Advertisement

Is Karelia Tobacco Company Inc’s (ATH:KARE) 18% ROCE Any Good?

Today we'll look at Karelia Tobacco Company Inc (ATH:KARE) and reflect on its potential as an investment. Specifically, we're going to calculate its Return On Capital Employed (ROCE), in the hopes of getting some insight into the business.

First, we'll go over how we calculate ROCE. Next, we'll compare it to others in its industry. Finally, we'll look at how its current liabilities affect its ROCE.

What is Return On Capital Employed (ROCE)?

ROCE measures the amount of pre-tax profits a company can generate from the capital employed in its business. All else being equal, a better business will have a higher ROCE. Overall, it is a valuable metric that has its flaws. Author Edwin Whiting says to be careful when comparing the ROCE of different businesses, since 'No two businesses are exactly alike.'

How Do You Calculate Return On Capital Employed?

The formula for calculating the return on capital employed is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

Or for Karelia Tobacco Company:

0.18 = €83m ÷ (€546m - €92m) (Based on the trailing twelve months to September 2018.)

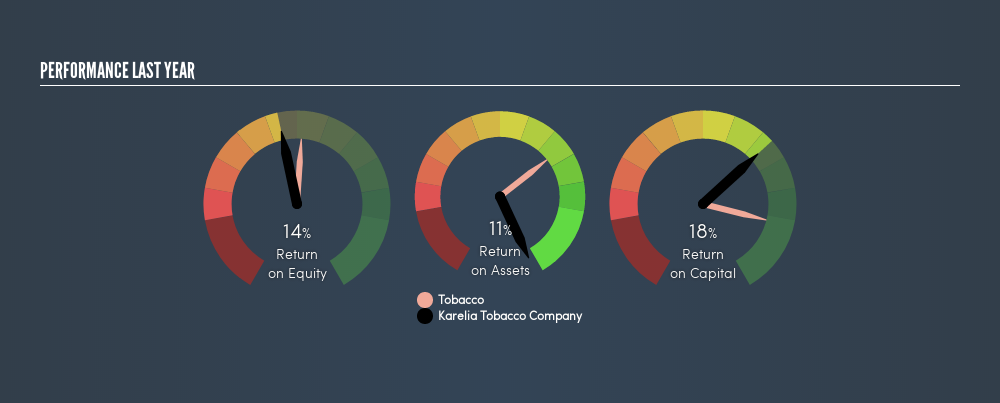

So, Karelia Tobacco Company has an ROCE of 18%.

View our latest analysis for Karelia Tobacco Company

Does Karelia Tobacco Company Have A Good ROCE?

ROCE can be useful when making comparisons, such as between similar companies. Karelia Tobacco Company's ROCE appears to be substantially greater than the 14% average in the Tobacco industry. We consider this a positive sign, because it suggests it uses capital more efficiently than similar companies. Regardless of where Karelia Tobacco Company sits next to its industry, its ROCE in absolute terms appears satisfactory, and this company could be worth a closer look.

As we can see, Karelia Tobacco Company currently has an ROCE of 18%, less than the 24% it reported 3 years ago. Therefore we wonder if the company is facing new headwinds.

Remember that this metric is backwards looking - it shows what has happened in the past, and does not accurately predict the future. Companies in cyclical industries can be difficult to understand using ROCE, as returns typically look high during boom times, and low during busts. ROCE is, after all, simply a snap shot of a single year. You can check if Karelia Tobacco Company has cyclical profits by looking at this freegraph of past earnings, revenue and cash flow.

Karelia Tobacco Company's Current Liabilities And Their Impact On Its ROCE

Current liabilities are short term bills and invoices that need to be paid in 12 months or less. Due to the way the ROCE equation works, having large bills due in the near term can make it look as though a company has less capital employed, and thus a higher ROCE than usual. To counteract this, we check if a company has high current liabilities, relative to its total assets.

Karelia Tobacco Company has total assets of €546m and current liabilities of €92m. As a result, its current liabilities are equal to approximately 17% of its total assets. Low current liabilities are not boosting the ROCE too much.

What We Can Learn From Karelia Tobacco Company's ROCE

With that in mind, Karelia Tobacco Company's ROCE appears pretty good. Of course you might be able to find a better stock than Karelia Tobacco Company. So you may wish to see this freecollection of other companies that have grown earnings strongly.

If you like to buy stocks alongside management, then you might just love this freelist of companies. (Hint: insiders have been buying them).

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About ATSE:KARE

Karelia Tobacco

Engages in the production and sale of tobacco products in European Union, Africa, Asia, Greece, and Other European countries.

Flawless balance sheet established dividend payer.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

138 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

930 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative