Advertisement

- United Kingdom

- /

- Metals and Mining

- /

- LSE:GLEN

Is Glencore Fairly Priced After Recent Merger Talks and Share Price Dip?

Simply Wall St

Reviewed by Bailey Pemberton

- Wondering if Glencore's current share price is truly a bargain or just hype? You're not alone. It's the perfect question to be asking right now.

- The stock has seen quite a journey, rising 101.0% over five years but down 4.2% over the last year. This shows that investor sentiment can shift quickly.

- Recently, Glencore’s share price has moved in response to ongoing debates about global commodity demand, as well as high-profile discussions around its merger activity and evolving sustainability commitments. These headlines have helped shape both near-term optimism and longer-term cautiousness in the market.

- Looking at valuation, Glencore scores a 4 out of 6 on our checks, indicating it’s undervalued in several key areas but not across the board. See the full breakdown here. Let's dive into the methods behind this score. Stick around, because we'll also show you a smarter way to assess value later in the article.

Find out why Glencore's -4.2% return over the last year is lagging behind its peers.

Approach 1: Glencore Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates a company’s intrinsic value by projecting its future cash flows and discounting them back to today’s value. This helps investors judge whether the current share price reflects the business’s genuine worth.

For Glencore, the latest reported Free Cash Flow is approximately $987 million. Analysts forecast steady growth in the coming years, with five-year projections reaching as high as $4.85 billion by the end of 2029. After that, Simply Wall St extends these forecasts out to 2035, with Free Cash Flow projections staying above $4 billion per year and gradually trending down.

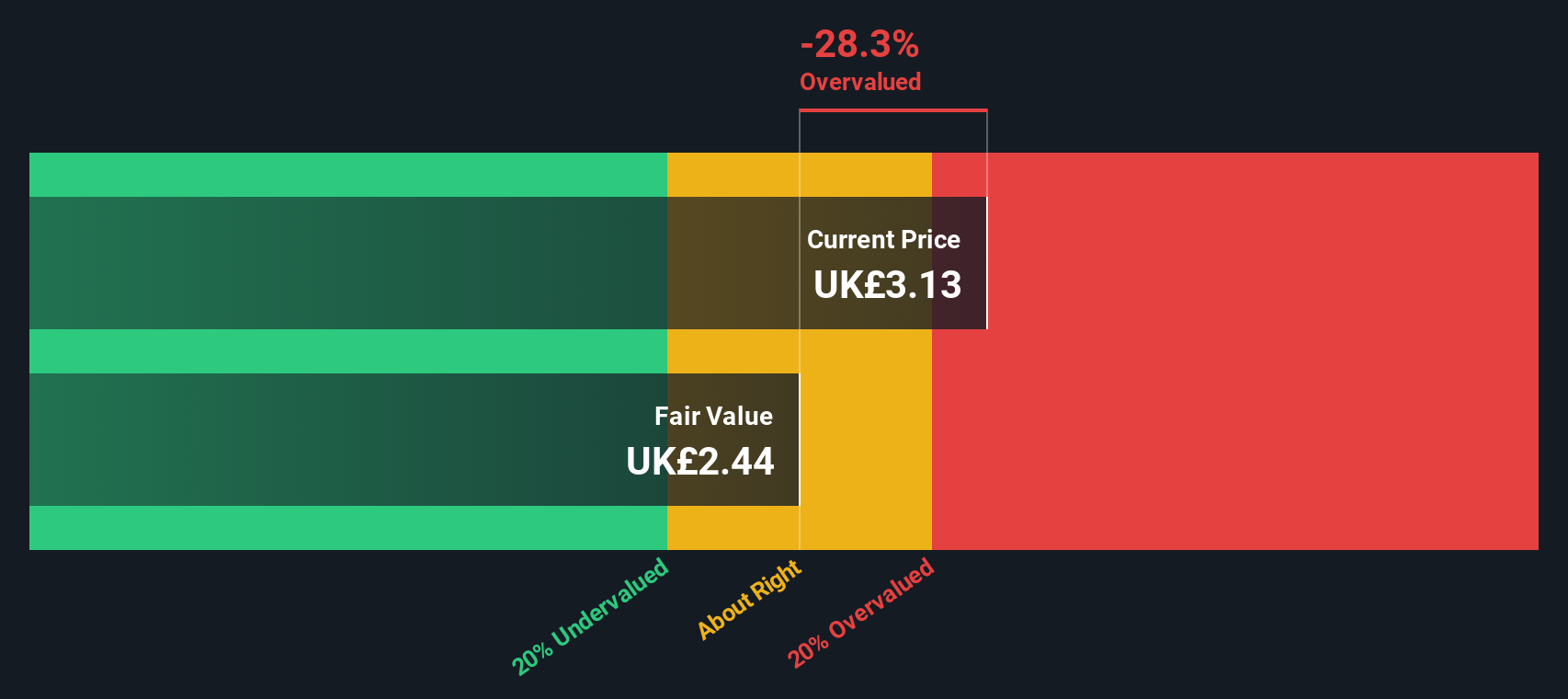

Based on these future cash flows, the resulting DCF estimate puts Glencore’s fair value at $3.67 per share. The current share price trades at a 4.5% discount to this value, suggesting the stock is essentially trading in line with its calculated worth.

Result: ABOUT RIGHT

Glencore is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

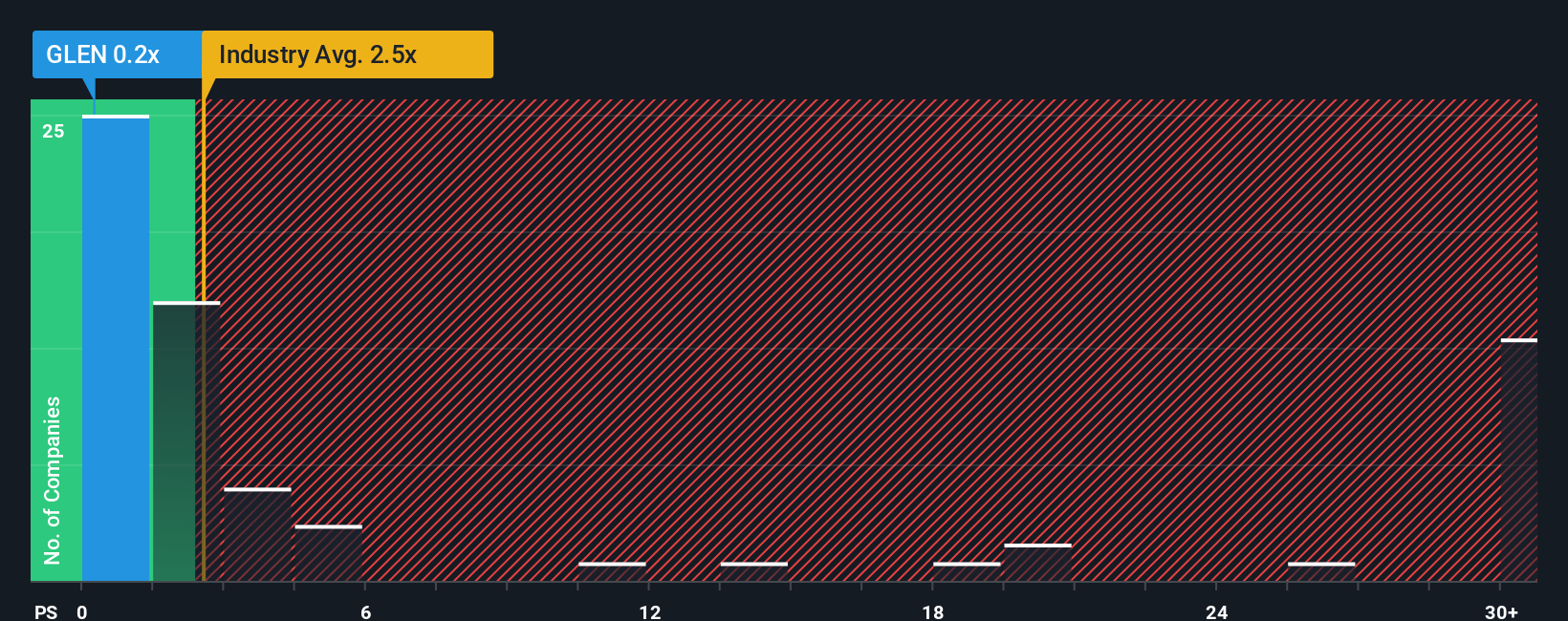

Approach 2: Glencore Price vs Sales

The Price-to-Sales (P/S) ratio is often used to value companies in sectors where profits can swing wildly from year to year, such as mining. It gives investors a clearer sense of what the market is willing to pay for each unit of a company’s revenue, making it especially useful for assessing companies with volatile or cyclical earnings. When comparing a company to others using P/S, it is important to consider factors like expected revenue growth and risk. Higher growth prospects or lower risks generally justify a higher “fair” multiple.

Glencore’s current P/S ratio is 0.24x, which is significantly lower than the industry average of 2.62x and the average of its direct peers at 3.73x. This may appear to be a discount at first glance, but it is necessary to go further to account for Glencore’s specific characteristics.

Simply Wall St’s proprietary Fair Ratio adds another perspective. Unlike simple peer or industry comparisons, the Fair Ratio weighs factors such as the company’s revenue growth outlook, profit margins, market cap, and sector-specific risks. For Glencore, the Fair Ratio stands at 0.86x, providing a more tailored benchmark than the broad industry average.

With Glencore currently trading at a P/S ratio of 0.24x, which is less than the Fair Ratio of 0.86x, the shares appear undervalued based on this approach.

Result: UNDERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1434 companies where insiders are betting big on explosive growth.

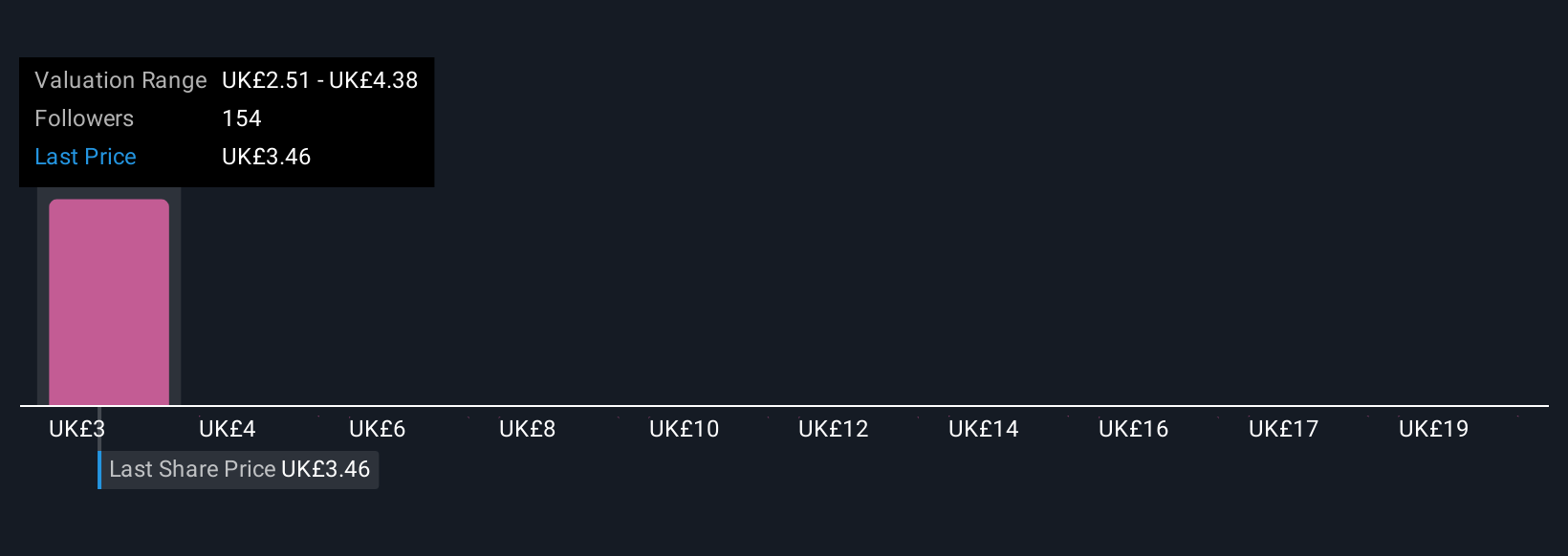

Upgrade Your Decision Making: Choose your Glencore Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives. A Narrative is a story investors create to explain what they believe will happen with a company, supported by their own forecasts for Glencore’s revenue, profit margins, and fair value. By linking your perspective on Glencore with your projections and seeing how these assumptions play out financially, Narratives help clarify both the company’s story and its numbers.

On Simply Wall St’s Community page, Narratives are an accessible tool used by millions of investors. They help you evaluate your investment options by comparing your own estimate of fair value—driven by your Narrative—to the current share price. Narratives also update automatically as new financial results or major news is released, ensuring your view stays relevant.

For Glencore, for example, the highest shared Narrative currently expects a future price target of £4.61 per share based on strong copper growth and efficient operations, while the lowest sees just £3.09, citing regulatory risks and uncertain project outcomes. This range of perspectives helps demonstrate how different stories and assumptions about Glencore’s future can yield different, but data-driven, conclusions.

Do you think there's more to the story for Glencore? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:GLEN

Glencore

Engages in the production, refinement, processing, storage, transport, and marketing of metals and minerals, and energy products in the Americas, Europe, Asia, Africa, and Oceania.

Good value with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

75 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8147.4% undervalued

9 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

89 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

926 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative