Advertisement

- Israel

- /

- Healthcare Services

- /

- TASE:MDTR

Mediterranean Towers (TASE:MDTR) Net Profit Surges on One-Off Gain, Raising Questions About Sustainability

Simply Wall St

Reviewed by Simply Wall St

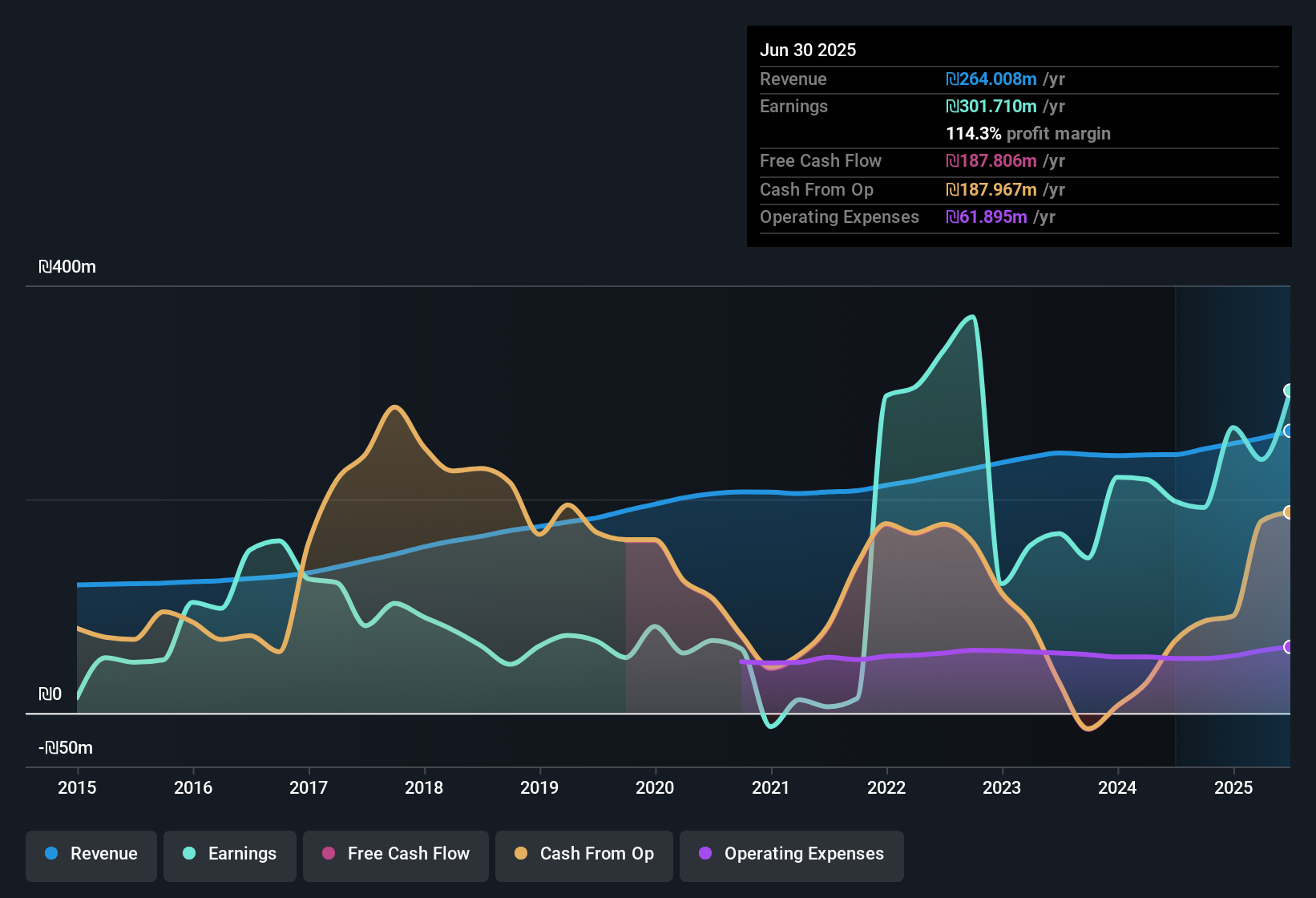

Mediterranean Towers (TASE:MDTR) just posted its Q2 2025 results, reporting total revenue of ₪68.2 million and basic EPS of ₪0.61. Looking back, the company saw revenue increase from ₪61.4 million in Q2 2024 to ₪68.2 million in Q2 2025, with basic EPS advancing from ₪0.18 to ₪0.61 over the same stretch. These headline numbers come amid notably high margins, setting the stage for investors to weigh the sustainability of such profitability.

See our full analysis for Mediterranean Towers.Now, let’s put these figures in perspective by comparing them with the prevailing narratives and expectations. Some beliefs might hold up, but there is always room for fresh insights when the real numbers are released.

Curious how numbers become stories that shape markets? Explore Community Narratives

Massive One-Off Gain Lifts Net Profit Margins

- Over the past twelve months, Mediterranean Towers’ net profit margins surged to 82%, far exceeding its historic average margin and propelled by a one-off gain of ₪468.9 million.

- What stands out from the prevailing analysis is that this exceptional gain heavily skews the profit narrative and raises doubts about the sustainability of such profitability levels.

- Reported profits rose 52.2% year-on-year, but this jump is largely attributed to the one-time event and not ongoing business strength.

- Without this outlier, profit comparisons with previous periods and peers may be less favorable, tempering any over-optimistic interpretations.

- Consensus narrative suggests investors should consider both the boost from the extraordinary gain and the underlying recurring performance when assessing future prospects.

- This rare event makes it crucial to distinguish between enduring growth and isolated spikes when forming expectations about future results.

- The core business trend, after normalizing for one-offs, is more moderate, providing a balanced view for long-term shareholders.

Here's why the latest surge could mean more than meets the eye for those tracking the full story. 📊 Read the full Mediterranean Towers Consensus Narrative.

Valuation Remains Attractive Versus Peers

- Mediterranean Towers trades at a Price-to-Earnings ratio of 7.2x, which is significantly below the Israeli market average of 15.1x, industry average of 19.5x, and peer average of 27x.

- While bulls highlight the apparent value and discounted multiples, the consensus market perspective points out that such a low multiple could partly reflect persistent concerns about debt coverage and unreliable dividend history.

- Debt coverage issues flagged in recent analysis, combined with earnings boosted by non-recurring items, suggest the discount may be justified for now.

- If core performance strengthens and risks around leverage recede, a re-rating toward peer valuations could be possible.

Profit Growth Rate Outpaces Five-Year Trend

- Profit expansion reached 52.2% year-on-year, well ahead of the company’s historical five-year annual average growth rate of 23.6%.

- This rapid growth draws bullish attention to the company’s ability to capitalize on sector tailwinds, but the consensus points to a need for caution, as a substantial share of the jump is linked to non-repeatable factors.

- Momentum like this is rarely sustainable without support from underlying operational improvements.

- Investors may want to watch the next quarters to see if momentum continues once the one-off gain is no longer in play.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Mediterranean Towers's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Mediterranean Towers’ attractive valuation is tempered by concerns around debt coverage, one-off profit boosts, and uncertainty about the reliability of future dividends.

If you want stocks built on stronger financial footing, check out solid balance sheet and fundamentals stocks screener (1938 results) and discover options with robust balance sheets designed to withstand uncertainty.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TASE:MDTR

Mediterranean Towers

Owns and operates residential homes for the elderly population in Israel.

Proven track record average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7924.0% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative