Advertisement

- Spain

- /

- Construction

- /

- BME:OHLA

OHLA (BME:OHLA) Q3 Net Loss of €17.2M Persists Despite Margin Gains, Testing Turnaround Narrative

Simply Wall St

Reviewed by Simply Wall St

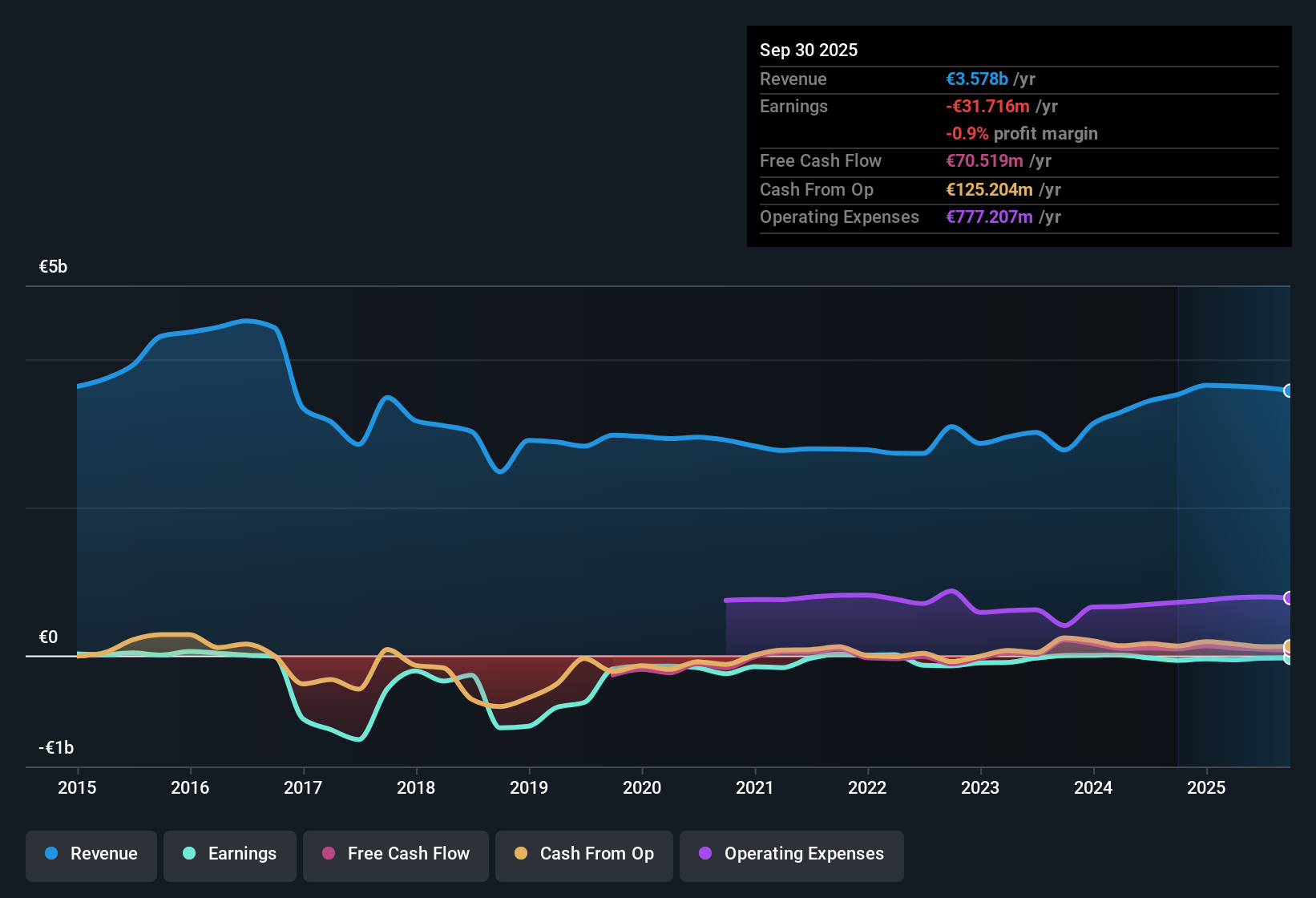

Obrascón Huarte Lain (BME:OHLA) just released its Q3 2025 numbers with revenue of €959.8 million and net income from continuing operations of -€17.2 million. Over recent periods, the company has seen revenue move from €783.1 million in Q1 to €959.8 million in Q3, while net income slipped from -€16.7 million to -€17.2 million. Margins remain under pressure as OHLA works to return to profitability.

See our full analysis for Obrascón Huarte Lain.Now that the headline numbers are out, the next step is to see how the latest results stack up against market narratives and investor expectations.

See what the community is saying about Obrascón Huarte Lain

Margins Move Up as Cost Reductions Take Hold

- Construction division EBITDA margin reached 6.8%, up from 4% the previous year. This reflects benefits from a €40 million cost-cutting plan and a stronger focus on higher-margin infrastructure contracts.

- Consensus narrative notes that narrowing losses, with annual losses shrinking by 30.4% per year over five years, suggests operational improvements are working. However, net income from continuing operations remains negative at -€17.2 million, which highlights the challenge of sustained profitability.

- Consensus sees ongoing revenue growth and margin gains as essential to achieving positive earnings by 2028.

- Stabilizing costs and higher margins support the analysts' view that OHLA could return to profitability within three years despite recent setbacks.

- To see if these margin gains can fuel a long-term turnaround, read the full consensus narrative. 📊 Read the full Obrascón Huarte Lain Consensus Narrative.

Discounted Valuation Versus Peers and Fair Value

- Shares trade at a Price-to-Sales Ratio of 0.1x, which is well below both the 0.8x peer average and 0.5x European construction industry average. The current share price of €0.39 is significantly below the DCF fair value of €0.58.

- Consensus narrative points to this valuation gap as a potential opportunity for investors. It argues that if OHLA achieves the projected revenue growth of 4.9% per year and earnings growth of 78.3% per year, the stock’s discounted price could offer upside, though risks like past shareholder dilution and price volatility remain important considerations.

- Share price volatility, along with higher dilution over the past year, continue to temper sentiment, even with the discounted valuation.

- With analyst price targets set at €0.53, the upside depends on the company meeting aggressive profit and revenue assumptions contained in the consensus view.

Revenue Quality and Portfolio Reshaping

- A strong contract backlog of €8.6 billion and a 1.3 book-to-bill ratio reinforce visibility on future revenue. The disposal of the Services division and other non-core assets aims to sharpen the infrastructure focus.

- Consensus narrative stresses that while these moves aim to improve earnings stability and focus, revenue concentration risk remains high with 94% of sales from construction. Delays in the sale or turnaround of underperforming assets could limit future profit growth.

- An improving backlog signals potential for steady top-line growth, but high reliance on construction heightens sensitivity to market swings in core regions.

- Analysts warn that lingering legal disputes and slow asset sales could offset gains from current strategic moves.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Obrascón Huarte Lain on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Not convinced by the consensus? You can quickly turn your unique interpretation of OHLA’s results into a personalized narrative that reflects your perspective. Do it your way

A great starting point for your Obrascón Huarte Lain research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

See What Else Is Out There

OHLA’s persistent losses, ongoing reliance on construction, and exposure to volatile margins raise concerns about the company’s ability to deliver consistent and stable earnings growth.

If you want investment ideas with steadier results, check out stable growth stocks screener (2074 results) to find companies proving they can deliver reliable revenue and earnings expansion regardless of market swings.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About BME:OHLA

Obrascón Huarte Lain

Engages in the construction and concession businesses in the United States, Canada, Mexico, Chile, Peru, Colombia, Spain, Central and Eastern Europe, Northern Europe, and internationally.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SW

swift11 on DXC Technology ·

CEO: We are winners in the long term in the AI world

Fair Value:US$17.4624.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

102 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative