- Hong Kong

- /

- Specialty Stores

- /

- SEHK:6033

Are Telecom Digital Holdings's (HKG:6033) Statutory Earnings A Good Reflection Of Its Earnings Potential?

It might be old fashioned, but we really like to invest in companies that make a profit, each and every year. However, sometimes companies receive a one-off boost (or reduction) to their profit, and it's not always clear whether statutory profits are a good guide, going forward. In this article, we'll look at how useful this year's statutory profit is, when analysing Telecom Digital Holdings (HKG:6033).

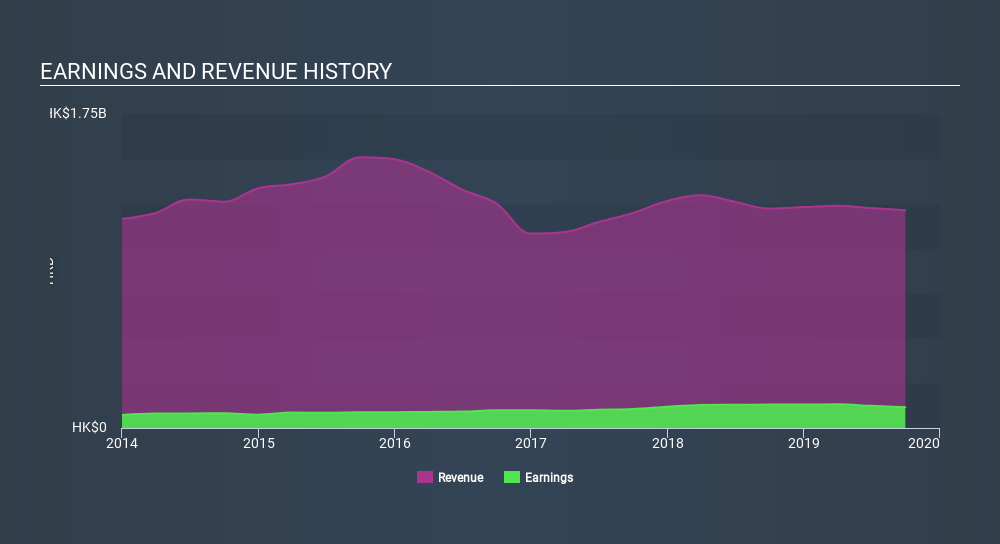

It's good to see that over the last twelve months Telecom Digital Holdings made a profit of HK$115.6m on revenue of HK$1.21b. Even though its revenue is down over the last three years, its profit has actually increased, as you can see, below.

Check out our latest analysis for Telecom Digital Holdings

Of course, it is only sensible to look beyond the statutory profits and question how well those numbers represent the sustainable earnings power of the business. As a result, we think it's well worth considering what Telecom Digital Holdings's cashflow (when compared to its earnings) can tell us about the nature of its statutory profit. Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Telecom Digital Holdings.

Examining Cashflow Against Telecom Digital Holdings's Earnings

One key financial ratio used to measure how well a company converts its profit to free cash flow (FCF) is the accrual ratio. To get the accrual ratio we first subtract FCF from profit for a period, and then divide that number by the average operating assets for the period. You could think of the accrual ratio from cashflow as the 'non-FCF profit ratio'.

That means a negative accrual ratio is a good thing, because it shows that the company is bringing in more free cash flow than its profit would suggest. While having an accrual ratio above zero is of little concern, we do think it's worth noting when a company has a relatively high accrual ratio. To quote a 2014 paper by Lewellen and Resutek, "firms with higher accruals tend to be less profitable in the future".

Telecom Digital Holdings has an accrual ratio of -0.14 for the year to September 2019. Therefore, its statutory earnings were quite a lot less than its free cashflow. In fact, it had free cash flow of HK$178m in the last year, which was a lot more than its statutory profit of HK$115.6m. Telecom Digital Holdings's free cash flow improved over the last year, which is generally good to see.

Our Take On Telecom Digital Holdings's Profit Performance

As we discussed above, Telecom Digital Holdings has perfectly satisfactory free cash flow relative to profit. Because of this, we think Telecom Digital Holdings's earnings potential is at least as good as it seems, and maybe even better! And on top of that, its earnings per share have grown at 16% per year over the last three years. The goal of this article has been to assess how well we can rely on the statutory earnings to reflect the company's potential, but there is plenty more to consider. So while earnings quality is important, it's equally important to consider the risks facing Telecom Digital Holdings at this point in time. Case in point: We've spotted 3 warning signs for Telecom Digital Holdings you should be aware of.

Today we've zoomed in on a single data point to better understand the nature of Telecom Digital Holdings's profit. But there is always more to discover if you are capable of focussing your mind on minutiae. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About SEHK:6033

Telecom Digital Holdings

An investment holding company, engages in the telecommunications and related businesses in Hong Kong and the People’s Republic of China.

Established dividend payer and good value.