Advertisement

- Hong Kong

- /

- Infrastructure

- /

- SEHK:576

Zhejiang Expressway Co., Ltd.'s (HKG:576) Stock's On An Uptrend: Are Strong Financials Guiding The Market?

Zhejiang Expressway's (HKG:576) stock is up by a considerable 14% over the past three months. Given that the market rewards strong financials in the long-term, we wonder if that is the case in this instance. In this article, we decided to focus on Zhejiang Expressway's ROE.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. Simply put, it is used to assess the profitability of a company in relation to its equity capital.

How To Calculate Return On Equity?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Zhejiang Expressway is:

8.8% = CN¥8.1b ÷ CN¥93b (Based on the trailing twelve months to September 2025).

The 'return' is the yearly profit. Another way to think of that is that for every HK$1 worth of equity, the company was able to earn HK$0.09 in profit.

View our latest analysis for Zhejiang Expressway

What Has ROE Got To Do With Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

A Side By Side comparison of Zhejiang Expressway's Earnings Growth And 8.8% ROE

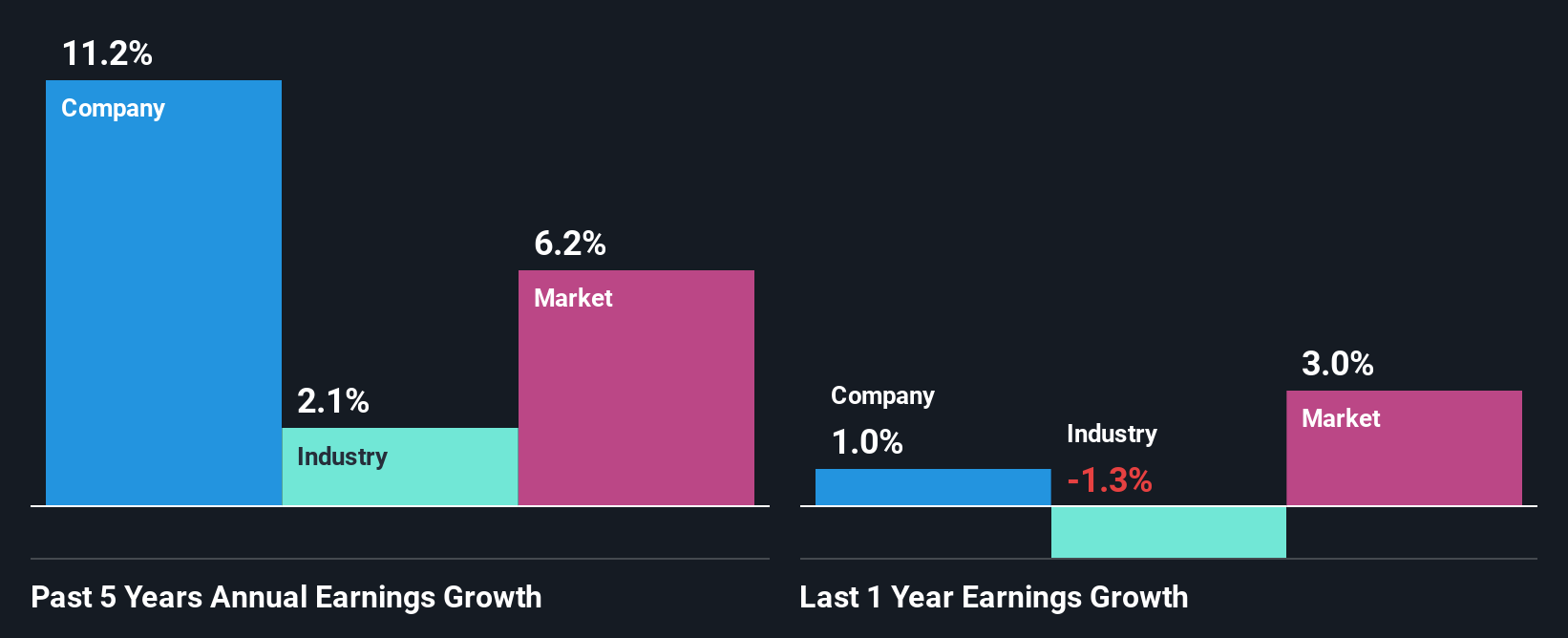

When you first look at it, Zhejiang Expressway's ROE doesn't look that attractive. Although a closer study shows that the company's ROE is higher than the industry average of 6.9% which we definitely can't overlook. This certainly adds some context to Zhejiang Expressway's moderate 11% net income growth seen over the past five years. Bear in mind, the company does have a moderately low ROE. It is just that the industry ROE is lower. Hence there might be some other aspects that are causing earnings to grow. E.g the company has a low payout ratio or could belong to a high growth industry.

We then compared Zhejiang Expressway's net income growth with the industry and we're pleased to see that the company's growth figure is higher when compared with the industry which has a growth rate of 2.1% in the same 5-year period.

Earnings growth is a huge factor in stock valuation. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. This then helps them determine if the stock is placed for a bright or bleak future. Is Zhejiang Expressway fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is Zhejiang Expressway Making Efficient Use Of Its Profits?

With a three-year median payout ratio of 33% (implying that the company retains 67% of its profits), it seems that Zhejiang Expressway is reinvesting efficiently in a way that it sees respectable amount growth in its earnings and pays a dividend that's well covered.

Additionally, Zhejiang Expressway has paid dividends over a period of at least ten years which means that the company is pretty serious about sharing its profits with shareholders. Our latest analyst data shows that the future payout ratio of the company over the next three years is expected to be approximately 39%. Regardless, the future ROE for Zhejiang Expressway is predicted to rise to 11% despite there being not much change expected in its payout ratio.

Conclusion

Overall, we are quite pleased with Zhejiang Expressway's performance. Specifically, we like that it has been reinvesting a high portion of its profits at a moderate rate of return, resulting in earnings expansion. With that said, the latest industry analyst forecasts reveal that the company's earnings growth is expected to slow down. Are these analysts expectations based on the broad expectations for the industry, or on the company's fundamentals? Click here to be taken to our analyst's forecasts page for the company.

Valuation is complex, but we're here to simplify it.

Discover if Zhejiang Expressway might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:576

Zhejiang Expressway

An investment holding company, invests, develops, maintains, and operates roads in the People’s Republic of China.

Undervalued with excellent balance sheet and pays a dividend.

Market Insights

Advertisement

Weekly Picks

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

109 followersusers have followed this narrative

10 commentsusers have commented on this narrative

21 likesusers have liked this narrative

TI

TibiT on Canadian National Railway ·

The Indispensable Artery for a New North American Economy

Fair Value:CA$132.870.7% overvalued

20 followersusers have followed this narrative

4 commentsusers have commented on this narrative

3 likesusers have liked this narrative

RE

RecMag on Agfa-Gevaert ·

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Fair Value:€5.3988.2% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

NI

niteco on Texas Instruments ·

Engineered for Stability. Positioned for Growth.

Fair Value:US$314.4446.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$28.1829.5% undervalued

46 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BE

Bejgal on Fiverr International ·

Fiverr International will transform the freelance industry with AI-powered growth

Fair Value:US$36.8143.1% undervalued

79 followersusers have followed this narrative

7 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

109 followersusers have followed this narrative

10 commentsusers have commented on this narrative

21 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

939 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

145 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative