Advertisement

- Japan

- /

- Professional Services

- /

- TSE:6098

3 Asian Stocks Estimated To Be Up To 36.2% Below Intrinsic Value

Simply Wall St

Reviewed by Simply Wall St

As Asian markets navigate a landscape marked by mixed economic signals and evolving monetary policies, investors are increasingly focused on identifying opportunities that may be undervalued relative to their intrinsic worth. In this context, understanding the fundamentals of a stock becomes crucial, as it can help uncover potential value in an environment where market conditions are constantly shifting.

Top 10 Undervalued Stocks Based On Cash Flows In Asia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Xi'an NovaStar Tech (SZSE:301589) | CN¥154.08 | CN¥302.65 | 49.1% |

| Xi'an International Medical Investment (SZSE:000516) | CN¥4.73 | CN¥9.38 | 49.6% |

| Xiamen Amoytop Biotech (SHSE:688278) | CN¥81.57 | CN¥161.77 | 49.6% |

| Ningxia Building Materials GroupLtd (SHSE:600449) | CN¥13.05 | CN¥26.06 | 49.9% |

| Meitu (SEHK:1357) | HK$7.51 | HK$14.61 | 48.6% |

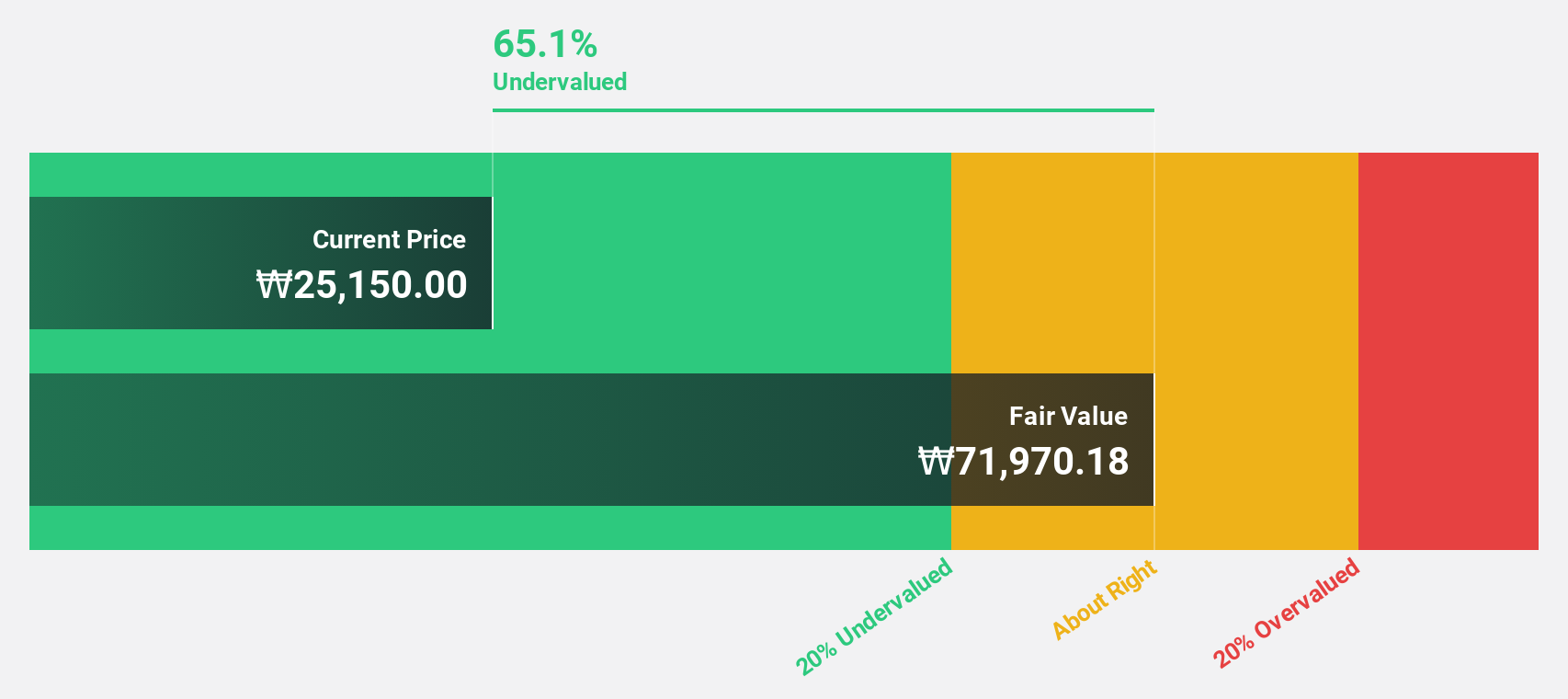

| JUSUNG ENGINEERINGLtd (KOSDAQ:A036930) | ₩29250.00 | ₩56972.54 | 48.7% |

| Japan Eyewear Holdings (TSE:5889) | ¥1975.00 | ¥3843.99 | 48.6% |

| East Buy Holding (SEHK:1797) | HK$20.42 | HK$40.27 | 49.3% |

| China Ruyi Holdings (SEHK:136) | HK$2.45 | HK$4.81 | 49.1% |

| Beijing Beimo High-tech Frictional MaterialLtd (SZSE:002985) | CN¥28.28 | CN¥55.83 | 49.3% |

We'll examine a selection from our screener results.

Hanall Biopharma (KOSE:A009420)

Overview: Hanall Biopharma Co., Ltd. is a pharmaceutical company that manufactures and sells pharmaceutical products both in South Korea and internationally, with a market cap of approximately ₩2.59 trillion.

Operations: Hanall Biopharma generates revenue through the manufacturing and sale of pharmaceutical products domestically and internationally.

Estimated Discount To Fair Value: 12%

Hanall Biopharma's recent profitability and earnings growth highlight its potential as an undervalued stock based on cash flows. Despite trading at ₩51,100, below the estimated fair value of ₩58,048.36, the discount is modest at 12%. The company reported a turnaround with net income of KRW 690.22 million for the nine months ended September 2025 compared to a loss last year. Earnings are projected to grow significantly by over 50% annually in the near term.

- Our expertly prepared growth report on Hanall Biopharma implies its future financial outlook may be stronger than recent results.

- Click here to discover the nuances of Hanall Biopharma with our detailed financial health report.

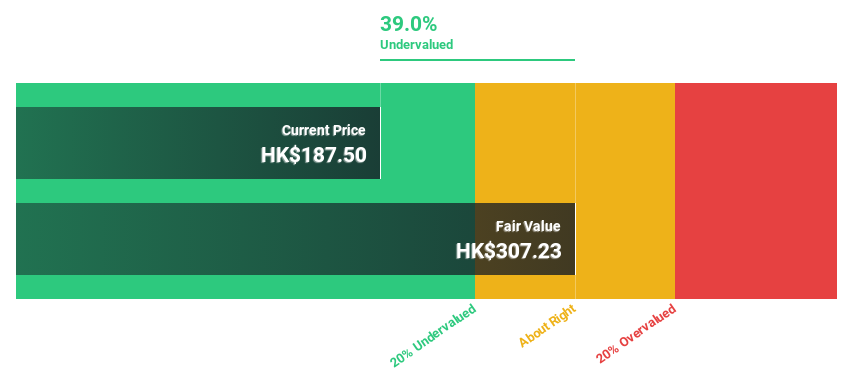

Sichuan Kelun-Biotech Biopharmaceutical (SEHK:6990)

Overview: Sichuan Kelun-Biotech Biopharmaceutical Co., Ltd. is a biopharmaceutical company focused on the R&D, manufacturing, and commercialization of novel drugs in oncology and immunology both in China and internationally, with a market cap of approximately HK$107.27 billion.

Operations: The company's revenue is derived from its pharmaceuticals segment, totaling CN¥1.50 billion.

Estimated Discount To Fair Value: 30.2%

Sichuan Kelun-Biotech Biopharmaceutical's strategic partnerships and pipeline advancements underscore its status as an undervalued stock based on cash flows. The company, trading at HK$460, is valued below its estimated fair value of HK$658.7. Recent collaborations, such as with Crescent Biopharma for oncology therapeutics development and a $185 million private placement, enhance its growth prospects. Forecasts indicate revenue growth of 36.2% annually and profitability within three years, surpassing market averages in Hong Kong.

- According our earnings growth report, there's an indication that Sichuan Kelun-Biotech Biopharmaceutical might be ready to expand.

- Take a closer look at Sichuan Kelun-Biotech Biopharmaceutical's balance sheet health here in our report.

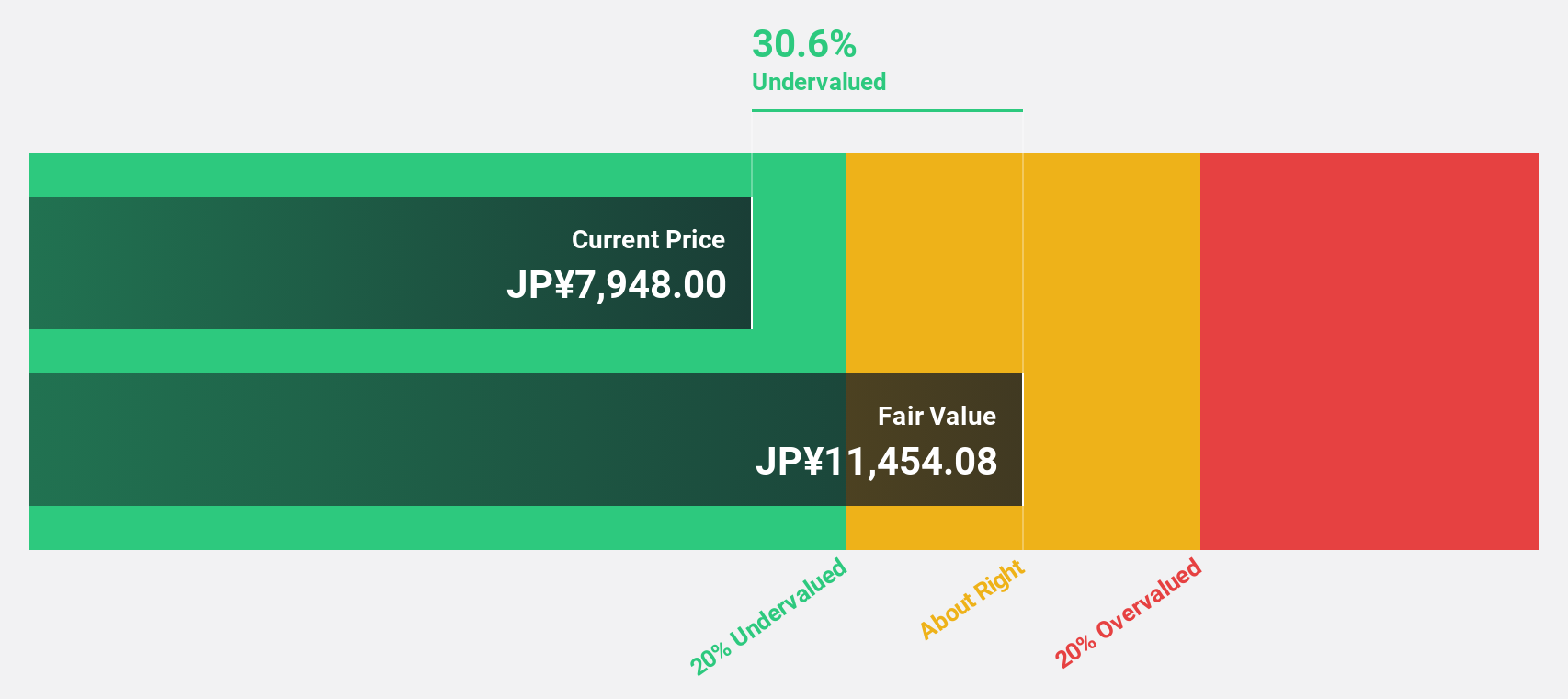

Recruit Holdings (TSE:6098)

Overview: Recruit Holdings Co., Ltd. offers HR technology and business solutions aimed at transforming the world of work, with a market cap of ¥11.67 trillion.

Operations: The company's revenue is derived from three main segments: Staffing at ¥1.66 billion, HR Technology at ¥1.26 billion, and Marketing Matching Technologies at ¥688.75 million.

Estimated Discount To Fair Value: 36.2%

Recruit Holdings is trading at ¥8,249, significantly below its estimated fair value of ¥12,922.48, highlighting its undervaluation based on cash flows. Recent guidance revisions project revenue and profit growth for the fiscal year ending March 2026. The company's share repurchase program aims to enhance shareholder returns and capital efficiency. Despite recent volatility, earnings grew by 19.6% last year and are expected to outpace the Japanese market with a forecasted annual growth of 9.9%.

- Our comprehensive growth report raises the possibility that Recruit Holdings is poised for substantial financial growth.

- Navigate through the intricacies of Recruit Holdings with our comprehensive financial health report here.

Turning Ideas Into Actions

- Investigate our full lineup of 276 Undervalued Asian Stocks Based On Cash Flows right here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:6098

Recruit Holdings

Provides HR technology and business solutions that transforms the world of work.

Outstanding track record with flawless balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

64 followersusers have followed this narrative

7 commentsusers have commented on this narrative

19 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

IN

IncomeAssets on Magma Silver ·

Silver's Breakout to over $50US will make Magma’s future shine with drill sampling returning 115g/t Silver and 2.3 g/t Gold at its Peru Mine

Fair Value:CA$0.3534.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on SEGRO ·

SEGRO's Revenue to Rise 14.7% Amidst Optimistic Growth Plans

Fair Value:UK£9.3924.7% undervalued

0 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PI

PicaCoder on Microsoft ·

After the AI Party: A Sobering Look at Microsoft's Future

Fair Value:US$42015.0% overvalued

62 followersusers have followed this narrative

12 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

118 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

958 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

64 followersusers have followed this narrative

7 commentsusers have commented on this narrative

19 likesusers have liked this narrative