Advertisement

CStone Pharmaceuticals (SEHK:2616) Is Up 9.7% After EC Approval for Sugemalimab in Lung Cancer—Has The Bull Case Changed?

Simply Wall St

Reviewed by Sasha Jovanovic

- On November 25, 2025, CStone Pharmaceuticals announced that the European Commission approved sugemalimab as a monotherapy for adult patients with unresectable stage III non-small cell lung cancer characterized by specific genetic profiles and stable disease following platinum-based chemoradiotherapy.

- This regulatory milestone not only broadens sugemalimab's reach into the European market, but also highlights the growing importance of targeted immunotherapies for difficult-to-treat cancers.

- We'll now explore how European market approval for sugemalimab could influence CStone Pharmaceuticals' investment narrative and future global opportunities.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 25 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

What Is CStone Pharmaceuticals' Investment Narrative?

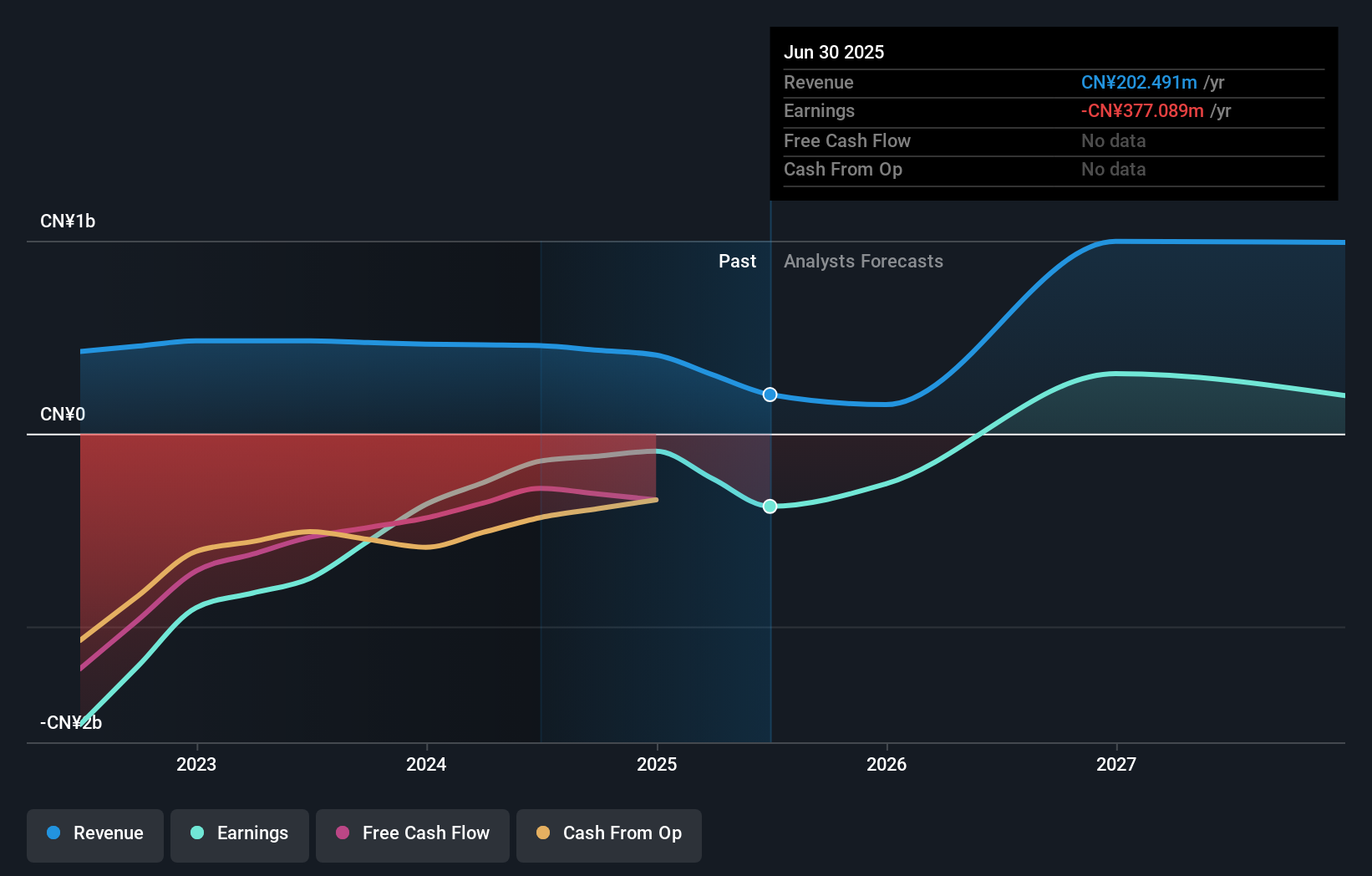

To be a CStone Pharmaceuticals shareholder right now, you need to believe in the company’s ability to translate promising drug approvals, like the recent European Commission nod for sugemalimab, into meaningful commercial traction. This milestone brings sugemalimab into the European market for a challenging lung cancer indication and could act as a catalyst for near-term sales and broader global recognition. Previously, uncertainty around monetizing the pipeline outside of China and persistent earnings losses dominated conversations about CStone’s risks. With this approval, the short-term narrative shifts toward actual market uptake and competitive positioning in Europe. However, CStone’s high Price-To-Sales ratio and continued unprofitability remain key issues, especially in light of recent share price volatility. Investors may also want to watch for execution risks in commercial rollouts and whether the anticipated revenue growth materializes.

On the flip side, the company’s significant valuation premium is something investors should be mindful of.

Exploring Other Perspectives

Explore 2 other fair value estimates on CStone Pharmaceuticals - why the stock might be worth over 3x more than the current price!

Build Your Own CStone Pharmaceuticals Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your CStone Pharmaceuticals research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free CStone Pharmaceuticals research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate CStone Pharmaceuticals' overall financial health at a glance.

Curious About Other Options?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

- These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:2616

CStone Pharmaceuticals

A biopharmaceutical company, researches and develops anti-cancer therapies to address the unmet medical needs of cancer patients in Mainland China and internationally.

High growth potential with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1359.3% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SW

swift11 on DXC Technology ·

CEO: We are winners in the long term in the AI world

Fair Value:US$17.4624.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25158.0% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

98 followersusers have followed this narrative

10 commentsusers have commented on this narrative

19 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative