Advertisement

- Hong Kong

- /

- Hospitality

- /

- SEHK:9922

Asian Penny Stocks To Watch In November 2025

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate a complex landscape of economic shifts and geopolitical developments, Asia's stock markets have shown resilience, with particular interest in smaller-cap stocks. Penny stocks, a term that may seem outdated but remains relevant, often represent smaller or newer companies that can offer unique growth opportunities. By focusing on those with solid financial foundations and potential for expansion, investors can uncover promising prospects amid the broader market fluctuations.

Top 10 Penny Stocks In Asia

| Name | Share Price | Market Cap | Rewards & Risks |

| JBM (Healthcare) (SEHK:2161) | HK$2.84 | HK$2.31B | ✅ 3 ⚠️ 1 View Analysis > |

| Lever Style (SEHK:1346) | HK$1.52 | HK$940.15M | ✅ 4 ⚠️ 1 View Analysis > |

| TK Group (Holdings) (SEHK:2283) | HK$2.54 | HK$2.11B | ✅ 4 ⚠️ 1 View Analysis > |

| CNMC Goldmine Holdings (Catalist:5TP) | SGD1.13 | SGD457.98M | ✅ 4 ⚠️ 2 View Analysis > |

| T.A.C. Consumer (SET:TACC) | THB4.94 | THB2.96B | ✅ 3 ⚠️ 3 View Analysis > |

| Atlantic Navigation Holdings (Singapore) (Catalist:5UL) | SGD0.10 | SGD52.35M | ✅ 2 ⚠️ 4 View Analysis > |

| Yangzijiang Shipbuilding (Holdings) (SGX:BS6) | SGD3.39 | SGD13.34B | ✅ 5 ⚠️ 1 View Analysis > |

| Anton Oilfield Services Group (SEHK:3337) | HK$1.05 | HK$2.82B | ✅ 4 ⚠️ 1 View Analysis > |

| Livestock Improvement (NZSE:LIC) | NZ$1.07 | NZ$152.31M | ✅ 2 ⚠️ 5 View Analysis > |

| Rojana Industrial Park (SET:ROJNA) | THB4.44 | THB8.97B | ✅ 3 ⚠️ 3 View Analysis > |

Click here to see the full list of 940 stocks from our Asian Penny Stocks screener.

Let's uncover some gems from our specialized screener.

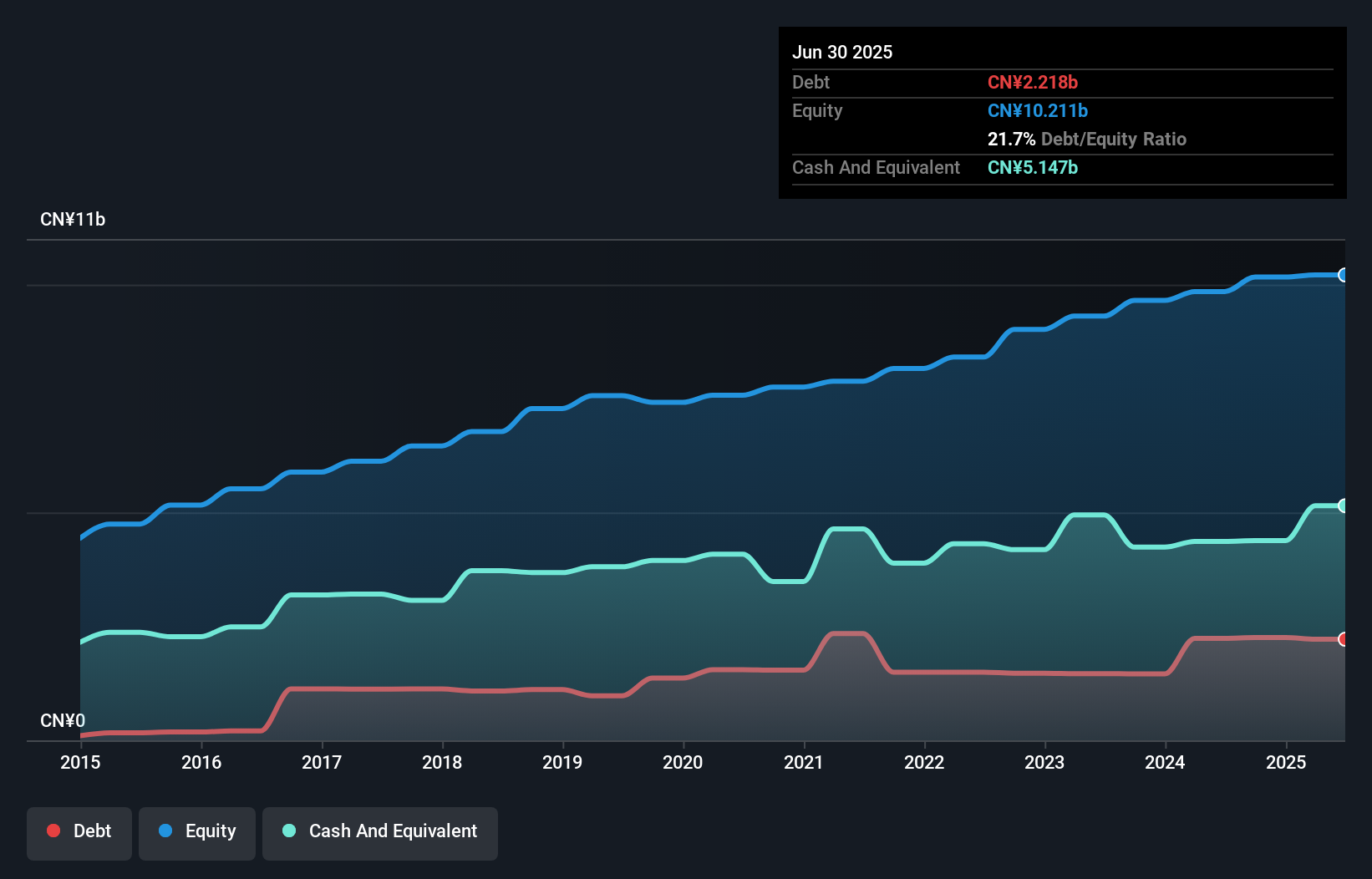

Tong Ren Tang Technologies (SEHK:1666)

Simply Wall St Financial Health Rating: ★★★★★☆

Overview: Tong Ren Tang Technologies Co. Ltd., along with its subsidiaries, is engaged in the production and distribution of Chinese medicine products in Mainland China and Hong Kong, with a market cap of HK$6.21 billion.

Operations: The company's revenue is primarily derived from its operations, with CN¥4.16 billion generated by the main entity and CN¥1.57 billion from its Chinese medicine segment.

Market Cap: HK$6.21B

Tong Ren Tang Technologies faces challenges with declining sales and net income, reporting CNY 3.74 billion in sales and CNY 338.67 million in net income for the first half of 2025, down from the previous year. Despite this, the company maintains a strong financial position with short-term assets exceeding liabilities and more cash than debt. While earnings growth has been negative recently, it is forecasted to grow at 16.4% annually. The company offers a reliable dividend yield of 4.03% and trades below its estimated fair value, though recent board changes suggest potential strategic shifts ahead.

- Get an in-depth perspective on Tong Ren Tang Technologies' performance by reading our balance sheet health report here.

- Learn about Tong Ren Tang Technologies' future growth trajectory here.

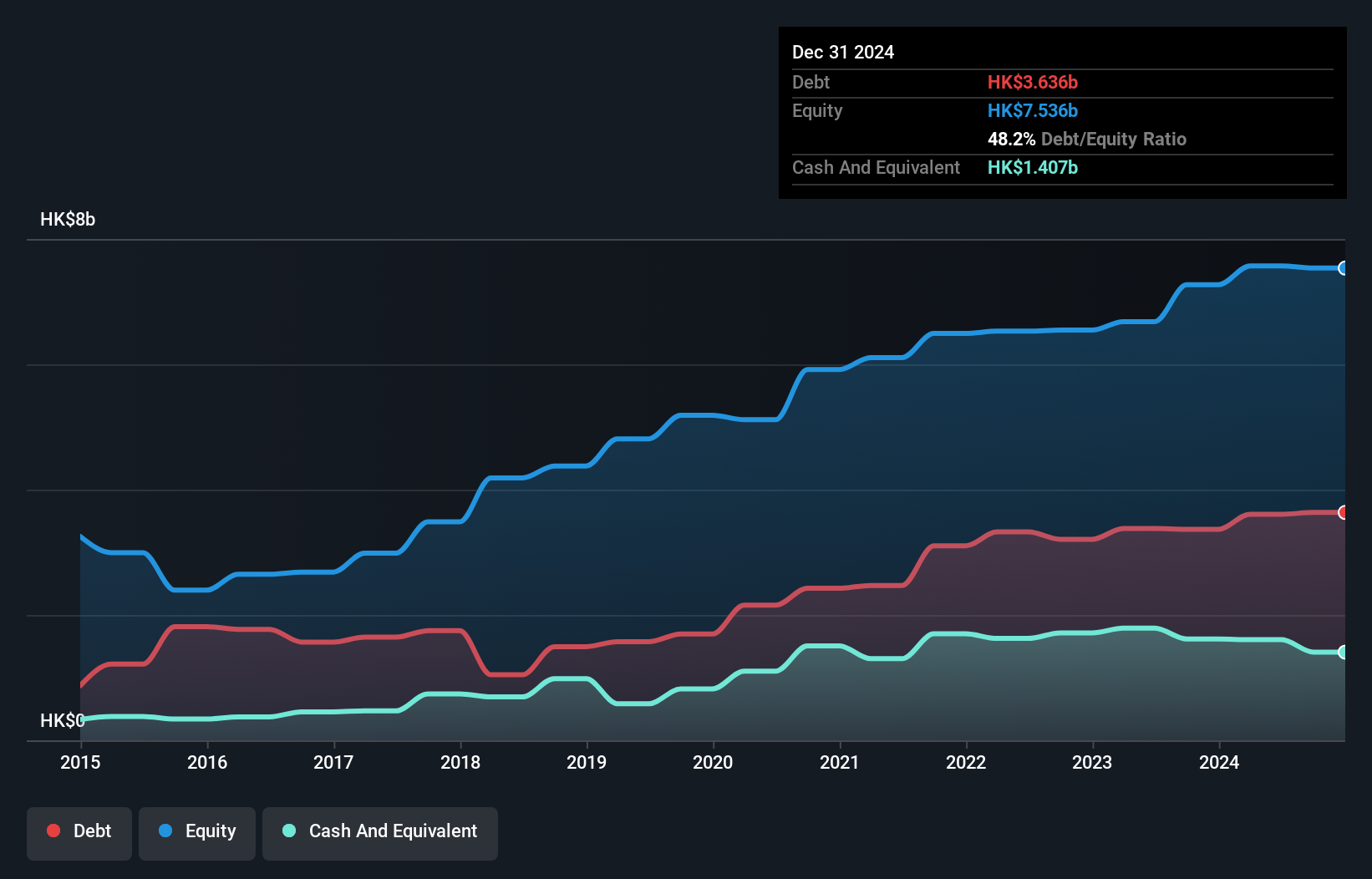

SSY Group (SEHK:2005)

Simply Wall St Financial Health Rating: ★★★★☆☆

Overview: SSY Group Limited is an investment holding company that engages in the research, development, manufacturing, trading, and sale of pharmaceutical products to hospitals and distributors both in the People’s Republic of China and internationally, with a market cap of HK$9.19 billion.

Operations: The company's revenue is primarily derived from its Intravenous Infusion Solution and Others segment, which generated HK$4.39 billion, complemented by HK$375.23 million from Medical Materials.

Market Cap: HK$9.19B

SSY Group Limited, with a market cap of HK$9.19 billion, has shown resilience despite recent declines in earnings and profit margins. The company's debt is not well covered by operating cash flow, but its short-term assets exceed both short- and long-term liabilities. Recent approvals from China's National Medical Products Administration for multiple drugs indicate potential growth avenues in the pharmaceutical sector. However, the dividend yield of 4.59% is not well supported by free cash flows, suggesting caution for income-focused investors. Despite trading at good value compared to peers, challenges remain with low return on equity and increased debt levels over five years.

- Click to explore a detailed breakdown of our findings in SSY Group's financial health report.

- Examine SSY Group's earnings growth report to understand how analysts expect it to perform.

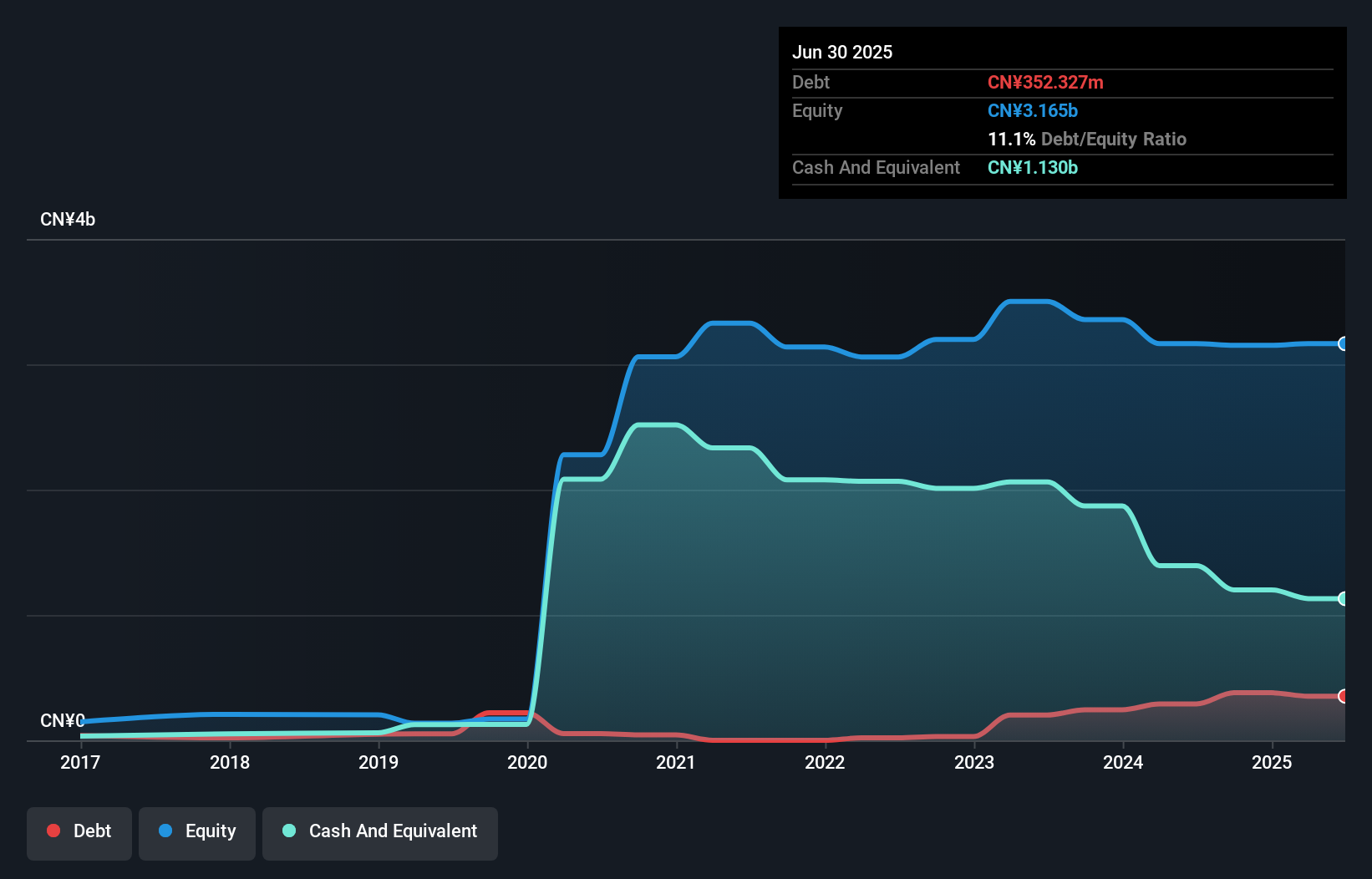

Jiumaojiu International Holdings (SEHK:9922)

Simply Wall St Financial Health Rating: ★★★★★☆

Overview: Jiumaojiu International Holdings Limited operates Chinese cuisine restaurant brands across several countries, including China, Singapore, Canada, Malaysia, the United States, Thailand, and Indonesia with a market cap of HK$2.78 billion.

Operations: The company's revenue is primarily generated from its Tai Er brand, contributing CN¥4.11 billion, followed by Song Hot Pot with CN¥880.10 million and Jiu Mao Jiu with CN¥480.30 million.

Market Cap: HK$2.78B

Jiumaojiu International Holdings, with a market cap of HK$2.78 billion, has seen its earnings affected by a large one-off loss of CN¥140.5 million over the past year. Despite this, the company maintains strong financial health with more cash than total debt and short-term assets exceeding liabilities. The recent share buyback program could enhance its net asset value and earnings per share. However, challenges persist as profit margins have declined from 4.9% to 0.8%, and return on equity remains low at 1.1%. Earnings are forecasted to grow significantly in the coming years, indicating potential recovery prospects.

- Click here to discover the nuances of Jiumaojiu International Holdings with our detailed analytical financial health report.

- Gain insights into Jiumaojiu International Holdings' outlook and expected performance with our report on the company's earnings estimates.

Make It Happen

- Jump into our full catalog of 940 Asian Penny Stocks here.

- Looking For Alternative Opportunities? Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:9922

Jiumaojiu International Holdings

Manages and operates Chinese cuisine restaurant brands in the People’s Republic of China, Singapore, Canada, Malaysia, the United States, Thailand, and Indonesia.

Excellent balance sheet with moderate growth potential.

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor