Advertisement

Zealand Pharma (CPSE:ZEAL) Is Up 22.7% After Earnings Swing From Loss to Net Income – Has The Bull Case Changed?

Simply Wall St

Reviewed by Sasha Jovanovic

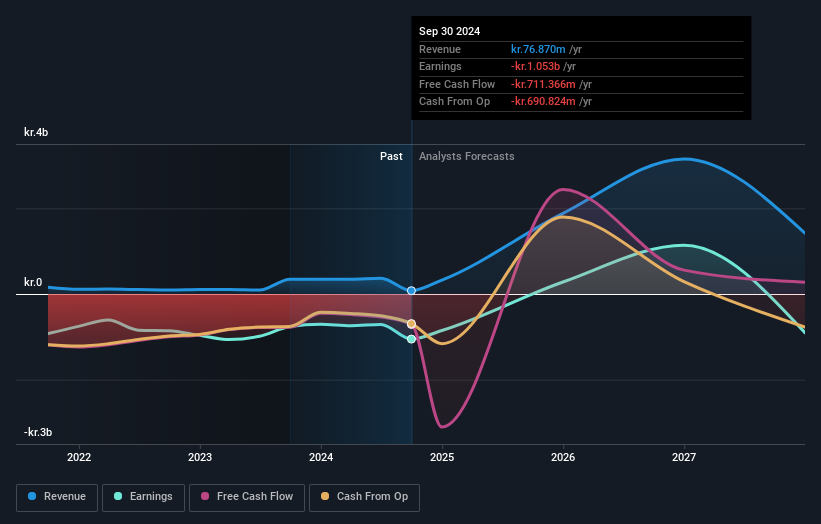

- Zealand Pharma reported its third quarter 2025 results, announcing sales of DKK49.57 million and a quarterly net loss of DKK404.23 million, while nine-month sales reached DKK9.15 billion with net income of DKK6.83 billion.

- This rapidly shifting financial picture shows a swing from net loss to substantial net income over the nine-month period, underlining the impact of recent commercial developments.

- We'll now consider how Zealand's dramatic year-to-date earnings turnaround may influence the company's investment narrative and risk outlook.

AI is about to change healthcare. These 31 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Zealand Pharma Investment Narrative Recap

To own Zealand Pharma stock, investors must believe in the company’s pipeline-driven turnaround and the ability to convert milestone-driven revenue into sustainable growth, especially as its lead products progress through development stages. The latest quarterly update does not materially change the short-term focus: clinical trial outcomes for petrelintide and dapiglutide remain the critical catalyst, while dependency on partnership payments and potential regulatory setbacks continue to be the largest risks for the business at this stage.

Among the recent announcements, the effective collaboration and licensing agreement with Roche stands out. This alliance, now operational, could help Zealand counterbalance the unpredictability of milestone revenues by expanding access to commercial expertise and resources as key clinical assets move forward. The direct impact on growth will be shaped by the success of Zealand’s ongoing late-stage studies.

Yet, despite these positive steps, the risk of intensified competition and margin pressure from larger players remains an important factor that investors should be aware of if...

Read the full narrative on Zealand Pharma (it's free!)

Zealand Pharma's narrative projects DKK2.3 billion revenue and DKK696.4 million earnings by 2028. This requires a 36.7% yearly revenue decline and a DKK6.0 billion decrease in earnings from DKK6.7 billion today.

Uncover how Zealand Pharma's forecasts yield a DKK818.80 fair value, a 57% upside to its current price.

Exploring Other Perspectives

The Simply Wall St Community reached four fair value estimates for Zealand Pharma ranging from DKK4 to DKK840 per share. As clinical data and milestone revenue shape the outlook, you can explore why market opinions vary so widely.

Explore 4 other fair value estimates on Zealand Pharma - why the stock might be worth less than half the current price!

Build Your Own Zealand Pharma Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Zealand Pharma research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Zealand Pharma research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Zealand Pharma's overall financial health at a glance.

No Opportunity In Zealand Pharma?

Our top stock finds are flying under the radar-for now. Get in early:

- Find companies with promising cash flow potential yet trading below their fair value.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 37 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Zealand Pharma might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About CPSE:ZEAL

Zealand Pharma

A biotechnology company, engages in the discovery, development, and commercialization of peptide-based medicines in Denmark and the United States.

Excellent balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.4% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.0% undervalued

EA

Community Contributor