- United Kingdom

- /

- Professional Services

- /

- AIM:ELIX

Undiscovered Gems In The United Kingdom For August 2024

Reviewed by Simply Wall St

The United Kingdom's stock market has recently been influenced by weak trade data from China, causing the FTSE 100 to close lower amid global economic uncertainties. Despite these broader market challenges, there are still promising opportunities within the small-cap sector that can offer potential growth and resilience. Identifying stocks with strong fundamentals and a clear growth strategy is crucial in navigating these turbulent times.

Top 10 Undiscovered Gems With Strong Fundamentals In The United Kingdom

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Andrews Sykes Group | NA | 1.69% | 3.16% | ★★★★★★ |

| Globaltrans Investment | 15.40% | 2.68% | 16.51% | ★★★★★★ |

| Impellam Group | 31.12% | -5.43% | -6.86% | ★★★★★★ |

| London Security | 0.31% | 9.47% | 7.41% | ★★★★★★ |

| M&G Credit Income Investment Trust | NA | -0.35% | 1.18% | ★★★★★★ |

| Rights and Issues Investment Trust | NA | -3.68% | -4.07% | ★★★★★★ |

| FW Thorpe | 3.34% | 11.37% | 9.41% | ★★★★★☆ |

| Goodwin | 59.96% | 9.26% | 13.12% | ★★★★★☆ |

| BBGI Global Infrastructure | 0.02% | 6.58% | 9.90% | ★★★★★☆ |

| Mountview Estates | 16.64% | 4.50% | -0.59% | ★★★★☆☆ |

Here's a peek at a few of the choices from the screener.

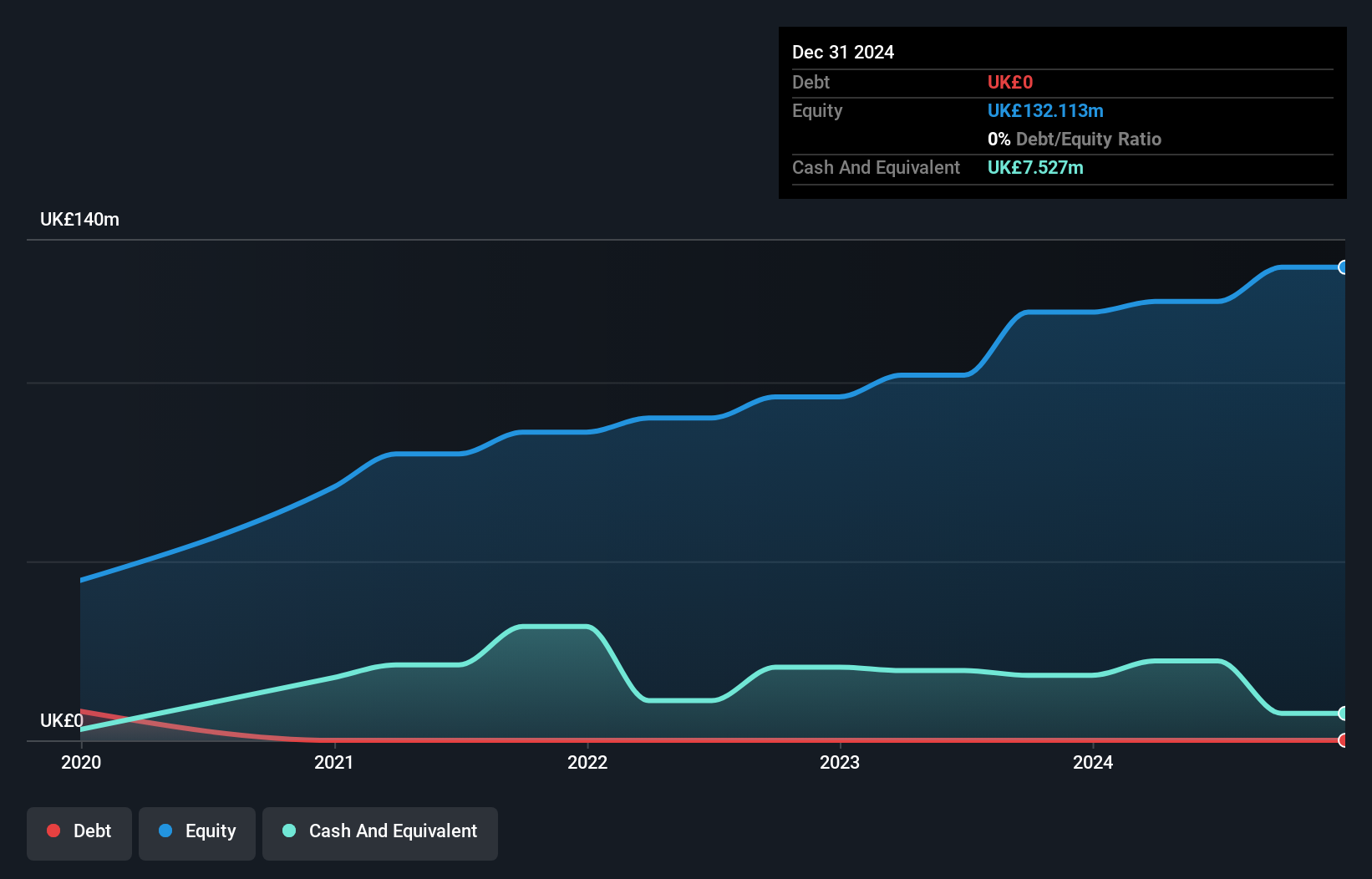

Elixirr International (AIM:ELIX)

Simply Wall St Value Rating: ★★★★★★

Overview: Elixirr International plc, with a market cap of £288.55 million, offers management consultancy services through its subsidiaries in the United Kingdom, the United States, and internationally.

Operations: Elixirr International generates £85.89 million in revenue from management consulting services.

Elixirr International, a notable player in the Professional Services industry, has shown impressive growth with earnings up 33.9% over the past year, outpacing the industry’s -3.9%. Trading at 59.7% below its estimated fair value and being debt-free adds to its appeal. Recent collaboration with Peak Performance Project (P3) significantly enhanced P3's data management system, reducing processing times from 4-6 hours to under 30 minutes and positioning both companies for continued growth and innovation.

Alpha Group International (LSE:ALPH)

Simply Wall St Value Rating: ★★★★★★

Overview: Alpha Group International plc offers foreign exchange risk management and alternative banking solutions across the United Kingdom, Europe, Canada, and internationally, with a market cap of £1.10 billion.

Operations: Alpha Group International plc generates revenue primarily from its segments: Alpha Pay (£64.30 million), Institutional (£61.29 million), and Corporate London excluding Amsterdam (£45.42 million). Other notable contributions come from Corporate Amsterdam (£8.70 million) and Corporate Toronto (£4.23 million).

Trading at a price-to-earnings ratio of 12.4x, Alpha Group International offers good value compared to the UK market average of 17x. The firm has no debt and boasts high-quality past earnings with significant non-cash components. Over the past year, earnings surged by 130%, outpacing the Capital Markets industry growth rate of 0.4%. Recent events include its addition to multiple FTSE indices and a share repurchase program authorized to buy back up to 10% of its issued shares.

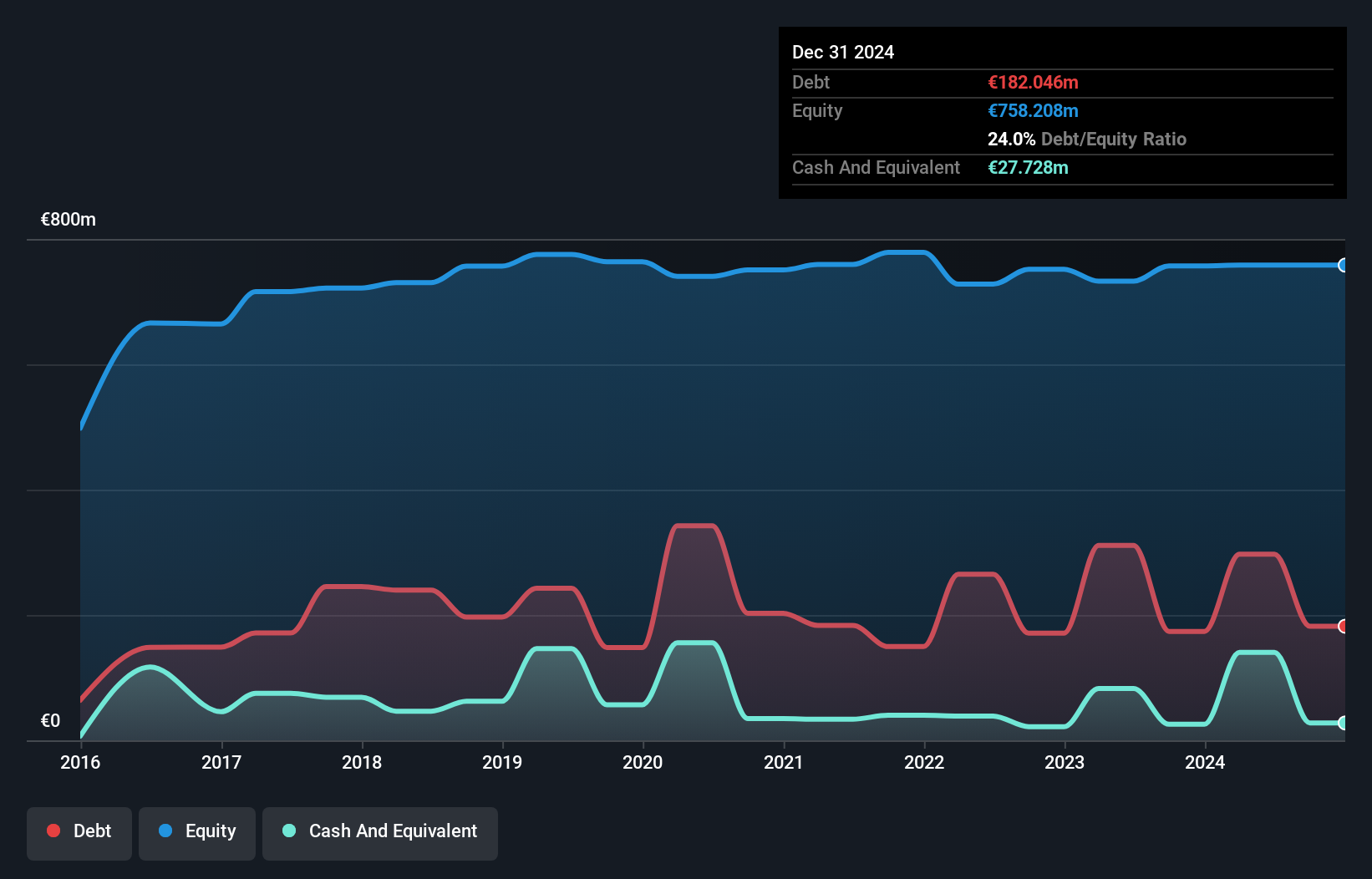

Cairn Homes (LSE:CRN)

Simply Wall St Value Rating: ★★★★★★

Overview: Cairn Homes plc, a holding company with a market cap of £1.02 billion, operates as a home and community builder in Ireland.

Operations: Cairn Homes generates revenue primarily from building and property development, amounting to €666.81 million. The company's net profit margin is 10.5%.

Cairn Homes, a notable player in the UK market, has shown promising financial health. The company's net debt to equity ratio stands at 19.6%, which is satisfactory by industry standards. Over the past year, earnings grew by 5.4%, outpacing the Consumer Durables sector's -14%. Cairn's EBIT covers its interest payments 8.4 times over, indicating strong debt management. Additionally, with a price-to-earnings ratio of 14x compared to the UK market's 17x, it offers good value for investors.

- Click here to discover the nuances of Cairn Homes with our detailed analytical health report.

Explore historical data to track Cairn Homes' performance over time in our Past section.

Next Steps

- Investigate our full lineup of 77 UK Undiscovered Gems With Strong Fundamentals right here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Elixirr International might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About AIM:ELIX

Elixirr International

Through its subsidiaries, provides management consultancy services in the United Kingdom, the United States, and internationally.

Very undervalued with flawless balance sheet.