Advertisement

Improved Revenues Required Before Biocytogen Pharmaceuticals (Beijing) Co., Ltd. (HKG:2315) Stock's 43% Jump Looks Justified

Biocytogen Pharmaceuticals (Beijing) Co., Ltd. (HKG:2315) shares have had a really impressive month, gaining 43% after a shaky period beforehand. This latest share price bounce rounds out a remarkable 480% gain over the last twelve months.

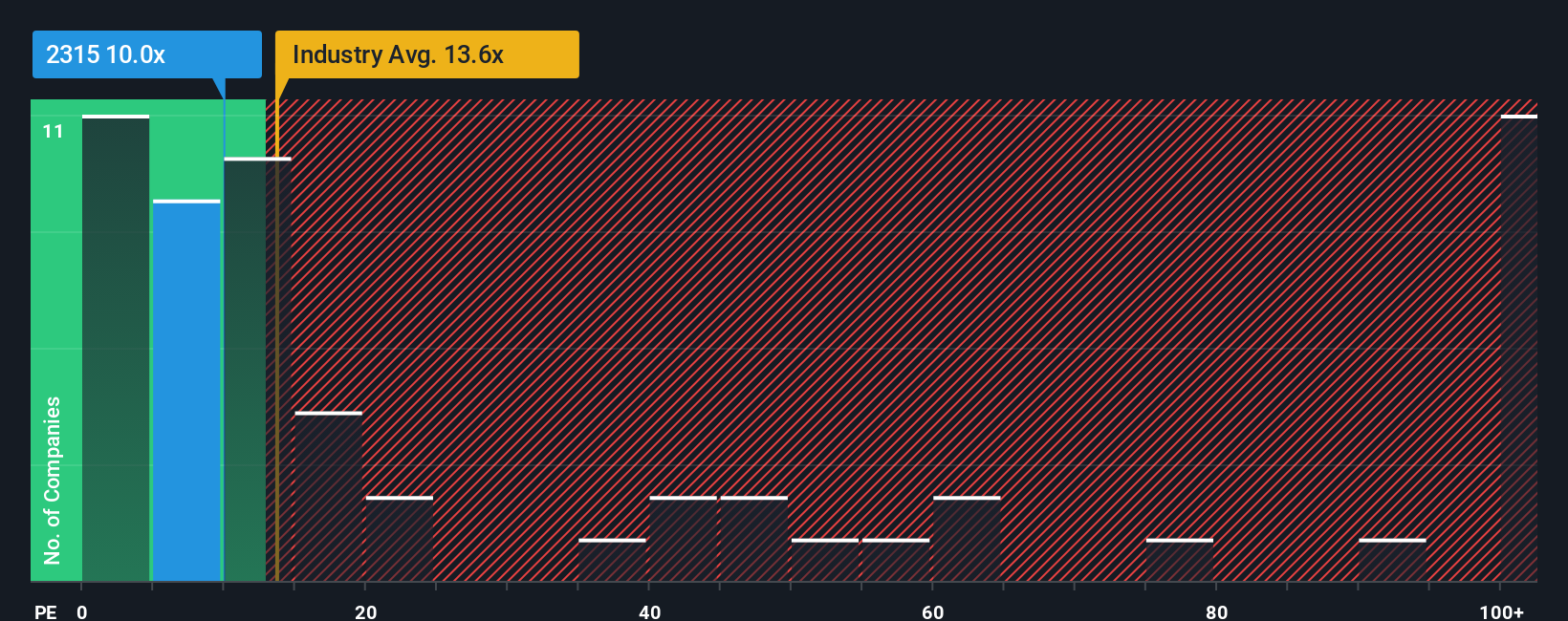

Although its price has surged higher, Biocytogen Pharmaceuticals (Beijing)'s price-to-sales (or "P/S") ratio of 10x might still make it look like a buy right now compared to the Biotechs industry in Hong Kong, where around half of the companies have P/S ratios above 13.6x and even P/S above 58x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/S.

View our latest analysis for Biocytogen Pharmaceuticals (Beijing)

What Does Biocytogen Pharmaceuticals (Beijing)'s Recent Performance Look Like?

Recent times have been quite advantageous for Biocytogen Pharmaceuticals (Beijing) as its revenue has been rising very briskly. One possibility is that the P/S ratio is low because investors think this strong revenue growth might actually underperform the broader industry in the near future. If that doesn't eventuate, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Biocytogen Pharmaceuticals (Beijing)'s earnings, revenue and cash flow.Is There Any Revenue Growth Forecasted For Biocytogen Pharmaceuticals (Beijing)?

Biocytogen Pharmaceuticals (Beijing)'s P/S ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the industry.

If we review the last year of revenue growth, the company posted a terrific increase of 49%. Pleasingly, revenue has also lifted 163% in aggregate from three years ago, thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing revenue over that time.

Comparing that to the industry, which is predicted to deliver 607% growth in the next 12 months, the company's momentum is weaker, based on recent medium-term annualised revenue results.

With this in consideration, it's easy to understand why Biocytogen Pharmaceuticals (Beijing)'s P/S falls short of the mark set by its industry peers. Apparently many shareholders weren't comfortable holding on to something they believe will continue to trail the wider industry.

What Does Biocytogen Pharmaceuticals (Beijing)'s P/S Mean For Investors?

Despite Biocytogen Pharmaceuticals (Beijing)'s share price climbing recently, its P/S still lags most other companies. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Our examination of Biocytogen Pharmaceuticals (Beijing) confirms that the company's revenue trends over the past three-year years are a key factor in its low price-to-sales ratio, as we suspected, given they fall short of current industry expectations. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises. If recent medium-term revenue trends continue, it's hard to see the share price experience a reversal of fortunes anytime soon.

We don't want to rain on the parade too much, but we did also find 1 warning sign for Biocytogen Pharmaceuticals (Beijing) that you need to be mindful of.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if Biocytogen Pharmaceuticals (Beijing) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:2315

Biocytogen Pharmaceuticals (Beijing)

A biotechnology company, engages in the research and development of novel antibody-based drugs and pre-clinical research services in the People’s Republic of China, the United States, and internationally.

Adequate balance sheet with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.4% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.0% undervalued

EA

Community Contributor