Advertisement

- Hong Kong

- /

- Capital Markets

- /

- SEHK:1709

One-Off Gain Drives Profit Surge at DL Holdings Group (SEHK:1709), Challenging Quality of Earnings Narrative

Simply Wall St

Reviewed by Simply Wall St

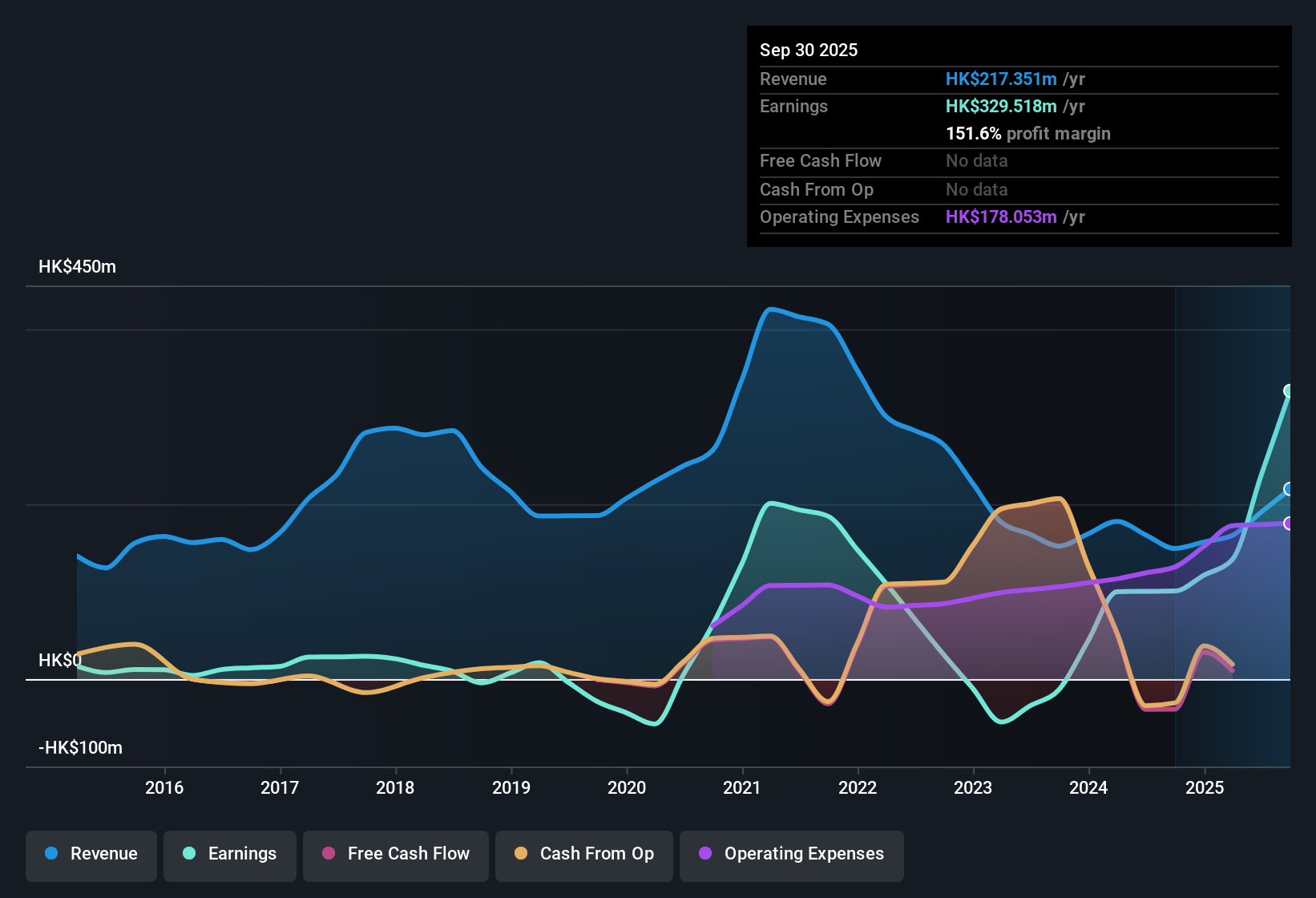

DL Holdings Group (SEHK:1709) has just posted its H1 2026 results, reporting total revenue of HK$104.2 million and basic EPS of HK$0.08796 for the period. The company has seen revenue climb from HK$89.1 million in H2 2024 to HK$104.2 million in the latest half, while EPS rose from HK$0.06501 to HK$0.08796 over the same periods. On the margins front, profitability and earnings momentum are in focus for investors watching DL Holdings Group this season.

See our full analysis for DL Holdings Group.Next, we are sizing up these fresh financials against the popular stories surrounding DL Holdings Group. Some narratives might get a boost, while others could face a rethink.

Curious how numbers become stories that shape markets? Explore Community Narratives

One-Off Gain Drives Profit Surge

- Net profit margins reached 67.5% in the last twelve months, propelled by a single, non-recurring gain of HK$194.9 million. This significantly lifted reported profitability above the five-year average growth trend of 7.2% per year.

- Market watchers note that the jump in profit largely depends on this extraordinary gain, raising questions about the sustainability of future margins:

- Analysts point out that although margins have increased rapidly, the one-off event makes it unlikely this pace will continue in the near term.

- Comparison of the HK$329.5 million trailing twelve-month net income with earlier periods highlights the substantial effect that temporary factors had on headline profits.

Valuation Stays Below Sector Average

- The price-to-earnings ratio is 15x, which is below the Hong Kong Capital Markets industry average of 21.6x. However, it remains above the average of similar peers, who are at 11.1x, placing the company’s valuation in the middle of the range.

- Some believe the lower industry multiple supports the view of fair value, while the premium over peers and the impact of non-recurring items add complexity to the value assessment:

- Some market participants see the below-industry P/E as a sign of relative opportunity, while others focus on the fact that earnings have been increased by unique, one-off items.

- Investors considering the 15x multiple may want to weigh both recent profit growth and the possibility that results could stabilize if extraordinary gains are not repeated.

Shareholder Dilution and Volatility Raise Flags

- Shareholders experienced significant dilution during the past year, coinciding with a period in which the share price was more volatile than the wider Hong Kong market.

- Current sentiment emphasizes that these risks could outweigh optimistic interpretations of headline growth:

- Critics note that while profit metrics appear strong, the risk created by additional shares and price fluctuations may impact future returns.

- The relationship between strong headline profitability and increased underlying risk is now a central consideration for investors evaluating new positions.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on DL Holdings Group's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Despite headline profit growth, concerns remain around non-recurring gains, valuation complexity, and heightened shareholder dilution. These factors introduce significant uncertainty for future performance.

If you want greater confidence in the fundamentals, check out companies with stronger cushions and steadier prospects by searching through solid balance sheet and fundamentals stocks screener (1935 results) today.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:1709

DL Holdings Group

An investment holding company, engages in the financial services of licensed business.

Proven track record with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25158.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on ANYCOLOR ·

Near zero debt, Japan centric focus provides future growth

Fair Value:JP¥7.61k15.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

95 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative