Advertisement

- Israel

- /

- Construction

- /

- TASE:CMER

C. Mer Industries (TASE:CMER) Net Margin Rises to 5.6%, Undercutting Market Caution on Profitability

Simply Wall St

Reviewed by Simply Wall St

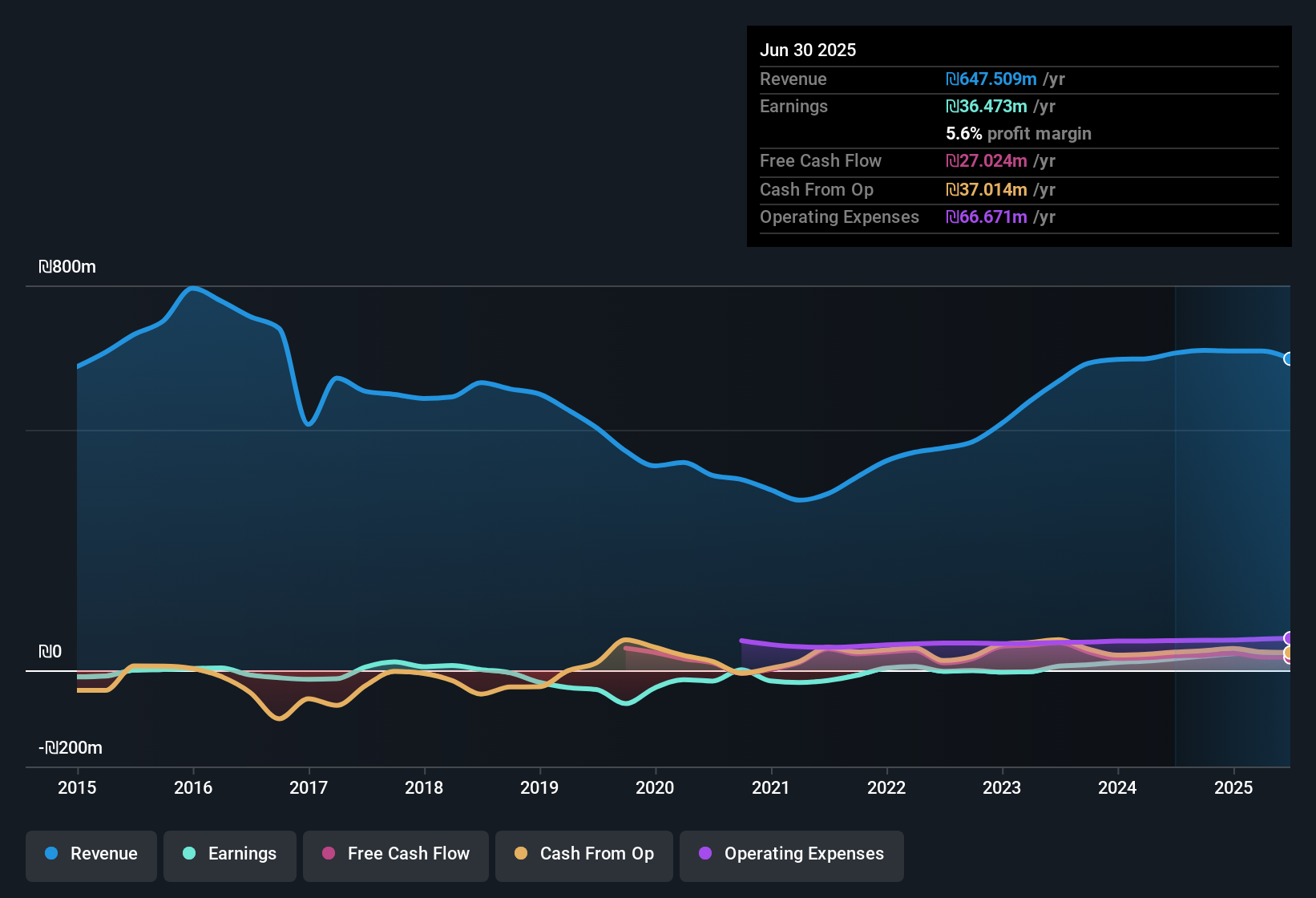

C. Mer Industries (TASE:CMER) just posted its Q3 2025 results, reporting revenue of 150.266 million ILS and basic EPS of 0.58 ILS. Looking back over the last year, the company has seen total revenue range from 174.506 million ILS in Q3 2024 to 150.266 million ILS this quarter, while basic EPS shifted from 0.89 ILS to 0.58 ILS over the same periods. Margins have remained a focal point for investors, with the most recent results showing how profitability measures up to previous quarters.

See our full analysis for C. Mer Industries.The next section will put these latest numbers head-to-head with the dominant market narratives to reveal what lines up and what might surprise investors.

Curious how numbers become stories that shape markets? Explore Community Narratives

Net Margin Hits 5.6%, Outpacing Prior Year

- C. Mer Industries has expanded its net profit margin to 5.6% over the past twelve months, up from 3.6% in the previous year. This reflects a notable jump in operational efficiency.

- Analysts see this margin improvement as a sign of healthier underlying profitability, especially since sustained earnings growth (+51.7%) remains well above the company's historic lows.

- Net income for the latest twelve months reached 36.5 million ILS, continuing a steady climb from 24.0 million ILS a year ago.

- With consistent growth in both net profit and margin, what stands out is that these improvements come despite revenue dipping in the most recent quarter. This scenario strengthens confidence in cost control and business model adaptability.

PE Ratio Undercuts Peers Despite Profit Jump

- Trading at a Price-to-Earnings ratio of 11.3x versus 19.1x for industry peers, C. Mer Industries appears attractively valued after its robust earnings progress.

- Investors weighing the consensus narrative point out that this valuation discount may offer a margin of safety, given the company has managed above-market earnings growth and margin expansion over the past year.

- Industry comparables trade at materially higher multiples, yet face many of the same sector headwinds around contract timing and customer budgets.

- While some may expect such a low multiple to signal concerns, the company's net income growth and margin gains indicate it is not simply a value trap.

Share Price Volatility and Debt Remain Watchpoints

- The company’s share price has been volatile over the past three months, with ongoing concern about high debt levels tempering otherwise strong fundamentals.

- What’s striking is the juxtaposition between rising profitability (trailing twelve month EPS of 2.79 ILS) and the persistent risks posed by leverage, as highlighted in analyst commentary.

- Despite a positive trajectory in earnings and net margin, investors should track how debt impacts future flexibility, especially as margins have only recently improved.

- This ongoing balance of profit gains against exposure to debt and market swings could keep the stock sensitive to both good and bad news catalysts.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on C. Mer Industries's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Despite improved margins and net income, C. Mer Industries continues to face significant concerns regarding its high debt and financial flexibility.

If you want peace of mind with companies that have stronger finances and lower debt risk, check out solid balance sheet and fundamentals stocks screener (1938 results) built to withstand future volatility.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TASE:CMER

C. Mer Industries

Provides solutions in the areas of homeland security (HLS), communication infrastructure, and defense technologies.

Solid track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7924.0% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative