Advertisement

Woori Technology Investment And 2 Other Undiscovered Gems In Asia

Simply Wall St

Reviewed by Simply Wall St

In the current landscape, Asian markets are capturing attention as small-cap stocks gain momentum amidst cooling labor markets and ongoing trade discussions. With global indices showing signs of resilience, investors are increasingly on the lookout for promising opportunities in Asia's dynamic economic environment. Identifying a good stock often involves assessing companies that can navigate these macroeconomic shifts effectively, leveraging unique growth potential while maintaining robust fundamentals.

Top 10 Undiscovered Gems With Strong Fundamentals In Asia

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Ve Wong | 11.74% | 0.90% | 4.16% | ★★★★★★ |

| Shenzhen iN-Cube Automation | NA | 1.75% | -15.44% | ★★★★★★ |

| Xiangyang Changyuandonggu Industry | 35.39% | 2.07% | -13.74% | ★★★★★★ |

| Zhejiang Haisen Pharmaceutical | NA | 4.06% | 9.83% | ★★★★★★ |

| Neosem | 1.48% | 23.75% | 22.84% | ★★★★★★ |

| Tohoku Steel | NA | 5.34% | -2.26% | ★★★★★★ |

| Hong Tai Electric Industrial | 2.14% | 8.92% | 1.39% | ★★★★★☆ |

| Jinsanjiang (Zhaoqing) Silicon Material | 3.59% | 18.23% | -7.68% | ★★★★★☆ |

| Wuxi Huadong Heavy Machinery | 8.60% | -53.47% | 3.40% | ★★★★★☆ |

| Sinomag Technology | 68.80% | 16.08% | 3.66% | ★★★★☆☆ |

Let's uncover some gems from our specialized screener.

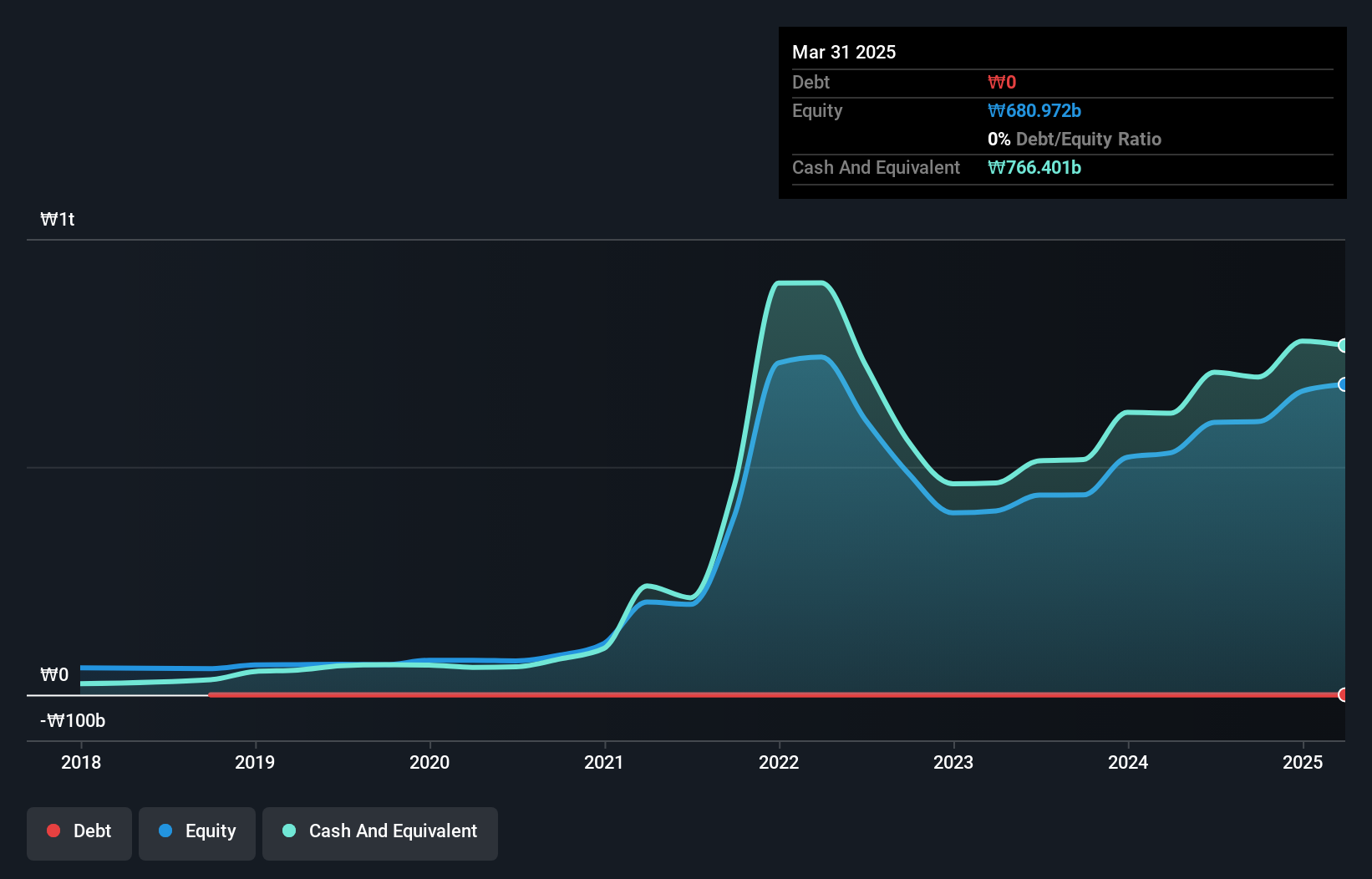

Woori Technology Investment (KOSDAQ:A041190)

Simply Wall St Value Rating: ★★★★★★

Overview: Woori Technology Investment Co., Ltd. is a venture capital firm that focuses on venture funds, mezzanine funds, project funds, and investments in small and medium-sized companies, with a market cap of ₩735.88 billion.

Operations: Woori Technology Investment generates revenue primarily from its financial services segment, amounting to ₩1.91 billion. The firm's market cap stands at ₩735.88 billion, reflecting its position in the venture capital industry.

Woori Technology Investment, a nimble player in the financial sector, stands out with its debt-free status and high-quality earnings. Despite trading at 66% below estimated fair value, it faces challenges with earnings declining by 2.6% annually over five years. The company has shown resilience by maintaining positive free cash flow recently, although revenue remains modest at ₩2 billion. While its recent annual growth of 21% lags behind the industry’s 41%, Woori's profitability ensures a stable cash runway without debt concerns, suggesting potential for value seekers willing to navigate its mixed performance landscape.

Harbin Electric (SEHK:1133)

Simply Wall St Value Rating: ★★★★★☆

Overview: Harbin Electric Company Limited, along with its subsidiaries, is involved in the manufacturing and sale of power plant equipment across various regions including China, Asia, Africa, Europe, and the United States with a market capitalization of approximately HK$12.97 billion.

Operations: The company's primary revenue stream is derived from its "New Power System With New Energy As The Main Body" segment, contributing CN¥31.38 billion. Other significant segments include "Clean and Efficient Industrial Systems" at CN¥4.74 billion and "Other businesses" at CN¥6.72 billion.

Harbin Electric, a promising player in the electrical sector, has shown impressive earnings growth of 193% over the past year, outpacing its industry peers. The company trades at a favorable price-to-earnings ratio of 7x compared to Hong Kong's market average of 11.2x, suggesting good relative value. Its debt management is noteworthy with a reduction from 39% to 35% in the debt-to-equity ratio over five years. Recent board changes include appointing Mr. Du Xing-kai as an executive director without remuneration, reflecting strategic leadership adjustments as they prepare for future growth opportunities and challenges.

- Click here to discover the nuances of Harbin Electric with our detailed analytical health report.

Understand Harbin Electric's track record by examining our Past report.

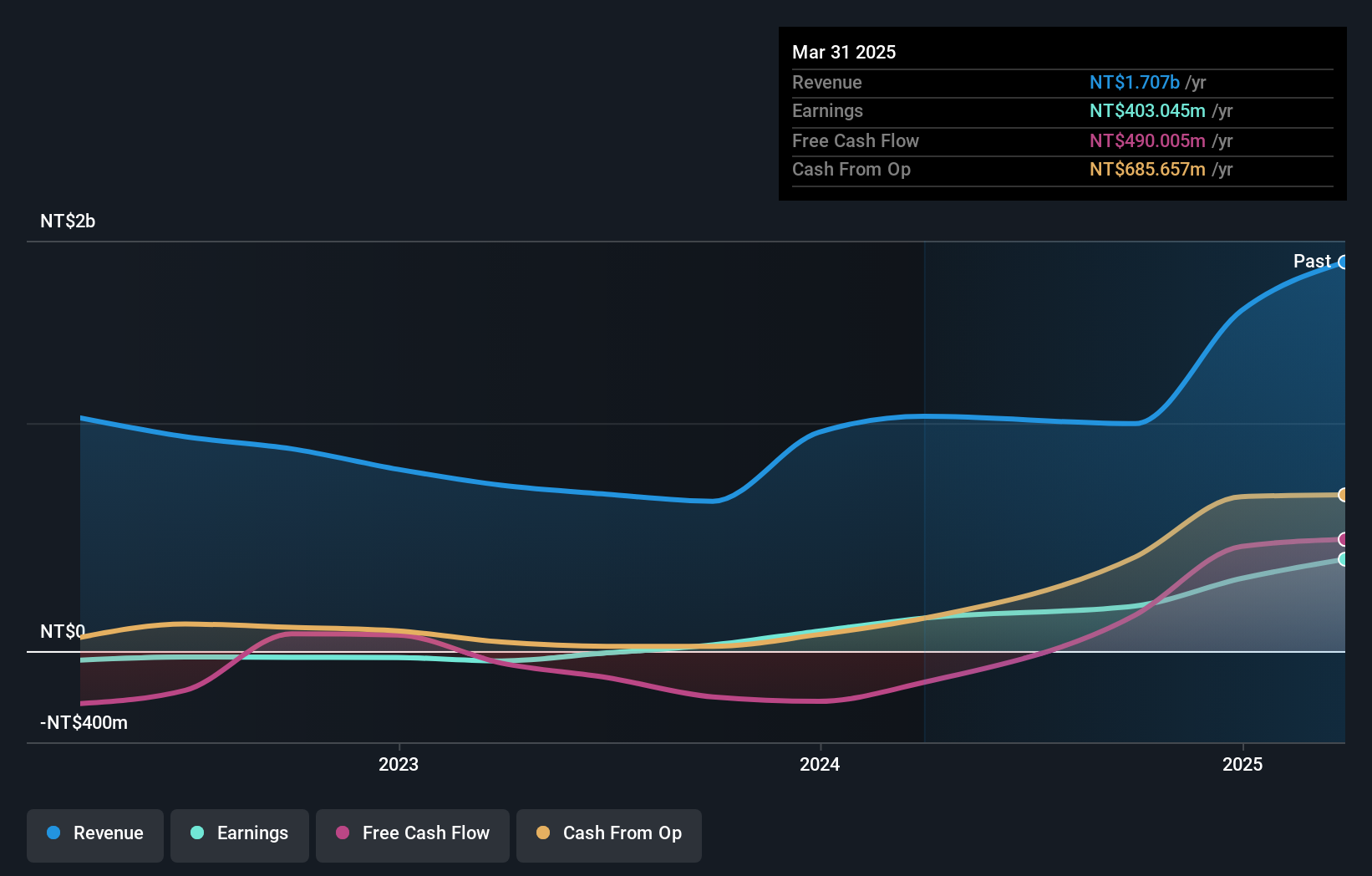

Wiselink (TPEX:8932)

Simply Wall St Value Rating: ★★★★★★

Overview: Wiselink Co., Ltd. manufactures and sells zippers globally under the MAX Zipper brand name, with a market capitalization of NT$21.56 billion.

Operations: The company's revenue primarily comes from the Taiwan Area, Mainland China Region, and Other Asia Pacific Regions, totaling NT$1.71 billion after accounting for intersegment transaction cancellations.

Wiselink, a notable player in the Asian market, has shown impressive growth with earnings surging 178% over the past year, outpacing its industry peers. Trading at 70.5% below estimated fair value, it presents a compelling valuation opportunity. The company reported first-quarter revenue of TWD 518.16 million and net income of TWD 144.99 million, reflecting strong financial health and high-quality earnings. Wiselink's debt-to-equity ratio improved from 46.6% to 9.7% over five years, indicating prudent financial management while planning to repurchase up to 1,500,000 shares for employee incentives by June 2025 enhances shareholder value further.

- Click here and access our complete health analysis report to understand the dynamics of Wiselink.

Assess Wiselink's past performance with our detailed historical performance reports.

Turning Ideas Into Actions

- Delve into our full catalog of 2614 Asian Undiscovered Gems With Strong Fundamentals here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Wiselink might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TPEX:8932

Wiselink

Manufactures and sells zippers under the MAX Zipper brand name worldwide.

Outstanding track record with flawless balance sheet.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|3.9% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$89.00|21.8% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|40.6% undervalued

TR

Community Contributor