Advertisement

Asian Market Insights: JW (Cayman) Therapeutics And 2 Other Promising Penny Stocks

Simply Wall St

Reviewed by Simply Wall St

As the Asian markets continue to navigate a complex global economic landscape, investors are keenly observing opportunities that lie within smaller sectors. Penny stocks, often seen as relics of past market eras, still hold significant potential for those willing to explore smaller or newer companies with promising financial health. In this article, we will examine three penny stocks in Asia that stand out for their financial strength and growth potential.

Top 10 Penny Stocks In Asia

| Name | Share Price | Market Cap | Rewards & Risks |

| Food Moments (SET:FM) | THB3.84 | THB3.79B | ✅ 4 ⚠️ 0 View Analysis > |

| JBM (Healthcare) (SEHK:2161) | HK$2.99 | HK$2.43B | ✅ 3 ⚠️ 1 View Analysis > |

| Lever Style (SEHK:1346) | HK$1.52 | HK$940.15M | ✅ 4 ⚠️ 1 View Analysis > |

| TK Group (Holdings) (SEHK:2283) | HK$2.55 | HK$2.12B | ✅ 4 ⚠️ 1 View Analysis > |

| CNMC Goldmine Holdings (Catalist:5TP) | SGD1.16 | SGD470.14M | ✅ 4 ⚠️ 1 View Analysis > |

| T.A.C. Consumer (SET:TACC) | THB4.80 | THB2.88B | ✅ 3 ⚠️ 3 View Analysis > |

| Yangzijiang Shipbuilding (Holdings) (SGX:BS6) | SGD3.28 | SGD12.91B | ✅ 5 ⚠️ 1 View Analysis > |

| Livestock Improvement (NZSE:LIC) | NZ$0.98 | NZ$139.5M | ✅ 2 ⚠️ 5 View Analysis > |

| Rojana Industrial Park (SET:ROJNA) | THB4.78 | THB9.66B | ✅ 3 ⚠️ 3 View Analysis > |

| Lum Chang Holdings (SGX:L19) | SGD0.43 | SGD161.09M | ✅ 2 ⚠️ 2 View Analysis > |

Click here to see the full list of 963 stocks from our Asian Penny Stocks screener.

Let's review some notable picks from our screened stocks.

JW (Cayman) Therapeutics (SEHK:2126)

Simply Wall St Financial Health Rating: ★★★★★☆

Overview: JW (Cayman) Therapeutics Co. Ltd is a clinical stage cell therapy company focused on the research, development, manufacture, and marketing of cellular immunotherapy products in China with a market cap of approximately HK$1.78 billion.

Operations: The company's revenue is derived from its Pharmaceuticals segment, totaling CN¥177.75 million.

Market Cap: HK$1.78B

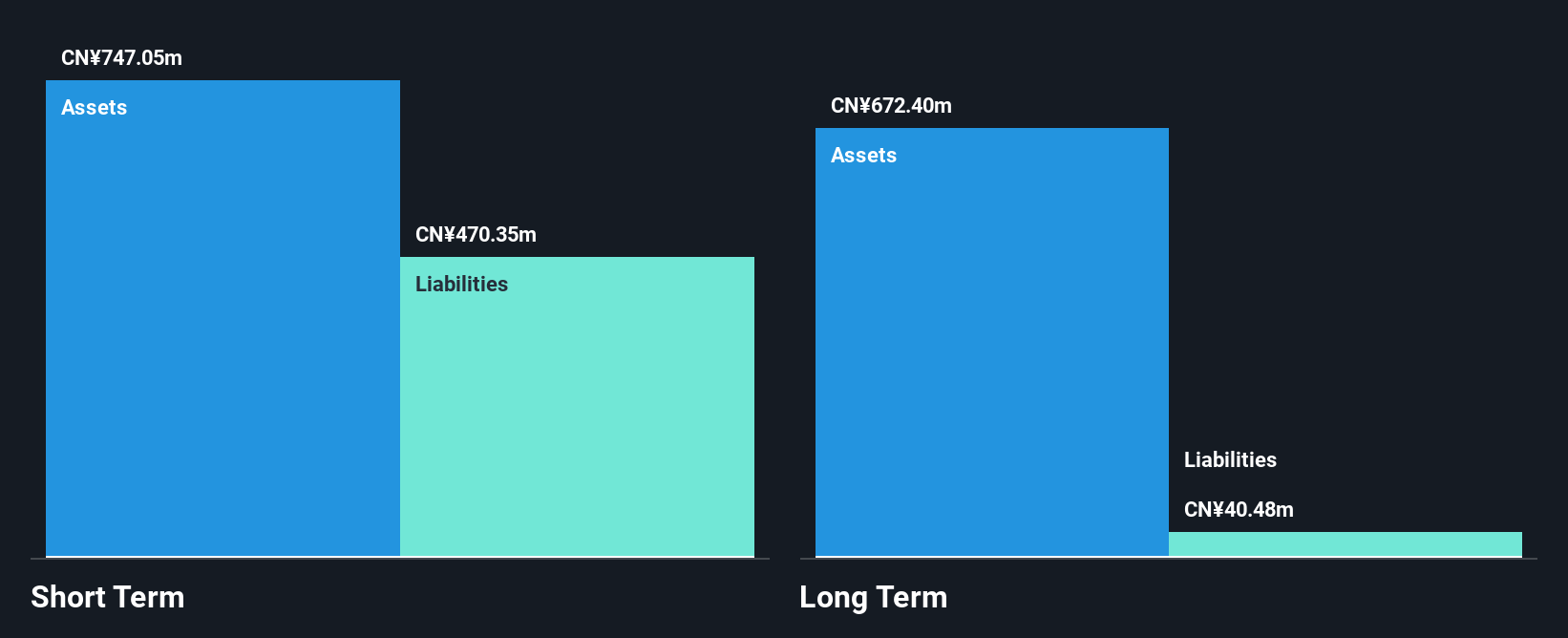

JW (Cayman) Therapeutics, a clinical stage cell therapy company, has been added to the S&P Global BMI Index, reflecting its growing recognition. Despite being unprofitable and reporting a net loss of CN¥267.27 million for the first half of 2025, the company is not pre-revenue with sales of CN¥106.35 million during this period. It maintains more cash than total debt and has sufficient cash runway for over three years based on current free cash flow. However, its share price remains highly volatile and Return on Equity is negative at -67.97%. The board's average tenure suggests inexperience with an average of 2.4 years.

- Jump into the full analysis health report here for a deeper understanding of JW (Cayman) Therapeutics.

- Evaluate JW (Cayman) Therapeutics' prospects by accessing our earnings growth report.

Broncus Holding (SEHK:2216)

Simply Wall St Financial Health Rating: ★★★★★☆

Overview: Broncus Holding Corporation is a medical device company that develops interventional pulmonology products for markets in Mainland China, the European Union, and internationally, with a market cap of HK$1.71 billion.

Operations: Broncus Holding generates revenue of $6.08 million from its medical products segment.

Market Cap: HK$1.71B

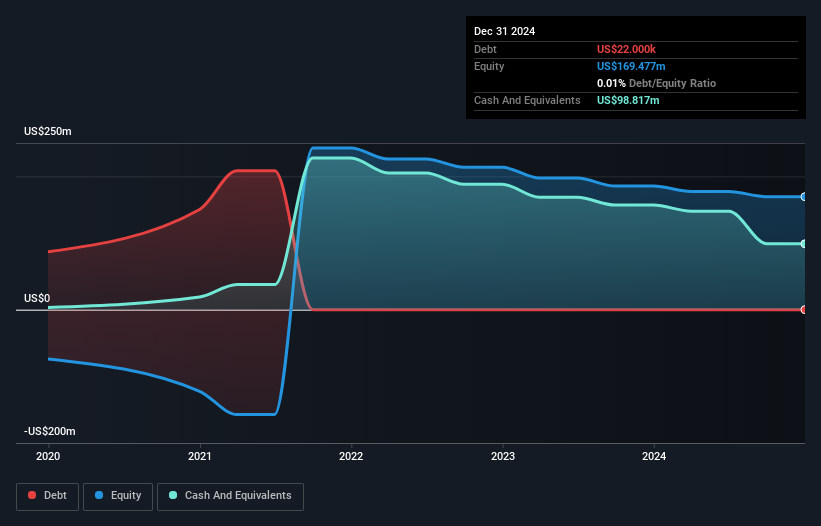

Broncus Holding has been added to the S&P Global BMI Index, signaling increased market recognition. The company reported a decline in sales to US$1.65 million for the first half of 2025, with a net loss of US$7.79 million, indicating ongoing unprofitability despite reducing losses by 43.8% annually over five years. Broncus maintains more cash than its total debt and no long-term liabilities, ensuring a stable financial position with sufficient cash runway exceeding three years based on current free cash flow. However, its share price remains highly volatile compared to peers in Hong Kong markets, and Return on Equity is negative at -9.45%.

- Navigate through the intricacies of Broncus Holding with our comprehensive balance sheet health report here.

- Examine Broncus Holding's earnings growth report to understand how analysts expect it to perform.

Delfi (SGX:P34)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: Delfi Limited is an investment holding company that manufactures, markets, distributes, and sells chocolate and confectionery products across Indonesia, the Philippines, Malaysia, Singapore, and internationally with a market cap of SGD504.20 million.

Operations: The company's revenue is primarily derived from its operations in Indonesia, contributing $331.12 million, and its Regional Markets segment, which adds $194.94 million.

Market Cap: SGD504.2M

Delfi Limited has demonstrated financial resilience with its short-term assets surpassing both long and short-term liabilities, and a reduction in debt levels over the past five years. The company's earnings are forecast to grow annually by 10.46%, though recent figures show a decline in net income from US$19.57 million to US$12.19 million year-over-year for the first half of 2025, reflecting challenges in maintaining profit margins. Delfi's dividend track record is unstable, with a recent decrease to 1 cent per share, representing half of its PATMI for the period ending June 2025.

- Take a closer look at Delfi's potential here in our financial health report.

- Understand Delfi's earnings outlook by examining our growth report.

Turning Ideas Into Actions

- Gain an insight into the universe of 963 Asian Penny Stocks by clicking here.

- Ready To Venture Into Other Investment Styles? We've found 18 US stocks that are forecast to pay a dividend yeild of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SGX:P34

Delfi

An investment holding company, manufactures, markets, distributes, and sells chocolate, chocolate confectionery, and consumer products in Indonesia, the Philippines, Malaysia, Singapore, and internationally.

Flawless balance sheet second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k2.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

80 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

46 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

91 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

927 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative