Advertisement

- Hong Kong

- /

- Electronic Equipment and Components

- /

- SEHK:2498

Robosense Technology (SEHK:2498) Valuation in Focus Following New OEM Deals and LiDAR Product Launches

Simply Wall St

Reviewed by Simply Wall St

Robosense Technology (SEHK:2498) just shared its latest earnings update, and there is a lot to unpack for investors tracking this LiDAR innovator. The headlines include steady quarterly sales, a reduced net loss over nine months, and fresh momentum from new technology deals.

See our latest analysis for Robosense Technology.

Robosense Technology’s shares have seen sharp moves, rising nearly 5% in the last day and more than 7% this week. However, the past month’s share price return was a weaker -9.25%. Despite recent volatility, its total shareholder return over the past year stands at an impressive 74.63%. This reflects growing optimism as new partnerships and LiDAR product launches suggest potential for long-term growth.

If these tech-driven gains have you curious, it’s a great moment to explore other innovators riding the AI and automation trend. See the growing opportunities in our See the full list for free..

With shares still trading at more than a 40% discount to analyst price targets despite recent volatility, the question is whether Robosense Technology is currently undervalued or if the market has already factored in its future growth potential.

Most Popular Narrative: 31% Undervalued

With Robosense Technology’s last close price at HK$32.76 and the most-followed narrative assigning a fair value of HK$47.45, there is a substantial gap that is fueling bullish speculation. The current price sits well below this target as analysts factor in aggressive growth and operational shifts.

The company's rapid increase in sales of LiDAR products for robotics and non-automotive applications (up 185% in revenue and more than 5x in units sold year-over-year), along with significant gross margin improvement in this segment (from 26.1% to 45%), points to successful expansion into new growth markets like robotics and smart cities. This positions Robosense to benefit from the wider adoption of intelligent infrastructure and automation, a trend that could influence long-term revenue and margin growth.

Want to know what financial momentum justifies this sharp upside? The most popular narrative hinges on bold earnings projections, future profit benchmarks, and a margin turnaround that few expected. Find out if these ambitious forecasts could actually pan out. Dive in to see the key variables driving this valuation.

Result: Fair Value of $47.45 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, ongoing customer concentration and falling selling prices could threaten Robosense Technology’s growth if new major partnerships or margin stability do not materialize.

Find out about the key risks to this Robosense Technology narrative.

Another View: Beware High Market Valuations

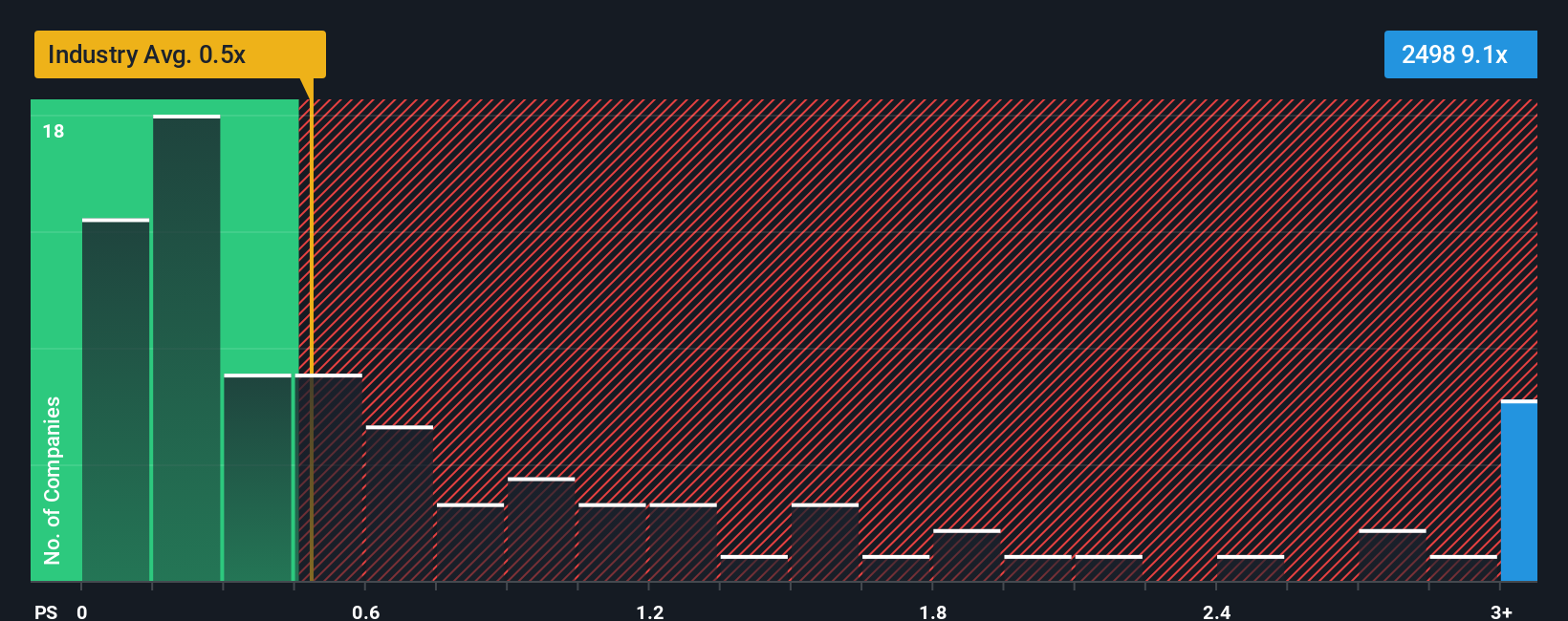

Not everyone agrees Robosense Technology is a bargain. On a sales basis, its current ratio of 8.3x looks expensive compared to both the Hong Kong Electronic industry average of just 0.5x and its peer average of 1x. The market could easily move closer to its fair ratio of 1.7x, which would mean downside risk if future growth disappoints. Can strong top-line momentum justify this hefty premium?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Robosense Technology Narrative

If you see things differently, or would rather examine the numbers firsthand, you can quickly build your own perspective in just a few minutes with our tools. Do it your way

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Robosense Technology.

Ready for More Opportunities?

Don’t limit your portfolio’s potential or risk missing tomorrow’s big winners. The market is full of dynamic growth stories and untapped value. Let’s put you ahead of the crowd.

- Grow your wealth by following these 15 dividend stocks with yields > 3% that consistently deliver strong yields and reliable income, ideal for building long-term financial security.

- Spot tomorrow’s hidden gems by checking out these 923 undervalued stocks based on cash flows set for a potential rebound based on strong fundamentals and discounted prices.

- Ride the momentum of innovation as you tap into these 25 AI penny stocks shaping the world through artificial intelligence breakthroughs and transformative new technologies.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:2498

Robosense Technology

An investment holding company, provides LiDAR and perception solutions in the People’s Republic of China and internationally.

High growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1359.3% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SW

swift11 on DXC Technology ·

CEO: We are winners in the long term in the AI world

Fair Value:US$17.4624.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25158.0% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

98 followersusers have followed this narrative

10 commentsusers have commented on this narrative

19 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative