Advertisement

Simcere (SEHK:2096) Valuation Spotlight After SIM0278 Advances to Phase II Trials for Atopic Dermatitis

Simply Wall St

Reviewed by Simply Wall St

Simcere Pharmaceutical Group (SEHK:2096) has kicked off Phase II clinical trials in China for SIM0278, its IL-2 mutant fusion protein targeting moderate to severe atopic dermatitis. The new study highlights advances in selective immune therapies.

See our latest analysis for Simcere Pharmaceutical Group.

Momentum has been surging for Simcere Pharmaceutical Group lately, with the stock posting a 1-day share price return of 7.52% and an 18.01% gain over the past month. Its year-to-date share price return exceeds 100%. The 1-year total shareholder return stands at a remarkable 100.17%, reflecting strong investor appetite alongside recent progress in the company’s drug pipeline.

Looking to spot other pharma innovators with exciting developments? Explore discoveries with See the full list for free.

With excitement swirling around Simcere’s drug pipeline and shares rallying sharply this year, investors must now ask whether the company is still undervalued, or if the market has already priced in future breakthroughs.

Price-to-Earnings of 37.8x: Is it justified?

Simcere Pharmaceutical Group’s stock trades at a price-to-earnings (P/E) ratio of 37.8, significantly higher than both its industry and peer averages. At the close of HK$14.02, this high valuation raises questions about the market’s expectations for the company’s future growth.

The P/E ratio measures the price investors are willing to pay for each dollar of earnings, reflecting expectations for future profitability. For a pharmaceutical company like Simcere, a high P/E often signals confidence in strong future earnings growth or belief in the company’s innovative pipeline.

Despite optimism, Simcere’s P/E is markedly above the Hong Kong Pharmaceuticals industry average of 14.3x and the peer average of 12.9x. This suggests the stock is currently much more expensive than its rivals. Compared to the estimated fair P/E of 26.8x, the market is pricing in much more aggressive growth than what regression analysis suggests is typical for this kind of company. If these ambitious assumptions do not materialize, the valuation premium may be challenged.

Explore the SWS fair ratio for Simcere Pharmaceutical Group

Result: Price-to-Earnings of 37.8x (OVERVALUED)

However, regulatory setbacks or slower than expected clinical results could prompt a shift in sentiment and challenge Simcere’s current valuation narrative.

Find out about the key risks to this Simcere Pharmaceutical Group narrative.

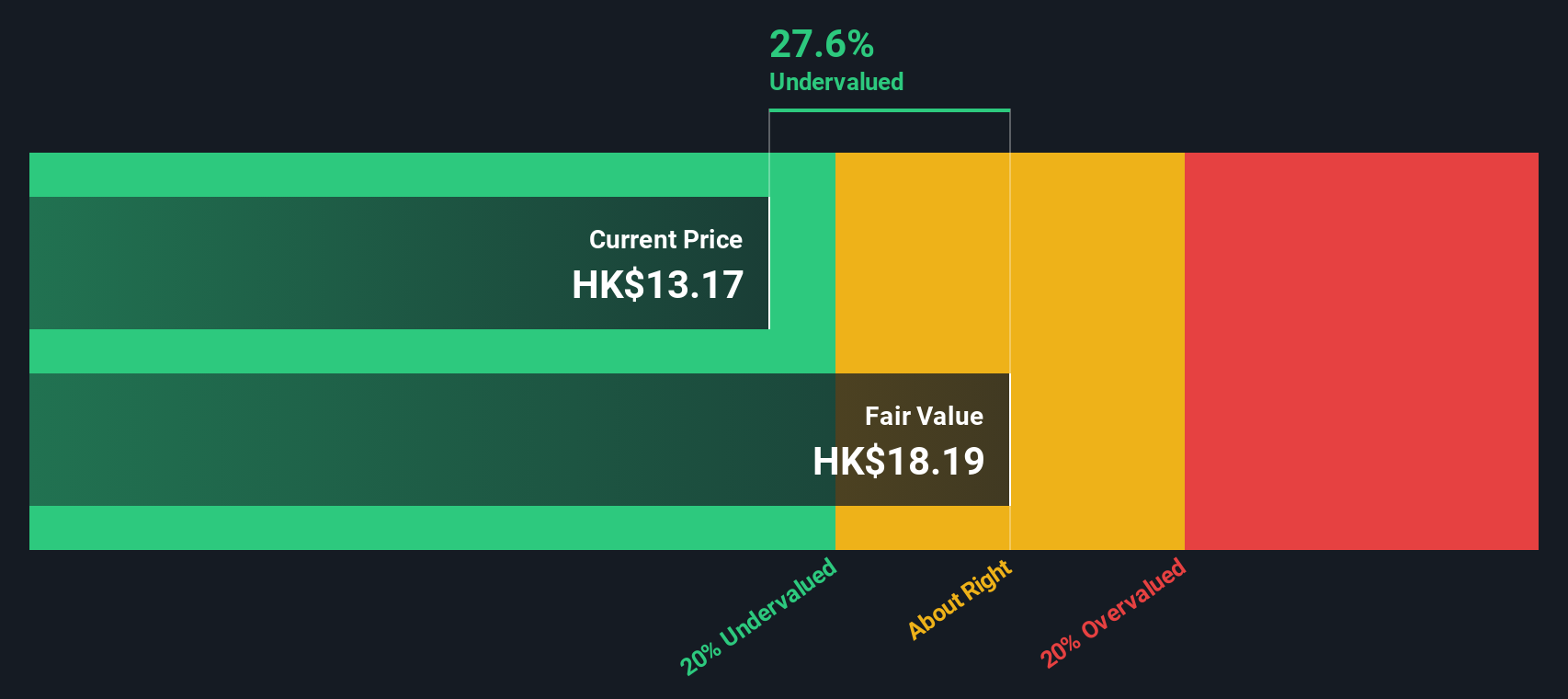

Another View: Is the Market Undervaluing Simcere?

Looking beyond earnings ratios, our DCF model estimates Simcere’s fair value at HK$18.15, about 23% above its current share price of HK$14.02. This method suggests the stock may be undervalued and challenges the story told by its high price-to-earnings ratio. Could the opportunity still be on the table?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Simcere Pharmaceutical Group for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 882 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Simcere Pharmaceutical Group Narrative

If you see the data differently or want to chart your own perspective, put your ideas to the test in just a few minutes by using Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Simcere Pharmaceutical Group.

Looking for More Standout Investment Opportunities?

Don’t let today’s momentum pass you by. With so many powerful trends shaping markets right now, you could spot your next winning stock in minutes using these handpicked tools:

- Unlock big returns by tapping into these 882 undervalued stocks based on cash flows, a selection of stocks priced below their intrinsic value, giving you an edge over the market.

- Benefit from steady income streams by checking out these 15 dividend stocks with yields > 3%, offering robust yields above 3% for long-term growth and security.

- Ride the cutting edge and get ahead of the curve with these 27 AI penny stocks, as AI transforms industries at record speed.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:2096

Simcere Pharmaceutical Group

An investment holding company, engages in the research, development, manufacture, and sale of pharmaceutical products to distributors, pharmacy chains, and other pharmaceutical manufacturers in China.

Flawless balance sheet with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.4% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.0% undervalued

EA

Community Contributor