Advertisement

- Israel

- /

- Capital Markets

- /

- TASE:IBI

I.B.I. Investment House (TASE:IBI) Net Profit Margin Decline Challenges Bullish Narrative

Simply Wall St

Reviewed by Simply Wall St

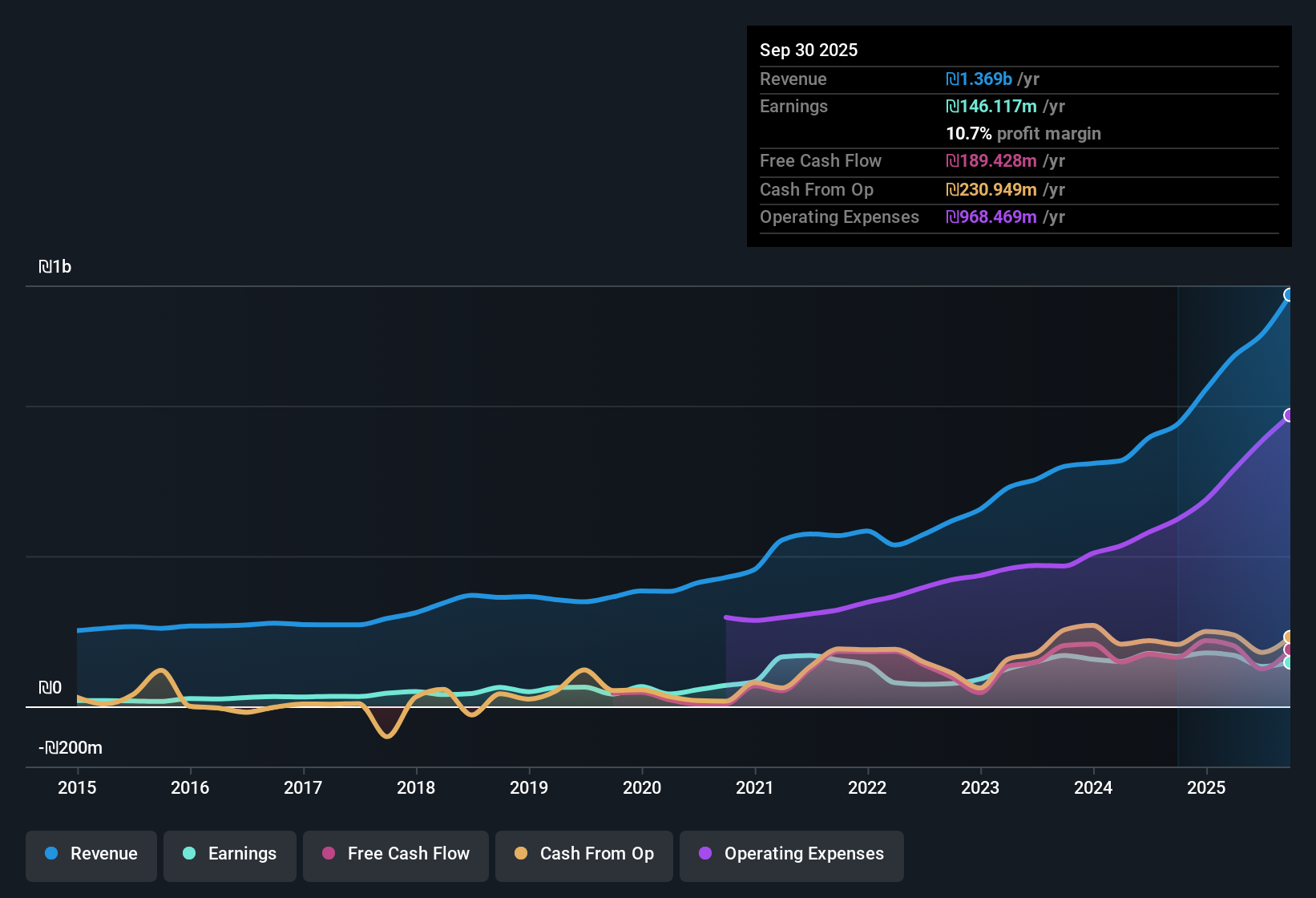

I.B.I. Investment House (TASE:IBI) has posted its Q3 2025 results, reporting revenue of ₪377.9 million and net income of ₪45.5 million, with basic EPS of ₪3.32 for the quarter. Historically, the company has seen revenue climb from ₪245.7 million in Q3 2024 to its current level, with basic EPS also rising from ₪2.51 over the same period. Investors are likely to focus on the company’s profitability trends as margins continue to shape sentiment around these results.

See our full analysis for I.B.I. Investment House.Let’s dig into how the latest numbers compare to the most widely tracked narratives for I.B.I. Investment House. Some expectations are met, while others are put to the test.

Curious how numbers become stories that shape markets? Explore Community Narratives

Profit Margin Drop Stands Out

- Net profit margin dropped to 10.7% over the past year, down from 17.7% the year before, even as revenue growth stayed positive.

- Analysts point out that while I.B.I. maintains high quality earnings and posted average growth of 9.1% per year over five years, the recent decline in margins complicates the case for continued outperformance.

- Shrinking profitability could make it harder to sustain robust dividend payments and high valuation levels.

- Figures suggest the strength once seen in past years is now showing signs of pressure, especially on the income line.

- Current annual profit trends mark a reversal from steady historical gains, challenging hopes for a rapid rebound.

Share Price Sits Above DCF Fair Value

- The share price is ₪275.00, notably above its DCF fair value estimate of ₪168.01, and trades at a 25.7x PE, higher than industry averages (20.5x peer group; 19.3x industry).

- Market opinion recognizes the company’s track record and diversified business strengths. However, valuations at this level mean investors are betting on a turnaround in profitability that recent margin data has yet to confirm.

- Premium pricing is not being matched by short-term earnings performance, leaving the bar higher for future results to justify current levels.

- Bulls typically seek this kind of stability, but critics might question whether price already factors in all of I.B.I.'s advantages.

Dividend Yield Faces Coverage Challenge

- Dividend yield stands at 4.17%, but it is not well covered by earnings according to the latest financial analysis.

- General market sentiment notes that while income seekers may find the yield attractive, the weakening profit margin raises sustainability concerns.

- Elevated payout risk could dampen enthusiasm if future profits continue to lag versus historical averages.

- No significant risks flagged in statements, yet financial coverage for dividends is running thin compared to portfolio income expectations.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on I.B.I. Investment House's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

I.B.I. Investment House’s weakening profit margins and questionable dividend coverage cast doubt on the sustainability of its current income payouts.

If reliable income matters to you, consider these these 1933 dividend stocks with yields > 3% that deliver strong yields with coverage metrics that withstand changing profit cycles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TASE:IBI

I.B.I. Investment House

I.B.I Investment House Ltd. is a publicly owned holding investment firm with approximately NIS 11 billion ($2.63 billion) in assets under management.

Flawless balance sheet second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

JO

JohnJ on Worldline ·

No miracle in sight

Fair Value:€7.0178.0% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k2.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

79 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

90 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

928 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative