Advertisement

- Hong Kong

- /

- Real Estate

- /

- SEHK:88

Tai Cheung Holdings (SEHK:88) Margin Compression Raises Questions Despite Revenue Growth Outpacing Market

Simply Wall St

Reviewed by Simply Wall St

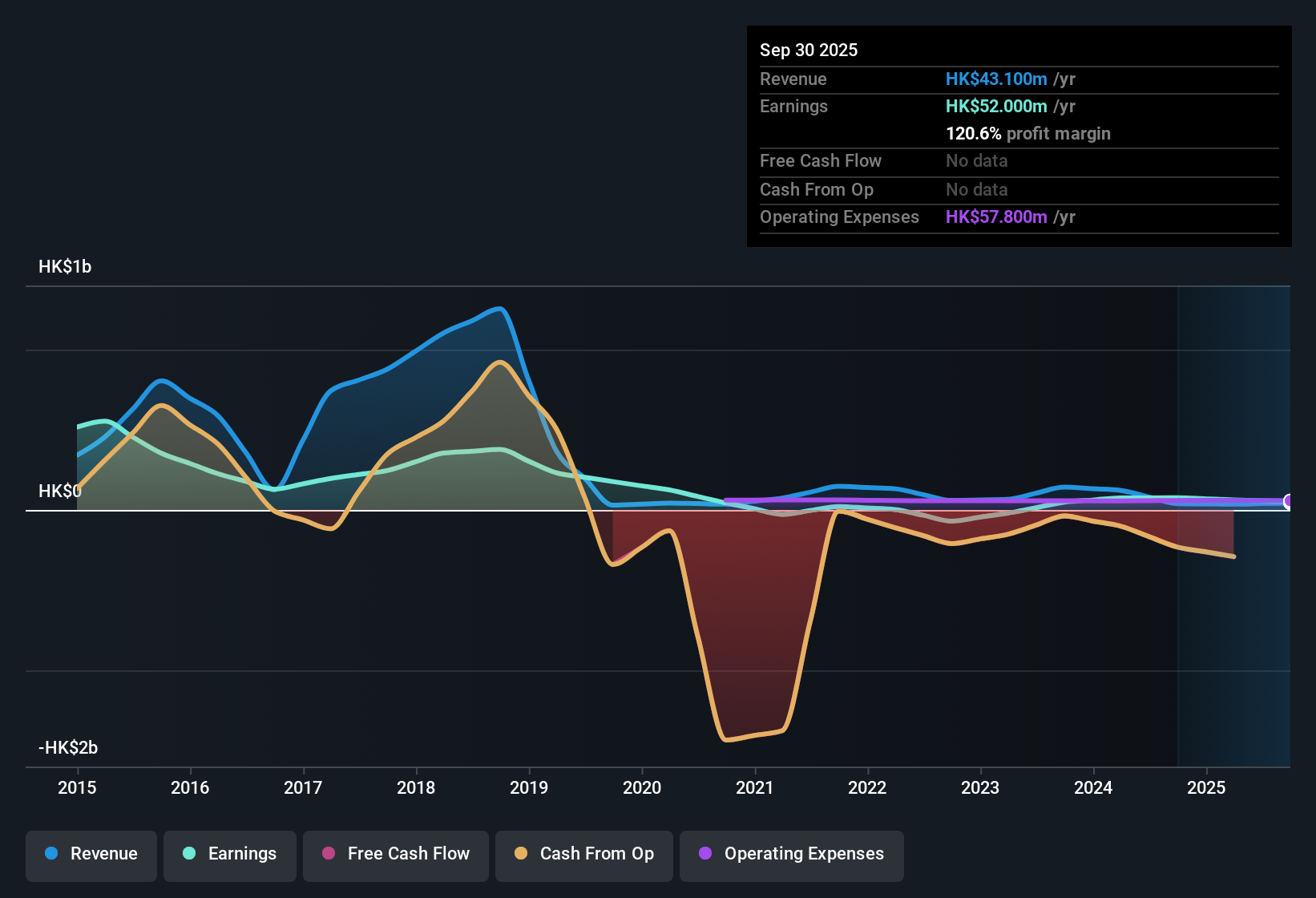

Tai Cheung Holdings (SEHK:88) posted total revenue of HK$43.1 million and basic EPS of HK$0.08462 in the trailing twelve months to H1 2026, while net income (excluding extra items) reached HK$52 million. The company has seen revenue fluctuate in recent years, with HK$27.5 million reported in the second half of 2024 and HK$39.3 million in the first half of 2025, alongside EPS moving from HK$0.063478 to HK$0.122746 over the same periods. Investors are paying close attention as profit margins appear to have compressed this period despite strong figures on the top line.

See our full analysis for Tai Cheung Holdings.The next section puts these numbers head-to-head with the main narratives investors have been debating. Let's see which stories the results confirm, and where they leave questions.

Curious how numbers become stories that shape markets? Explore Community Narratives

Profit Margin Slips Amid Revenue Surge

- Net profit margin in the trailing twelve months fell, even as revenue rose to HK$43.1 million and net income reached HK$52 million, influenced by a large one-off gain of HK$21.3 million.

- Consensus narrative notes that Tai Cheung's diversified property portfolio across Hong Kong and the US supports recurring income and resilience. However, the recent margin squeeze and earnings decline underscore ongoing sector headwinds.

- Net income excluding extra items over the last year was HK$52 million, but margins are lower compared to the previous year.

- Despite recurring revenue streams, profit sustainability may be challenged by sector volatility and the reduced influence of extraordinary items.

See how this neutral stance plays out in our full consensus breakdown. 📊 Read the full Tai Cheung Holdings Consensus Narrative.

Premium Valuation Stands Out

- Tai Cheung trades at a Price-To-Earnings Ratio of 40.4x, considerably higher than its peer average of 30.6x and the broader Hong Kong real estate industry at 14.4x.

- Critics point out that the current share price of HK$3.4 is much higher than both peer comparisons and the DCF fair value of HK$2.17, leading to concerns over whether expectations for rapid forecasted earnings growth are already reflected in the price.

- The valuation premium could limit potential upside, especially if margin pressure continues or forecasts do not materialize as anticipated.

- Persistent disparity between price and fair value places greater emphasis on sustained above-market earnings growth rates.

Dividend Payout Faces Pressure

- The company offers a 7.06% dividend yield, but this payout is not well covered by current earnings or free cash flow according to the latest risk summary.

- Although the headline yield appears attractive, concerns remain about long-term sustainability, as continued pressure on margins and earnings could prompt management to revisit future distributions.

- A payout ratio that exceeds available earnings raises questions about dividend reliability.

- Investors may wish to weigh the appeal of high yield against the elevated valuation and slimmer profit margins.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Tai Cheung Holdings's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Tai Cheung faces elevated valuation metrics and growing concerns over profit margin declines, putting its earnings reliability and future return potential in question.

If you’re keen to sidestep those overvaluation risks, consider focusing on better-priced opportunities like these 927 undervalued stocks based on cash flows, which highlights stocks backed by stronger value fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Tai Cheung Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:88

Tai Cheung Holdings

An investment holding company, engages in property investment, development, and management businesses in Hong Kong and the United States.

High growth potential with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$120.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k1.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

93 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative