Advertisement

- Israel

- /

- Hospitality

- /

- TASE:ISTA

Issta (TASE:ISTA) Net Profit Margin Drops to 19.3%, Challenging Profitability Narrative

Simply Wall St

Reviewed by Simply Wall St

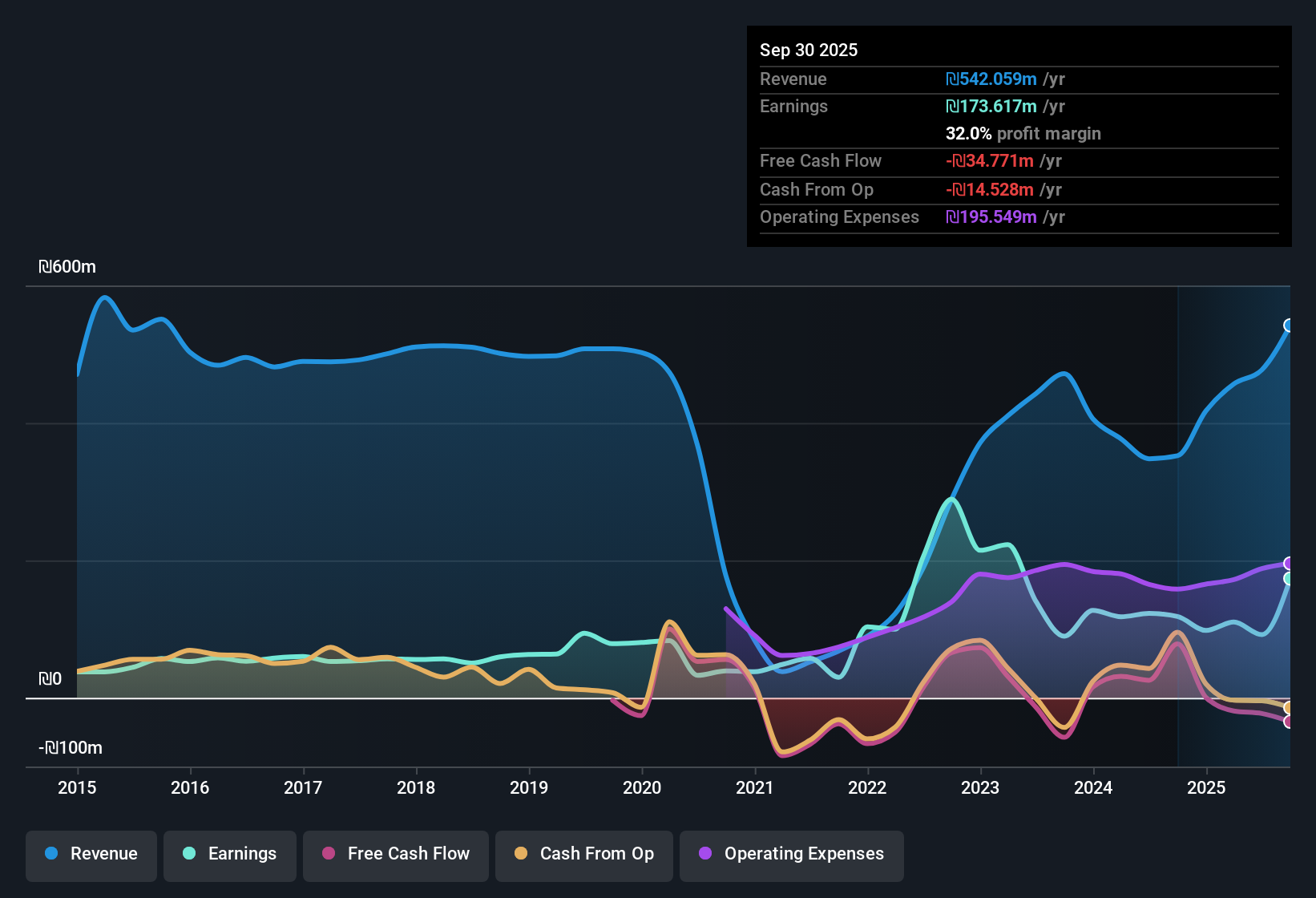

Issta (TASE:ISTA) just posted its Q2 2025 numbers, reporting revenue of ₪111.98 million and EPS of ₪0.35. For context, revenue was ₪93.82 million with EPS of ₪1.37 in Q1 2025, while Q4 2024 saw revenue at ₪109.42 million and EPS of ₪1.63. Margins remained under pressure, painting a mixed picture for investors focused on signs of sustainable profitability.

See our full analysis for Issta.Next, we examine the latest results in light of current narratives and market expectations, so you can see what the numbers mean in context.

Curious how numbers become stories that shape markets? Explore Community Narratives

Margin Compression Hits Profit Growth

- Net profit margin dropped sharply to 19.3% in the last twelve months, falling from 35.3% a year ago. This reflects escalating costs or a changing revenue mix that has not been offset by revenue gains.

- Profitability contraction puts the spotlight on scale and cost management as travel volumes normalize. Analysis emphasizes that strong brand and diversified distribution remain positives, yet margin pressures challenge the bullish case for leveraging demand recovery.

- The latest twelve months’ net income of ₪91.88 million is materially below the prior period, showing that previous years' double-digit growth has not been matched.

- Bulls cite Issta’s established market presence and broad service offering, but narrowing margins suggest competitive and cost headwinds persist even as global travel rebounds.

Valuation Below Peer Averages

- Issta’s price-to-earnings ratio stands at 20.3x, notably undercutting both the Asian Hospitality industry average of 22.1x and peer group average of 25x. This signals relative value for investors monitoring sector comps.

- The value gap appeals to cost-conscious investors who see sector-wide recovery as an opportunity. However, the stock trades at ₪107, above the DCF fair value of ₪67.19, which prompts caution in tying sector optimism too closely to current price.

- Investors weighing sector multiples against estimated fair value could find upside limited unless operating improvements are realized.

- The narrative highlights that longer-term annual earnings growth averaged 10.4% over five years, suggesting underlying strength if recent margin compressions prove temporary.

Dividend Yield Faces Sustainability Questions

- The trailing twelve month dividend yield sits at 5.61%, but coverage is insufficient, as payouts exceed both earnings and free cash flow according to risk analysis.

- While many travel stocks offer modest yields, sector peers often display stronger payout ratios, so the high yield here comes at the expense of safety and predictability.

- The company’s debt is not well covered by operating cash flow, a structural risk that could pressure dividends if operating performance stalls further.

- Market watchers stress that attractive yields should not distract from underlying payout risks, especially where profits and cash flows are volatile.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Issta's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Issta's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Issta’s margin compression, limited dividend coverage, and debt risks raise concerns about its financial resilience and ability to sustain shareholder returns.

If you want stocks backed by stronger balance sheets and less payout risk, try solid balance sheet and fundamentals stocks screener (1938 results) to uncover companies designed for financial stability over the long haul.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TASE:ISTA

Issta

Provides travel and tourism services to private and business customers, groups, and organizations in Israel and internationally.

Slight risk second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7924.0% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative