Advertisement

- Hong Kong

- /

- Hospitality

- /

- SEHK:341

Café de Coral (SEHK:341) Net Profit Margin Falls to 1.6%, Challenging Defensive Earnings Narrative

Simply Wall St

Reviewed by Simply Wall St

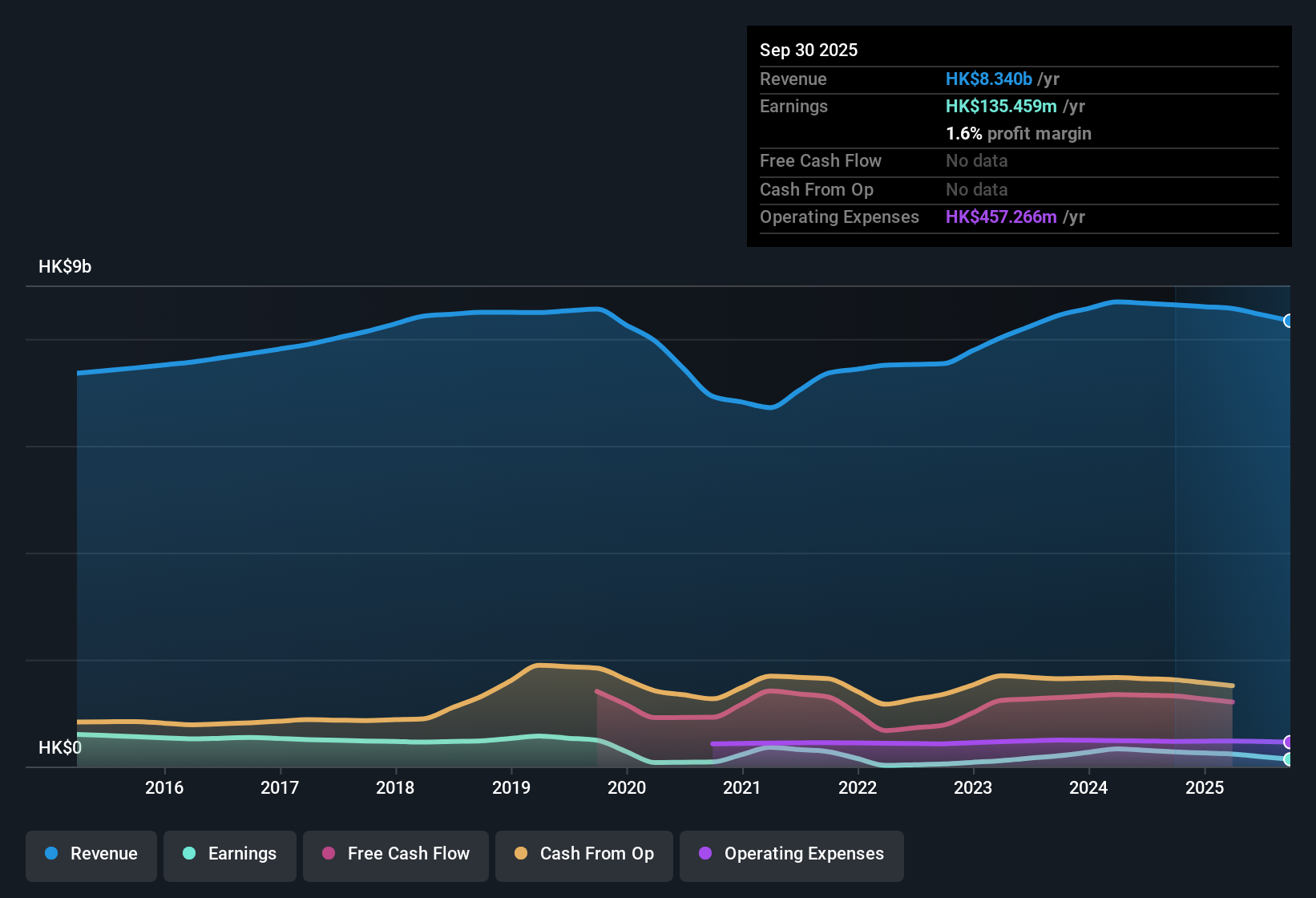

Café de Coral Holdings (SEHK:341) just released its H1 2026 results, reporting revenue of $4.3 billion HKD and EPS of 0.15 HKD. The company has seen revenue fluctuate between $4.3 billion HKD and $4.4 billion HKD over the past three half-year periods, while EPS has moved from 0.22 HKD to 0.25 HKD before settling at 0.15 HKD in the latest period. Margins compressed this time around, putting the spotlight on how investors weigh near-term profitability in relation to future growth potential.

See our full analysis for Café de Coral Holdings.Next, we will see how these headline results compare to the most popular narratives and expectations, as well as which market stories hold up in the face of the numbers.

Curious how numbers become stories that shape markets? Explore Community Narratives

Net Profit Margin Drops to 1.6%

- Net profit margin fell to 1.6% for the trailing twelve months, down from 3.2% in the previous year. This decline was mainly due to a one-off loss of HK$76.3 million that weighed on reported profits.

- While bulls highlight Café de Coral’s defensive positioning and diversified income streams as support for earnings resilience,

- the margin drop and non-recurring losses directly challenge the bullish view that stable demand alone is sufficient to support robust profitability through challenging periods.

- Bulls often point to the company’s brand strength and exposure to everyday dining. However, this year’s margin compression demonstrates that operational risks and one-time costs can undermine even well-established defensive strategies.

Shares Trade 30.8% Below DCF Fair Value

- Despite the trailing margin setback, Café de Coral shares recently traded at HK$5.65, which is a 30.8% discount to DCF fair value of HK$8.16 and well below the sector's average price-to-earnings multiple.

- The prevailing market view suggests that the deep discount could attract value-focused investors,

- but a higher-than-peer price-to-earnings ratio of 23.9x, compared to 22.1x for peers and 16.1x for the Hong Kong hospitality sector, prompts some to wonder if much of the growth optimism is already reflected in the price.

- Share price levels alone are not telling the whole story. Investors weighing discounted valuations must also consider recent profit pressures and limited dividend coverage.

Earnings Growth Forecast Beats Market

- Analyst forecasts indicate that Café de Coral’s earnings are expected to rise at 25.74% per year, outpacing the broader Hong Kong market estimate of 11.7% annual growth, even as revenue growth is projected at just 3.6% per year compared to the market’s 8.5%.

- Consensus narrative points to a balancing act: robust earnings growth could fuel optimism for a turnaround,

- but relatively subdued top-line expansion and the need for margin recovery mean execution on growth expectations, not just forecasts, will be key to changing investor conviction.

- This tension keeps longer-term momentum in play, but with increased near-term scrutiny on how quickly improvements materialize.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Café de Coral Holdings's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Café de Coral’s compressed margins and recent one-off losses highlight challenges with consistent profitability and reliable earnings growth.

If steady results matter more to you, use our stable growth stocks screener (2076 results) to focus on companies that have proven they can deliver reliable, sustained performance through every cycle.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:341

Café de Coral Holdings

An investment holding company, engages in the operation of quick service restaurants and casual dining chains in Hong Kong and Mainland China.

Adequate balance sheet second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$120.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k1.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

93 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative