Advertisement

Valuation Check: China Resources Beer (SEHK:291) After Boardroom Overhaul and Key Leadership Appointments

Simply Wall St

Reviewed by Simply Wall St

China Resources Beer (Holdings) (SEHK:291) has announced changes to its leadership, introducing new executive directors, including a chief financial officer, as well as an independent non-executive director with an extensive background in investment banking.

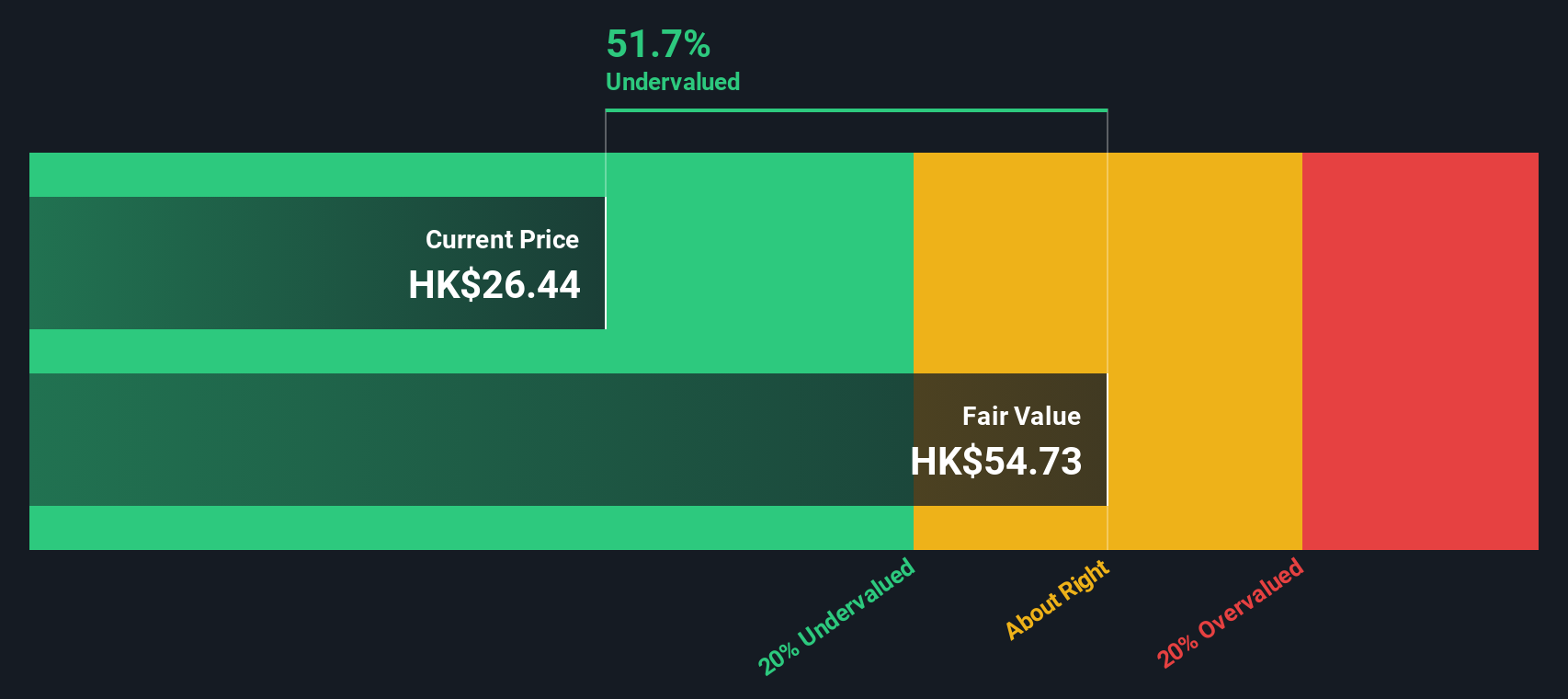

See our latest analysis for China Resources Beer (Holdings).

After a steady year marked by a 14.6% year-to-date share price return, China Resources Beer (Holdings) is showing early signs of a turnaround, supported by momentum in the past month and renewed confidence following its boardroom shakeup. However, with the share price rebounding, long-term investors may note the five-year total shareholder return remains deeply negative. This highlights the challenges of regaining lost ground even as short-term sentiment improves.

If management changes have you curious about what other opportunities are emerging, now is the perfect chance to broaden your search and discover fast growing stocks with high insider ownership

With the stock currently trading well below analyst targets and at a sizable discount to its estimated intrinsic value, investors are left wondering: is China Resources Beer truly undervalued, or has the market already priced in its recovery potential?

Price-to-Earnings of 14.1x: Is it justified?

At a price-to-earnings (P/E) ratio of 14.1x, China Resources Beer trades at a significant discount to both the Asian Beverage industry average of 19.4x and the peer group average of 29.5x. This lower valuation multiple stands out relative to its recent closing price and appears to suggest the market is underpricing the company's earnings capacity.

The price-to-earnings ratio compares a company's current share price to its per-share earnings. It serves as a gauge of investor expectations and sentiment on future profitability, especially in consumer sectors like beverages. For China Resources Beer, this multiple suggests investors may remain cautious despite visible earnings progress.

The company's earnings have grown by 11.8% over the past year, outpacing a declining industry. Management has delivered consistent profit growth over the past five years. The present P/E ratio is below both the sector and peer averages, hinting at value overlooked by the broader market. Notably, our fair ratio analysis points to an estimated “fair” P/E of 15x, a level that could be attained as sentiment recovers or operational momentum builds.

Explore the SWS fair ratio for China Resources Beer (Holdings)

Result: Price-to-Earnings of 14.1x (UNDERVALUED)

However, ongoing share price volatility and the company's lagging longer-term returns may dampen enthusiasm, especially if operational improvements do not lead to sustained market confidence.

Find out about the key risks to this China Resources Beer (Holdings) narrative.

Another View: SWS DCF Model Signals a Steeper Discount

While the market's price-to-earnings figure shows China Resources Beer as underappreciated, our SWS DCF model presents an even more dramatic picture. The model estimates fair value at HK$55.58, nearly double today’s price, which suggests a much deeper undervaluation. However, it is important to consider whether such models capture the full risks.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out China Resources Beer (Holdings) for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 920 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own China Resources Beer (Holdings) Narrative

If you see the story differently or want to reach your own conclusions, you can easily build a personalized view in just a few minutes with Do it your way.

A great starting point for your China Resources Beer (Holdings) research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Smart investors always keep an eye on new opportunities. Don’t miss out on the potential winners quietly gaining momentum and shaping the next investment wave. Get ahead with these top screeners now:

- Tap into the explosive growth in artificial intelligence by seeing these 25 AI penny stocks setting trends with machine learning and intelligent automation.

- Unlock hidden value in the market by checking out these 920 undervalued stocks based on cash flows that many investors may be overlooking right now.

- Grab lucrative passive income opportunities by browsing these 15 dividend stocks with yields > 3% offering solid yields above 3% and robust payout histories.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:291

China Resources Beer (Holdings)

An investment holding company, manufactures, distributes, and sells alcoholic beverages in Mainland China.

Very undervalued with proven track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative