Advertisement

- Hong Kong

- /

- Real Estate

- /

- SEHK:497

CSI Properties (SEHK:497): Net Loss Deepens to HK$1.34 Billion, Undercutting Turnaround Hopes

Simply Wall St

Reviewed by Simply Wall St

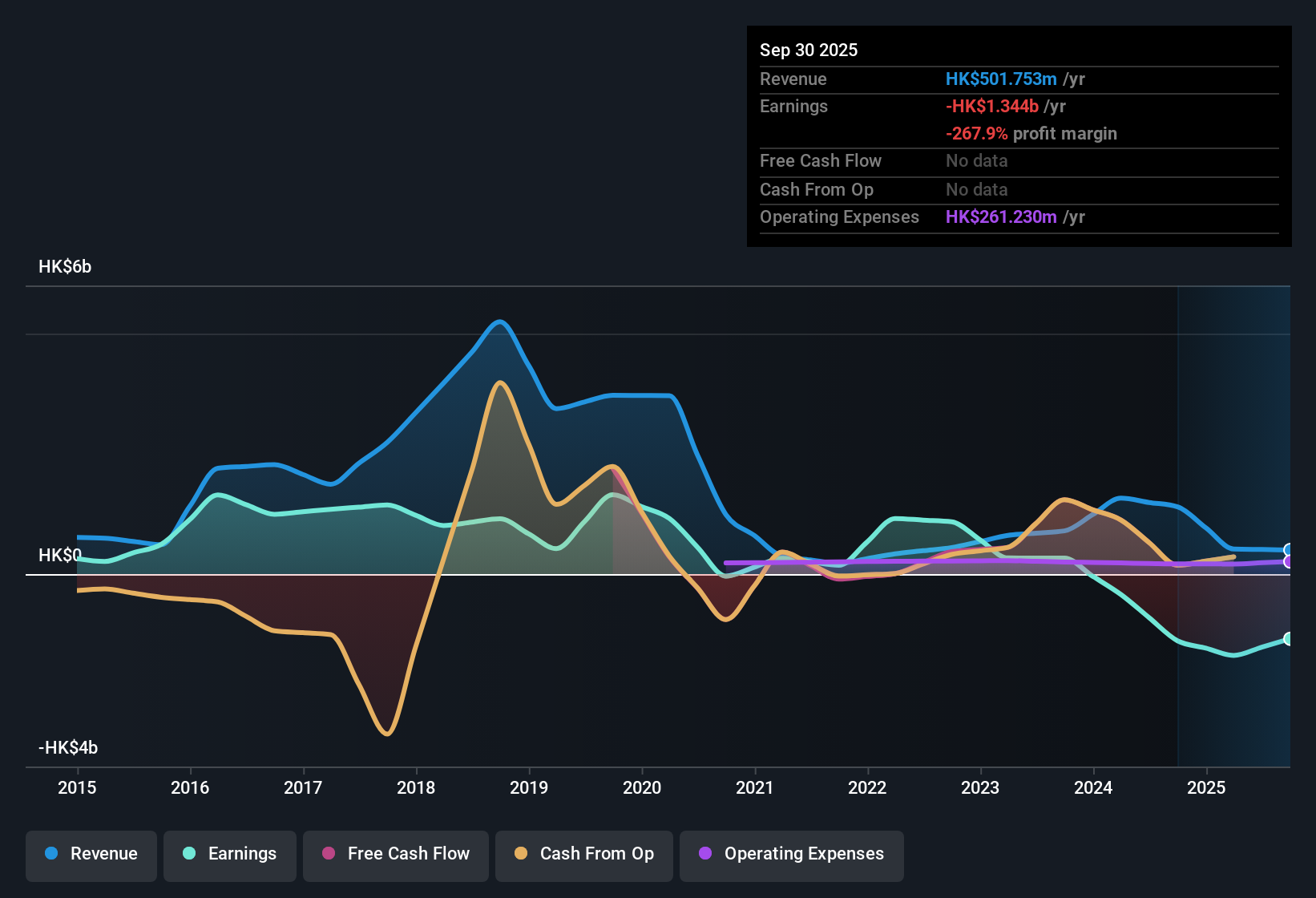

CSI Properties (SEHK:497) just posted its H1 2026 financials, reporting revenue of HK$501.8 million and a basic EPS loss of HK$0.16. The company has seen revenue move from HK$1.40 billion in H1 2025 to HK$501.8 million over the trailing twelve months, while EPS remained negative throughout. Margins have stayed deeply in the red, underscoring persistent operational challenges for investors watching this turnaround story.

See our full analysis for CSI Properties.Now let’s dig in and see how this latest performance stacks up against the main narratives simmering on Simply Wall St. Consider whether they reinforce expectations or require a fresh perspective.

Curious how numbers become stories that shape markets? Explore Community Narratives

Losses Deepen as Net Income Slides to -HK$1.34 Billion

- For the past twelve months, net income stood at negative HK$1,344.1 million, worsening from negative HK$904.1 million in H1 2025 and negative HK$1,387.3 million earlier in the year.

- Despite earlier hopes that recurring revenue from diversified properties could buffer cyclical headwinds, the ongoing losses highlight just how difficult it has been for CSI Properties to achieve stability.

- Bears point to the net loss increasing at an average rate of 60.1% per year over the last five years, reinforcing concerns about the sustainability of the business as losses mount.

- While the company maintains a geographically mixed portfolio, the consistent negative net income challenges the notion that diversification alone is enough to offset tough sector fundamentals.

Price-to-Sales Ratio Flags Valuation Challenge

- CSI’s price-to-sales ratio comes in at 4.6x, notably higher than the Hong Kong real estate industry average of 0.7x and the peer average of 2.1x.

- For investors comparing valuation metrics, the elevated ratio exposes a significant disconnect.

- Consensus narrative notes that, while the current share price of HK$0.18 trades 37.6% below the DCF fair value of HK$0.29, making the stock appear discounted, it remains expensive when viewed through traditional multiples.

- This tension between apparent value and high relative pricing prompts many to look more closely at whether operational turnaround is realistic before interpreting the stock as a bargain.

Debt Coverage Falls Short of Comfort Zone

- The company’s debt is not well covered by operating cash flow according to the most recent analysis, and recent financial periods show no signs of improvement in coverage ratios.

- General market opinion emphasizes that this ongoing stress on the balance sheet is a heightened risk.

- Substantial shareholder dilution occurred during the year, intensifying pressure on remaining shareholders and calling financial resilience into question.

- The lack of clear progress in generating operating cash flow makes debt management a persistent concern, even as management emphasizes long-term recovery themes.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on CSI Properties's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

CSI Properties' deepening net losses, weak debt coverage, and shareholder dilution highlight serious balance sheet risks and ongoing financial instability.

If financial stress like this is a concern, you can target companies with robust liquidity and lower debt by checking out solid balance sheet and fundamentals stocks screener (1934 results) before making your next move.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:497

CSI Properties

An investment holding company, engages in the property development, leasing, and investment activities in Hong Kong, Macau, and China.

Mediocre balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$120.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k1.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

93 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative