Advertisement

- Hong Kong

- /

- Consumer Services

- /

- SEHK:1851

The Return Trends At China Gingko Education Group (HKG:1851) Look Promising

If we want to find a stock that could multiply over the long term, what are the underlying trends we should look for? Amongst other things, we'll want to see two things; firstly, a growing return on capital employed (ROCE) and secondly, an expansion in the company's amount of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. Speaking of which, we noticed some great changes in China Gingko Education Group's (HKG:1851) returns on capital, so let's have a look.

Understanding Return On Capital Employed (ROCE)

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. The formula for this calculation on China Gingko Education Group is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

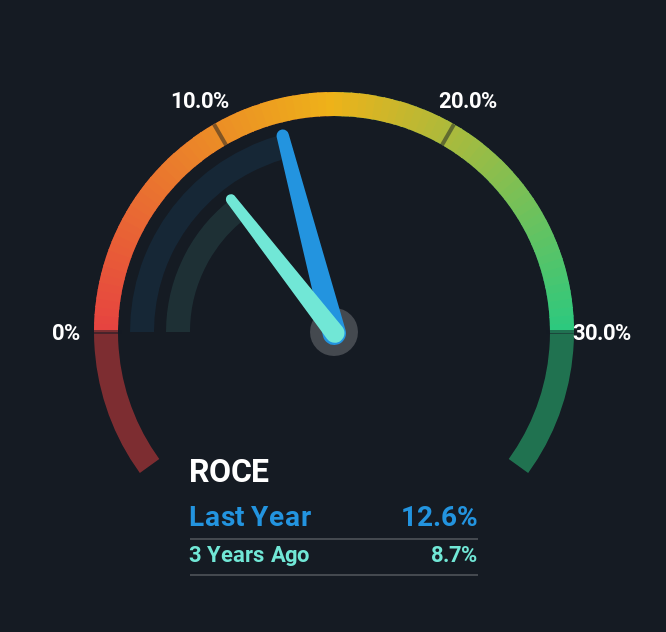

0.13 = CN¥149m ÷ (CN¥1.4b - CN¥201m) (Based on the trailing twelve months to June 2025).

Thus, China Gingko Education Group has an ROCE of 13%. On its own, that's a standard return, however it's much better than the 9.6% generated by the Consumer Services industry.

See our latest analysis for China Gingko Education Group

Historical performance is a great place to start when researching a stock so above you can see the gauge for China Gingko Education Group's ROCE against it's prior returns. If you want to delve into the historical earnings , check out these free graphs detailing revenue and cash flow performance of China Gingko Education Group.

What Can We Tell From China Gingko Education Group's ROCE Trend?

The trends we've noticed at China Gingko Education Group are quite reassuring. Over the last five years, returns on capital employed have risen substantially to 13%. The amount of capital employed has increased too, by 28%. This can indicate that there's plenty of opportunities to invest capital internally and at ever higher rates, a combination that's common among multi-baggers.

What We Can Learn From China Gingko Education Group's ROCE

In summary, it's great to see that China Gingko Education Group can compound returns by consistently reinvesting capital at increasing rates of return, because these are some of the key ingredients of those highly sought after multi-baggers. Astute investors may have an opportunity here because the stock has declined 49% in the last five years. That being the case, research into the company's current valuation metrics and future prospects seems fitting.

On a separate note, we've found 1 warning sign for China Gingko Education Group you'll probably want to know about.

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1851

China Gingko Education Group

An investment holding company, provides private higher education services in the People's Republic of China.

Adequate balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor