Advertisement

- Spain

- /

- Food and Staples Retail

- /

- BME:DIA

How Should Investors View Distribuidora Internacional de Alimentación After Its 95% Rally in 2024?

Simply Wall St

Reviewed by Simply Wall St

If you are eyeing Distribuidora Internacional de Alimentación and wondering whether now is the right moment to make a move, you are not alone. Over the past year, this stock has certainly given investors a wild ride. From turning heads with a whopping 95.7% gain over twelve months, to posting a near-tripling year-to-date bounce of 63.7%, Distribuidora Internacional de Alimentación has landed back on many watchlists after years in the shadows. Yet, for all this momentum, the last week saw shares dip by 2.9%, while the past month has been almost flat at -0.4%. This tug-of-war in performance says plenty about shifting market sentiment and a recalibration of risk, especially after such a dramatic longer-term rebound from tough years, considering the five-year loss still sits at -48.7%.

What is driving this action? Some of the recent moves have coincided with broader market rotations, as investors respond to renewed interest in consumer staples and potential corporate developments that have not quite flown under the radar. While not every shift comes on the back of blockbuster headlines, the context of macro stability and evolving competition keeps Distribuidora Internacional de Alimentación’s share price in focus.

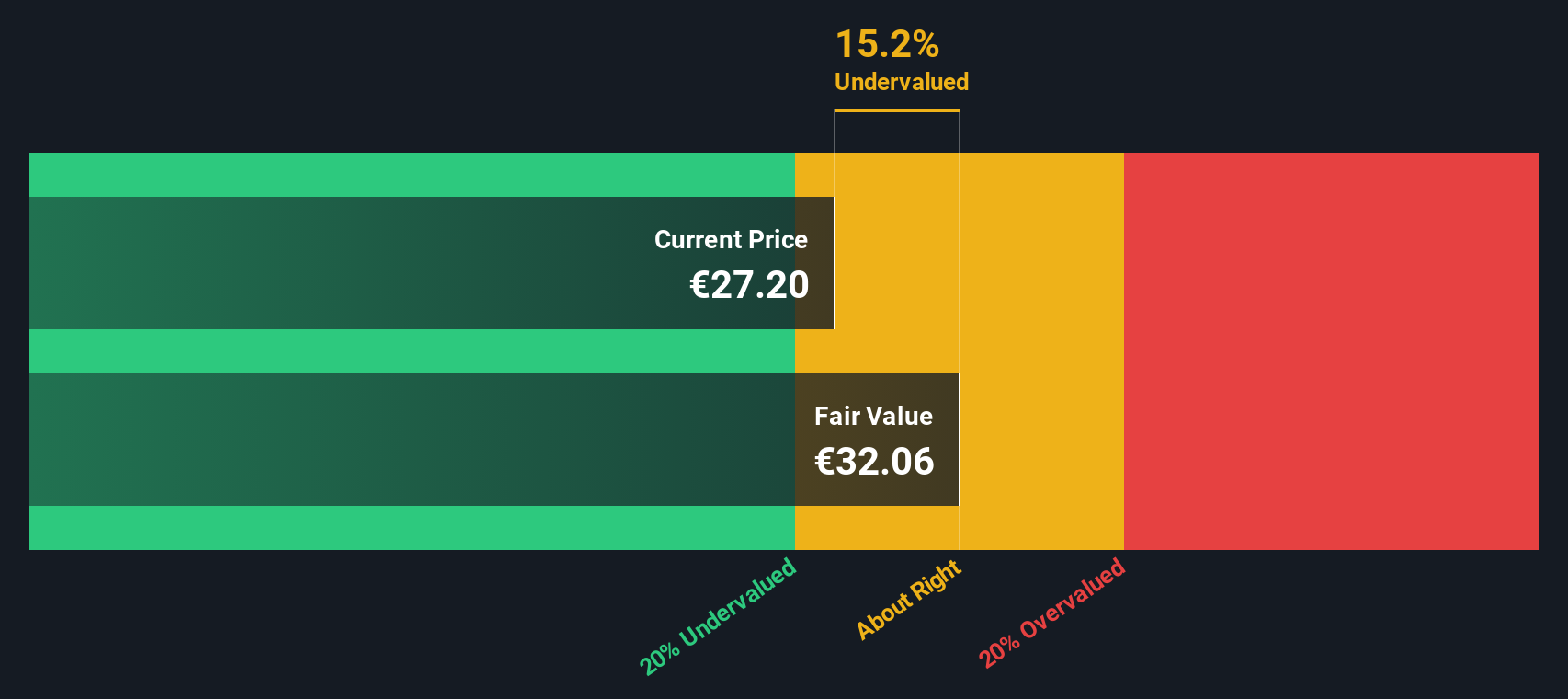

But before jumping in, it's crucial to ask: how does this company stack up by the numbers? According to our valuation scorecard, Distribuidora Internacional de Alimentación is undervalued in 0 out of 6 key checks, so at first glance, it may not scream “bargain.” Don’t worry, though. We are about to dig into what those valuation measures really mean, and why there could be a smarter way to judge if this stock truly deserves a place in your portfolio.

Distribuidora Internacional de Alimentación scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.Approach 1: Distribuidora Internacional de Alimentación Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model aims to estimate a company’s intrinsic value by projecting its expected future cash flows and then discounting them back to today’s value, reflecting both growth expectations and risk. For Distribuidora Internacional de Alimentación, the DCF uses a 2 Stage Free Cash Flow to Equity approach. In simple terms, it looks at how much free cash the business is expected to generate over time, starting with recent results and layering in forecasts and longer-term estimates.

The latest twelve months saw Distribuidora Internacional de Alimentación turn out free cash flow of €356.36 million. Analyst estimates stretch out five years, with Simply Wall St extrapolating beyond that horizon. By 2029, projections see annual free cash flow falling sharply to €53 million, with subsequent years tracing a declining path driven by modeled assumptions.

After discounting all these future cash flows to their present value, the model calculates an estimated intrinsic value per share of €16.28. Comparing this figure to the current share price, the outcome is a 53.9% premium, signaling the stock is significantly overvalued based on today’s expectations for future cash generation.

Result: OVERVALUED

Head to the Valuation section of our Company Report for more details on how we arrive at this Fair Value for Distribuidora Internacional de Alimentación.

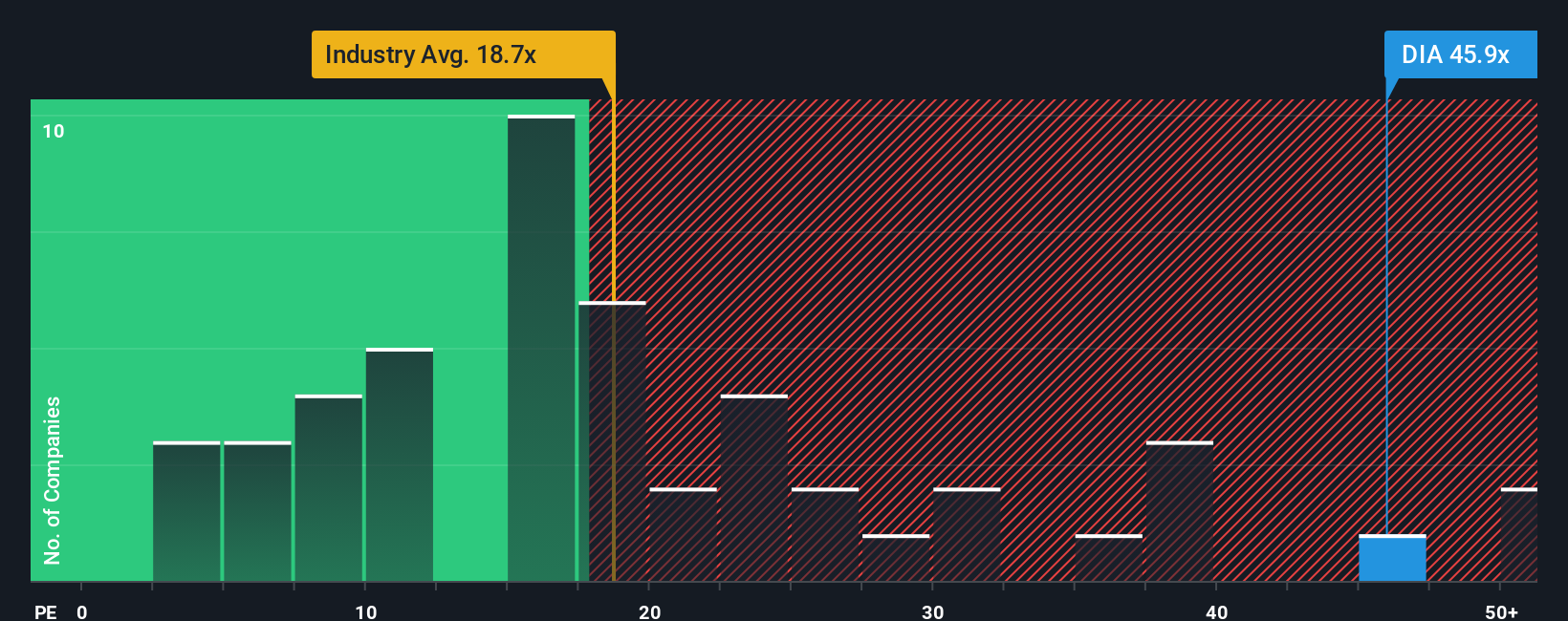

Approach 2: Distribuidora Internacional de Alimentación Price vs Earnings

The price-to-earnings (PE) ratio is a widely used valuation measure for profitable companies because it connects a company’s share price to its underlying earnings. It helps investors assess at a glance how much the market is willing to pay for each euro of earnings, making it especially useful for firms with positive net income like Distribuidora Internacional de Alimentación.

Choosing an appropriate “fair” PE ratio involves more than just looking at what peers or the industry are trading at. Factors such as whether a company is growing faster than its rivals, the stability of future profits, or whether there are unique risks, all play a part. Distribuidora Internacional de Alimentación’s PE ratio currently stands at 38.1x, well above both the Consumer Retailing industry average of 17.2x and its peer group average of 22.1x. At first glance, this suggests the market expects stronger future earnings or sees less risk compared to competitors.

This is where Simply Wall St’s proprietary Fair Ratio comes in. The Fair Ratio goes a step further than a simple comparison to peers, as it analyzes the company’s specific growth outlook, profitability, risks, and size. This provides a more nuanced view of what a reasonable valuation multiple should be, tailored to Distribuidora Internacional de Alimentación’s position and prospects instead of just broad industry trends.

Based on the Fair Ratio, Distribuidora Internacional de Alimentación’s actual PE multiple appears too high for what the fundamentals support. This points to the shares trading above their justified valuation level using this metric.

Result: OVERVALUED

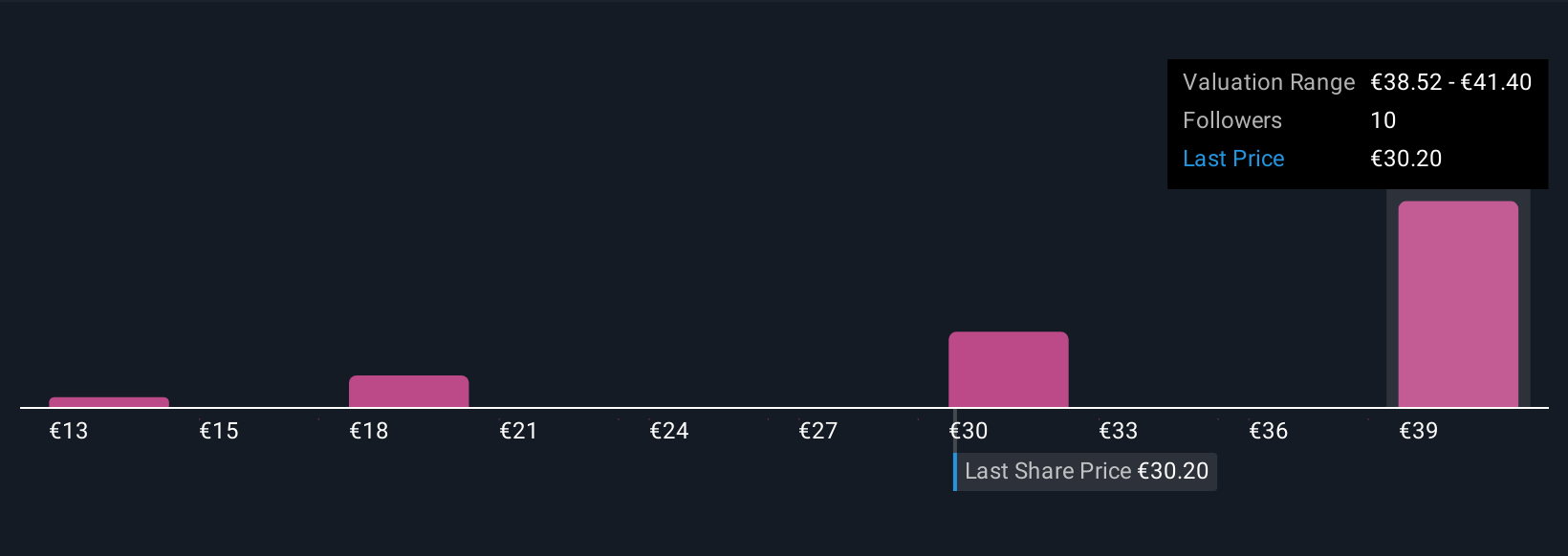

Upgrade Your Decision Making: Choose your Distribuidora Internacional de Alimentación Narrative

Earlier, we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative lets you connect your personal story or perspective about a company to the numbers, by outlining your view of its business model, prospects, and performance, and then linking that to your own fair value estimate based on future revenue, earnings, and margin forecasts. This means you are not just passively accepting a pre-made valuation, but actively shaping it with your insight and thesis, making the process both easy and accessible. Narratives are fully integrated into Simply Wall St's Community page alongside millions of other investor perspectives.

With Narratives, you can see how your expectations translate into a fair value, then easily compare this to the current share price to help you decide whether to buy or sell. Best of all, Narratives update dynamically as new news or financial results come in, so your thesis always stays relevant. For Distribuidora Internacional de Alimentación, for example, one Narrative may forecast robust growth and a higher fair value, while another might expect stagnation and a much lower fair value, reflecting the real-world difference in investor approaches.

Do you think there's more to the story for Distribuidora Internacional de Alimentación? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About BME:DIA

Distribuidora Internacional de Alimentación

Distribuidora Internacional de Alimentación, S.A.

High growth potential with moderate risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative