Advertisement

- France

- /

- Personal Products

- /

- ENXTPA:ITP

Assessing Interparfums After Recent Share Slide and Valuation Model Insights

Simply Wall St

Reviewed by Simply Wall St

If you are scratching your head over what to do with Interparfums right now, you are certainly not alone. It is a name that has managed to stir up conversation among investors, both for its resilience and its rollercoaster stock performance. Over the past year, shares have slid by 18.0 % and are down 19.9 % since the start of the year. That may raise eyebrows, especially when you factor in a five-year return of nearly 30 %. So, what is driving these moves?

Some of the recent turbulence seems tied to broader market trends hitting consumer brands, as well as shifting investor sentiment about luxury and fragrance stocks in general. Short-term returns are in the red, with a dip of 2.8 % in just the last week and an 8.1 % loss over the last month. That might tempt value-seekers. After all, Interparfums scores a 4 out of 6 on our value assessment checklist, meaning it is considered undervalued in the majority of key areas we analyse.

This is where things get interesting. Valuation can tell us a lot, but which method really reveals the truth behind a stock like Interparfums? Let’s dive into the main approaches for assessing value, and be sure to stick around as we close out with a powerful perspective on valuation that savvy investors should not miss.

Why Interparfums is lagging behind its peersApproach 1: Interparfums Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) valuation model estimates a company’s intrinsic value by projecting its future free cash flows and discounting them back to their present value. For Interparfums, this method provides a window into both its current financial health and long-term growth prospects.

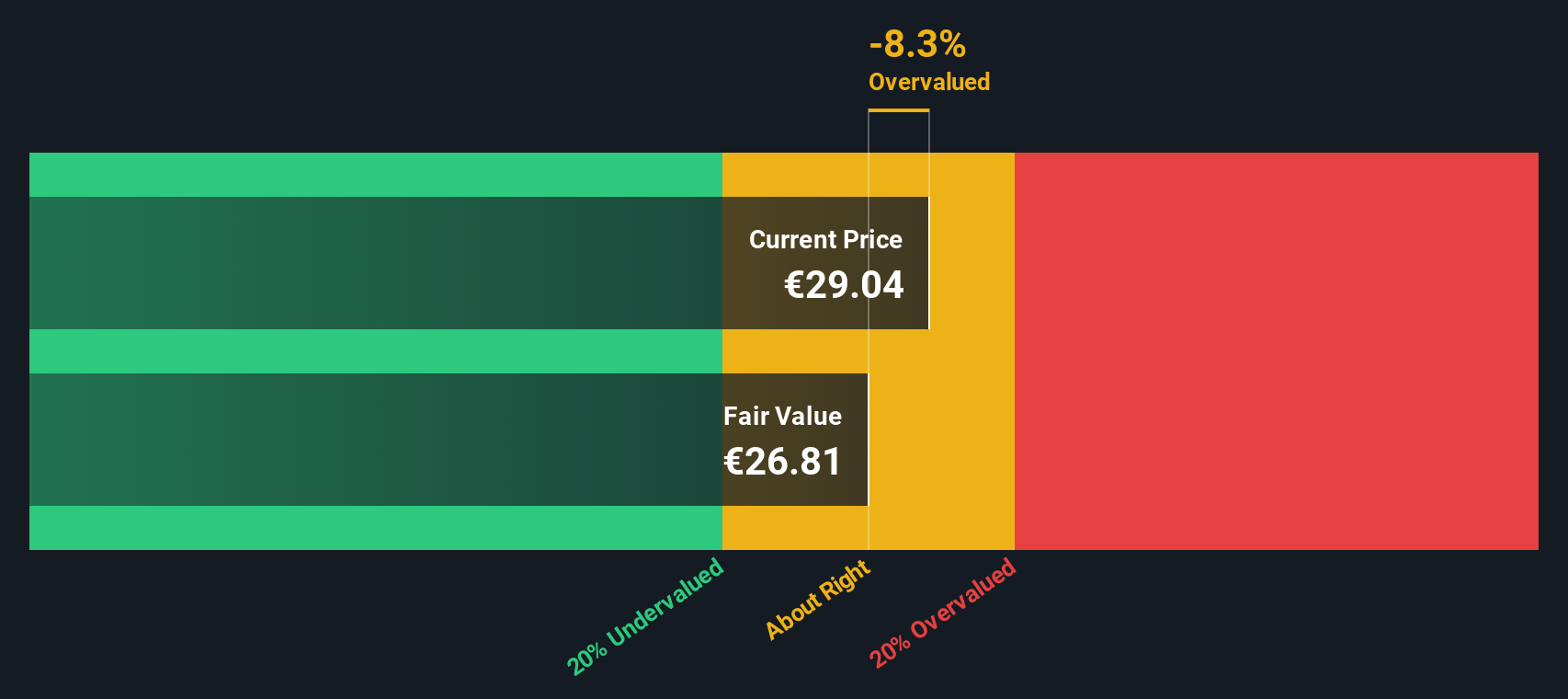

Currently, Interparfums generates free cash flow of €72.1 million. Analysts provide forecast figures for the next five years, and Simply Wall St extrapolates projections up to 2035. For example, free cash flow is expected to reach €127 million by 2028, with continued incremental growth into the next decade. All cash flows are evaluated in euros.

By aggregating these cash flow estimates and discounting them to account for the time value of money, the DCF model arrives at an intrinsic value of €26.92 per share. Compared to the current share price, this suggests the stock is about 9.1% more expensive than its fundamentals warrant. This points toward a modest overvaluation.

Result: ABOUT RIGHT

Head to the Valuation section of our Company Report for more details on how we arrive at this Fair Value for Interparfums.

Approach 2: Interparfums Price vs Earnings

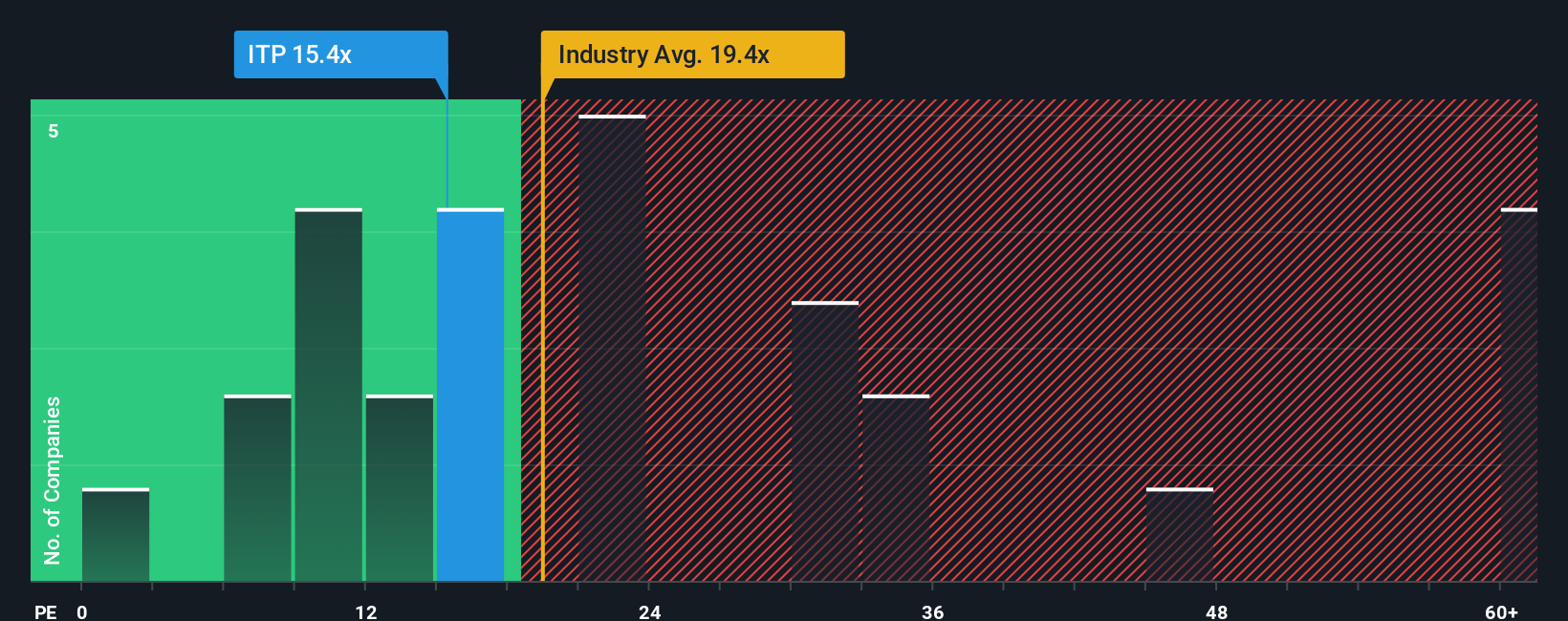

For companies that are reliably profitable, like Interparfums, the Price-to-Earnings (PE) ratio is a widely used and relevant metric. It captures how much investors are willing to pay for each euro of the company’s earnings. This makes it especially useful when analysing businesses with stable profit streams.

A company’s appropriate or “normal” PE ratio depends heavily on expected earnings growth and the perceived riskiness of those earnings. Higher growth prospects and lower risks tend to support higher PE multiples. More volatile or uncertain earnings usually demand a discount.

Currently, Interparfums trades at a PE ratio of 18.4x. For context, the average PE ratio across the Personal Products industry stands at 23.3x, while direct peers are trading at a higher average of 58.4x. Simply Wall St’s proprietary Fair Ratio for Interparfums, which considers factors like its earnings growth outlook, profit margins, industry classification, company size, and risk profile, comes in at 22.1x.

The Fair Ratio offers a more nuanced view compared to simply comparing Interparfums to its industry or peer group. It goes beyond raw averages by directly accounting for the company’s specific fundamentals and circumstances. This means it should be a more reliable benchmark for judging whether shares are priced reasonably.

With Interparfums’ current PE of 18.4x and a Fair Ratio of 22.1x, the company’s valuation is closely aligned with what you would expect based on its profile. The difference is not significant, suggesting it is priced fairly at current levels.

Result: ABOUT RIGHT

Upgrade Your Decision Making: Choose your Interparfums Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives. A Narrative is a simple, yet powerful way to tie your personal view or story about a company directly to the numbers. It shows what you believe is a fair value and how you expect revenue, earnings, or margins might change in the future.

Narratives connect the dots by linking your perspective about Interparfums (or any company) to a clear financial forecast and resulting fair value estimate. This turns valuation into something dynamic and personal, not just a number on a page. The great news is that Narratives are easily accessible on Simply Wall St, right on the Community page where millions of investors share their own perspectives and insights.

With Narratives, you decide when to buy or sell by directly comparing your fair value estimate to the current price, and your view is automatically updated whenever new news or earnings reports are released. For example, some investors may see Interparfums as currently undervalued with high growth ahead, while others might believe its recent challenges mean a lower fair value for now.

Do you think there's more to the story for Interparfums? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ENXTPA:ITP

Interparfums

Designs, manufactures, and distributes perfumes and cosmetics through license agreements with ready-to-wear, jewelry, or accessories houses in France, Africa, North America, South America, Eastern Europe, Western Europe, Asia, and the Middle East.

Undervalued with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

75 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8147.4% undervalued

9 followersusers have followed this narrative

2 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

89 followersusers have followed this narrative

11 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

926 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative