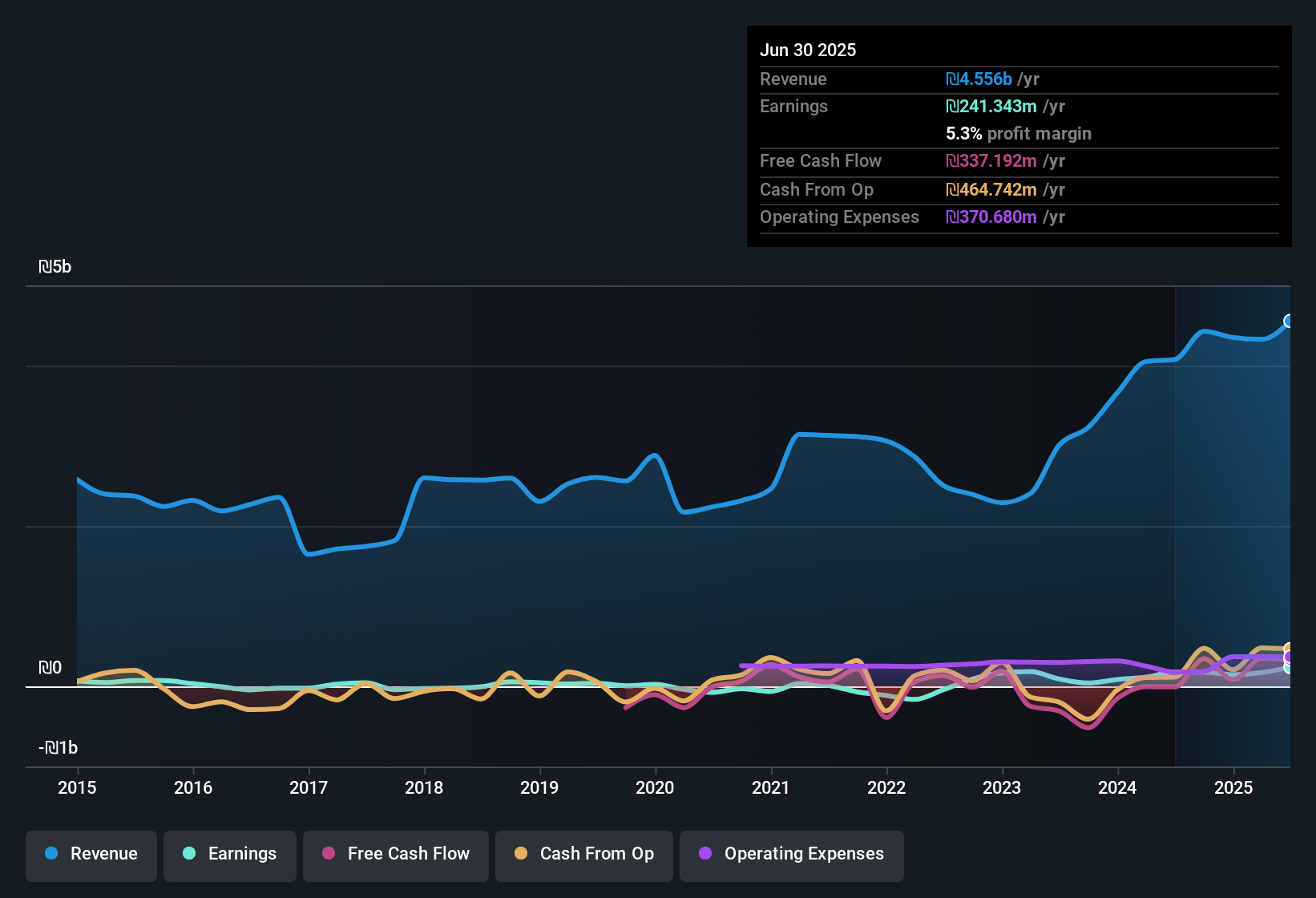

Ayalon Insurance (TASE:AYAL) just delivered its Q2 2025 financials, reporting total revenue of ₪1.3 billion and basic EPS of ₪5.78. Over the last six quarters, the company has seen revenue rise from ₪1.1 billion in Q1 2024 to a recent high, with EPS increasing from ₪1.29 to ₪5.78 over the same period. Investors will note that profit margins expanded in the most recent period, setting the stage for a lively discussion of what is driving these results.

See our full analysis for Ayalon Insurance.Next, we will see how these headline results compare to the most widely discussed narratives among investors and analysts. Some long-held views may be reinforced, while others could be up for debate.

Curious how numbers become stories that shape markets? Explore Community Narratives

Profit Margins Reach 5.3% High

- Net profit margin climbed to 5.3% for the trailing twelve months, up from last year's 4.4%, with net income for Q2 2025 reaching ₪144.3 million.

- Margin expansion strongly supports the narrative that Ayalon’s core insurance operations have gained efficiency, helped by a 34.8% earnings growth for the year.

- Analysts tracking these figures point to improved operational discipline. Even with higher top-line growth in the last two quarters, profit capture has kept pace or improved.

- Despite some sector-wide cost pressures, Ayalon’s ability to boost margins has made the quality of its earnings a key talking point for those highlighting its robust business fundamentals.

Shares Trade Well Below DCF Value

- The company’s current share price of ₪94.20 is 25.9% lower than its DCF fair value of ₪127.20, while its Price-to-Earnings Ratio stands at 10.6x versus a peer average of 13.1x.

- What surprises many is that even as profit margins have risen, the share price remains at a discount. This supports the case that the stock could be undervalued relative to its quality of earnings.

- Bulls argue this valuation gap reflects investor caution after recent volatility in Israeli markets. With no major risks flagged in the past year, many consider it an attractive entry point.

- The P/E ratio’s comparison to both peers and the Asian insurance sector is regularly cited by buyers as evidence that Ayalon’s valuation disconnect is not merely market-wide, but company-specific due to recent improvement in fundamentals.

Profit Growth Still Trails Five-Year Trend

- Earnings grew by 34.8% over the last year, which is solid but below the company’s five-year average growth of 54% per year.

- The prevailing market view highlights that while year-over-year profit gains remain strong, Ayalon’s current growth rate represents a deceleration from its own history. This suggests expectations for “outsized” future acceleration may be too optimistic.

- This context, when paired with rising margins, signals durable but moderating growth rather than ongoing explosive upside.

- For longer-term holders, the figures reinforce Ayalon’s stability in core business while resetting expectations around future compounding.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Ayalon Insurance's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Despite impressive margin expansion, Ayalon's current profit growth lags behind its robust five-year track record. This suggests there may be slowing momentum ahead.

If you want steadier gains through all cycles, check out stable growth stocks screener (2075 results) to discover companies consistently delivering reliable growth without sharp slowdowns.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TASE:AYAL

Ayalon Insurance

Through its subsidiaries, provides various insurance products in Israel.

Excellent balance sheet and good value.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7924.0% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative