Advertisement

- Hong Kong

- /

- Trade Distributors

- /

- SEHK:1142

E&P Global Holdings (SEHK:1142): Net Losses Deepen, Reinforcing Bearish Market Sentiment

Simply Wall St

Reviewed by Simply Wall St

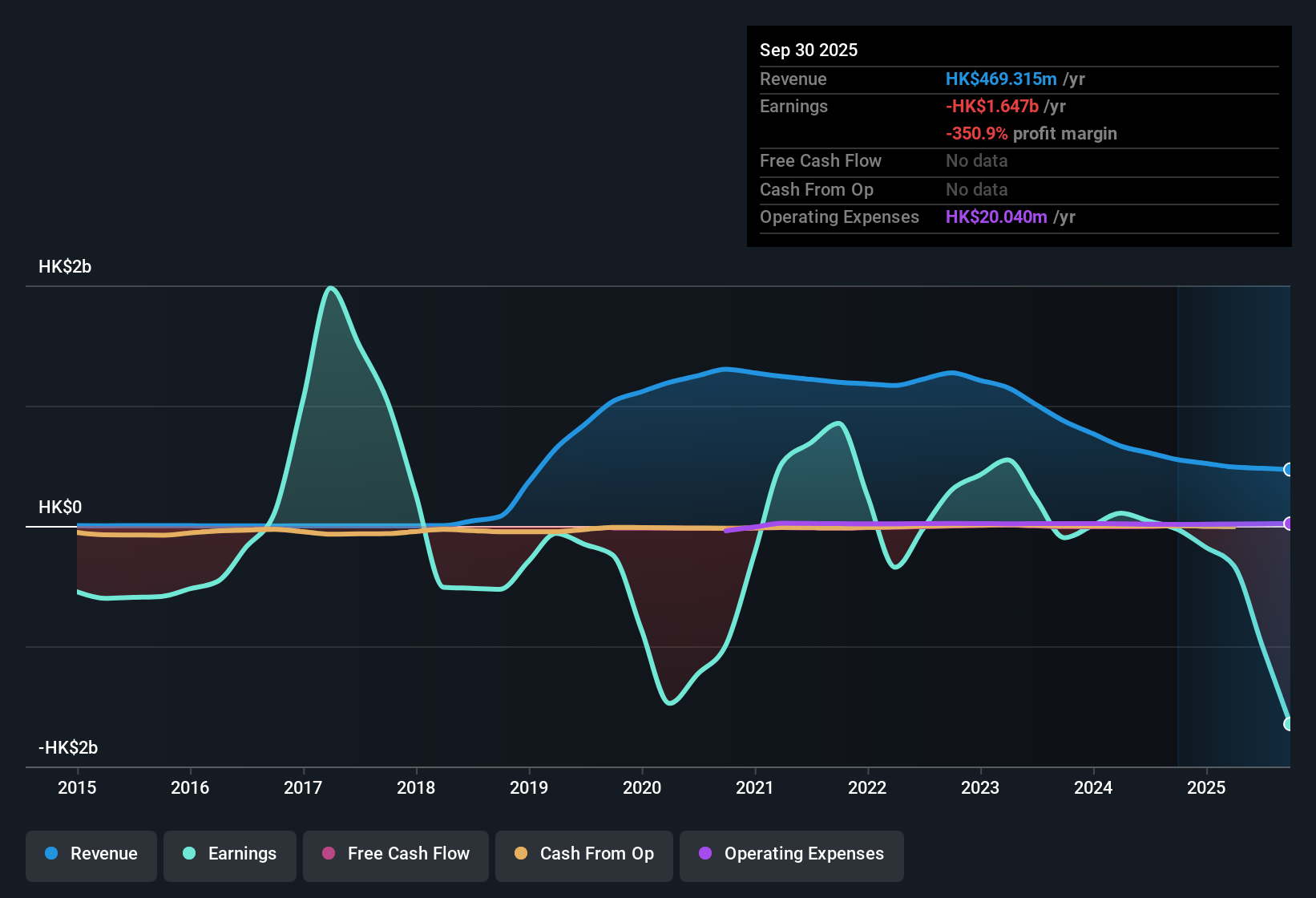

E&P Global Holdings (SEHK:1142) just released its H1 2026 financial results, reporting total revenue of 469.3 million HKD and basic EPS of -0.85 HKD. Looking back, the company's revenue moved from 551.8 million HKD in H1 2025 to 489.4 million HKD in H2 2025, with EPS shifting from -0.19 HKD to -2.27 HKD across those periods. Margins continued to compress, with sustained losses weighing on this latest set of results.

See our full analysis for E&P Global Holdings.Next, we will see how these headline numbers stack up against the prevailing narratives and expectations in the market. Some views could be reinforced, while others might get a reality check.

Curious how numbers become stories that shape markets? Explore Community Narratives

Losses Accelerate: Five-Year Net Income Downtrend

- Over the last five years, E&P Global Holdings’ net income losses widened at a steep annual rate of 39.3%, showing no sign of an earnings turnaround. Net income (excluding extra items) dropped from HKD -93.9 million in H1 2025 to HKD -235.2 million in H2 2025.

- What stands out in the prevailing market analysis is the absence of margin stabilization, as persistent negative net income and declining profit margins overshadowed any improvement.

- The company’s sustained losses, combined with negative shareholders’ equity, point to a heavy risk backdrop rather than a cyclical dip that might attract contrarian bulls.

- Consensus narrative highlights the steady erosion of profitability, signaling that market participants are likely focused on whether these structural losses can be controlled before considering any fundamental re-rating.

Relative Valuation: Price-to-Sales vs. Peers

- E&P Global Holdings trades at a Price-to-Sales ratio of 8.6x, which is both substantially higher than the Hong Kong Trade Distributors industry average of 0.6x and notably lower than the peer average of 14.6x.

- Market watchers note this premium P/S multiple casts doubt on value for risk, especially when set against ongoing net losses and sector volatility.

- While bulls might try to justify a higher multiple by pointing to direct peers, critics emphasize that the broader industry trades much cheaper, suggesting the company’s valuation is not supported by underlying profitability.

- This pricing tension underpins the lack of investor confidence in the face of repeated net losses, highlighted further by the absence of forward guidance or positive catalysts.

Shareholder Dilution and Volatility Undercut Value

- Significant shareholder dilution was reported during the last year, alongside a highly volatile share price that moved more aggressively than the broader Hong Kong market.

- Bears argue this combination is especially damaging to ongoing value, as both financial risk and share price instability discourage patient capital.

- Share dilution exacerbates losses for existing investors, compounding the negative impact of unprofitability and negative equity.

- High volatility may deter long-term holders, especially when no positive drivers for stability or recovery have emerged over the last twelve months.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on E&P Global Holdings's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Ongoing net losses, a deteriorating balance sheet, and significant shareholder dilution highlight persistent financial instability for E&P Global Holdings.

If you'd rather seek companies with stronger financial footing, use our solid balance sheet and fundamentals stocks screener (1939 results) to discover businesses built on healthier balance sheets and more resilient fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if E&P Global Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:1142

E&P Global Holdings

An investment holding company, engages in the trading of diesel, gasoline, and other related petroleum products and services in the Republic of Korea.

Slight risk with imperfect balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

138 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

931 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative