Discover 3 High Growth Chinese Stocks With Strong Insider Ownership

Reviewed by Simply Wall St

As Chinese equities show resilience despite weaker-than-expected economic activity, investors are increasingly eyeing growth stocks with strong insider ownership as potential opportunities. In this article, we will explore three high-growth Chinese companies where significant insider ownership could signal confidence in their long-term prospects.

Top 10 Growth Companies With High Insider Ownership In China

| Name | Insider Ownership | Earnings Growth |

| Ningbo Sunrise Elc TechnologyLtd (SZSE:002937) | 24.3% | 27.7% |

| ShenZhen Woer Heat-Shrinkable MaterialLtd (SZSE:002130) | 19% | 27.9% |

| Arctech Solar Holding (SHSE:688408) | 38.7% | 26.9% |

| Cubic Sensor and InstrumentLtd (SHSE:688665) | 10.1% | 34.3% |

| KEBODA TECHNOLOGY (SHSE:603786) | 12.8% | 25.1% |

| Xi'an Sinofuse Electric (SZSE:301031) | 36.8% | 43.1% |

| Suzhou Sunmun Technology (SZSE:300522) | 36.5% | 63.4% |

| Sineng ElectricLtd (SZSE:300827) | 36.5% | 40.1% |

| Jilin University Zhengyuan Information Technologies (SZSE:003029) | 12.6% | 82.2% |

| UTour Group (SZSE:002707) | 23% | 36.1% |

Let's explore several standout options from the results in the screener.

MayAir Technology (China) (SHSE:688376)

Simply Wall St Growth Rating: ★★★★★☆

Overview: MayAir Technology (China) Co., Ltd. focuses on the R&D, production, and sale of medical air purification equipment and atmospheric environment treatment products in China, with a market cap of CN¥3.44 billion.

Operations: The company's revenue segments include CN¥1.25 billion from medical air purification equipment and CN¥2.50 billion from atmospheric environment treatment products.

Insider Ownership: 14.6%

Revenue Growth Forecast: 20.9% p.a.

MayAir Technology (China) reported half-year sales of CNY 756.98 million, up from CNY 651.64 million last year, with net income rising to CNY 92.88 million from CNY 76.99 million. Earnings per share increased to CNY 0.69 from CNY 0.57 a year ago. The company's earnings are forecast to grow significantly at an annual rate of 24.3%, outpacing the market's growth rate of 21.9%. With a price-to-earnings ratio of 18.4x, it offers good value compared to the CN market average of 27.2x and has high insider ownership supporting strong alignment with shareholder interests.

- Unlock comprehensive insights into our analysis of MayAir Technology (China) stock in this growth report.

- Our expertly prepared valuation report MayAir Technology (China) implies its share price may be too high.

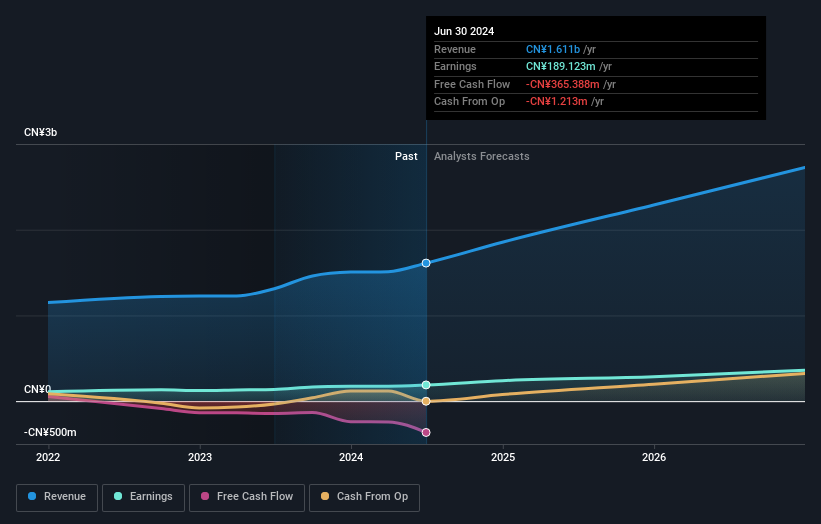

Shenzhen Yinghe Technology (SZSE:300457)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Shenzhen Yinghe Technology Co., Ltd specializes in the R&D, production, and sale of lithium-ion battery automation equipment in China with a market cap of CN¥9.33 billion.

Operations: Shenzhen Yinghe Technology generates revenue primarily from the research, development, production, and sale of lithium-ion battery automation equipment in China.

Insider Ownership: 19.3%

Revenue Growth Forecast: 17.6% p.a.

Shenzhen Yinghe Technology's earnings are forecast to grow significantly at 30.8% annually, outpacing the CN market's 21.9%. With a price-to-earnings ratio of 15.6x, it trades at good value compared to the market average of 27.2x. Despite a recent unstable dividend track record and low future return on equity (14.4%), its high insider ownership suggests strong alignment with shareholder interests, supporting its growth potential in China's competitive landscape.

- Click to explore a detailed breakdown of our findings in Shenzhen Yinghe Technology's earnings growth report.

- Our expertly prepared valuation report Shenzhen Yinghe Technology implies its share price may be lower than expected.

Pansoft (SZSE:300996)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Pansoft Company Limited offers enterprise management information solutions and IT integrated services in China, with a market cap of approximately CN¥3.18 billion.

Operations: Pansoft's revenue segments include enterprise management information solutions and IT integrated services in China.

Insider Ownership: 34.8%

Revenue Growth Forecast: 20.8% p.a.

Pansoft's earnings are projected to grow significantly at 25.2% annually, surpassing the CN market's 21.9%. The company's revenue is expected to increase by 20.8% per year, also outpacing the market average of 13.4%. Trading at a price-to-earnings ratio of 29.7x, below the industry average of 56.3x, it offers good value despite recent volatility and low forecasted return on equity (12.7%). Recent earnings results show improved profitability with sales rising to CNY191.99 million and net income reaching CNY13.39 million for H1 2024, reversing a prior loss.

- Navigate through the intricacies of Pansoft with our comprehensive analyst estimates report here.

- The valuation report we've compiled suggests that Pansoft's current price could be quite moderate.

Key Takeaways

- Click this link to deep-dive into the 374 companies within our Fast Growing Chinese Companies With High Insider Ownership screener.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:300457

Shenzhen Yinghe Technology

Engages in the research and development, production, and sale of lithium-ion battery automation equipment in China.

Flawless balance sheet and good value.