- China

- /

- Medical Equipment

- /

- SZSE:300633

Laopu Gold And 2 Other Stocks Possibly Trading At A Discount

Reviewed by Simply Wall St

As global markets continue to rally, with major indices like the Dow Jones Industrial Average and S&P 500 reaching record highs, investors are navigating a landscape influenced by geopolitical factors and domestic policy changes. Amid this environment of robust trading activity and economic reports that exceed expectations in some areas while lagging in others, identifying stocks that may be undervalued can present unique opportunities for investors seeking to capitalize on potential market inefficiencies. In such a context, understanding the fundamentals of what makes a stock potentially undervalued—such as strong financial health or growth potential not yet reflected in its price—becomes crucial for those looking to make informed investment decisions.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Corporativo Fragua. de (BMV:FRAGUA B) | MX$633.57 | MX$1257.07 | 49.6% |

| BP Plastics Holding Bhd (KLSE:BPPLAS) | MYR1.20 | MYR2.39 | 49.7% |

| Ramssol Group Berhad (KLSE:RAMSSOL) | MYR0.70 | MYR1.39 | 49.5% |

| Krsnaa Diagnostics (NSEI:KRSNAA) | ₹996.65 | ₹1971.74 | 49.5% |

| Equity Bancshares (NYSE:EQBK) | US$48.12 | US$96.15 | 50% |

| Pluk Phak Praw Rak Mae (SET:OKJ) | THB15.50 | THB30.86 | 49.8% |

| Acerinox (BME:ACX) | €9.92 | €19.82 | 49.9% |

| Nidaros Sparebank (OB:NISB) | NOK100.10 | NOK198.62 | 49.6% |

| Marcus & Millichap (NYSE:MMI) | US$40.88 | US$81.13 | 49.6% |

| FINEOS Corporation Holdings (ASX:FCL) | A$1.91 | A$3.77 | 49.4% |

Below we spotlight a couple of our favorites from our exclusive screener.

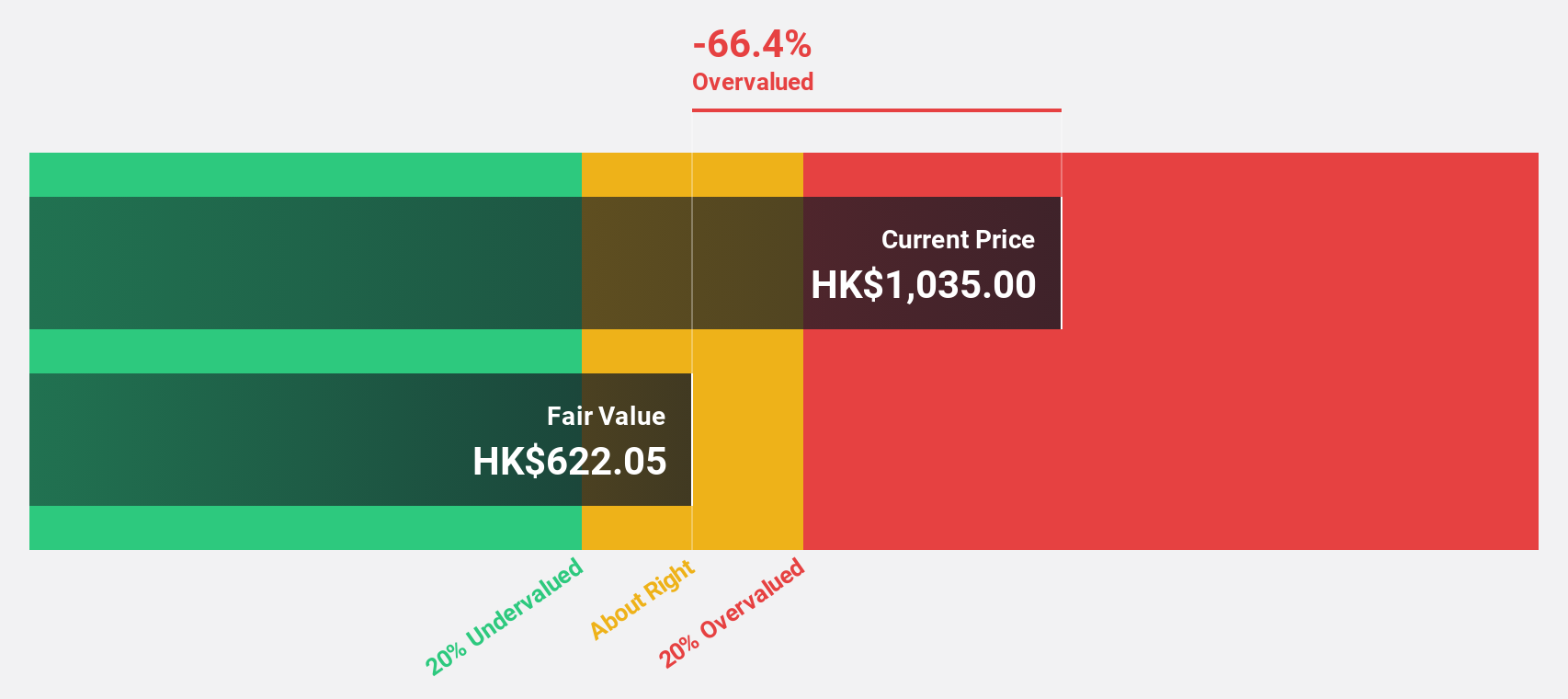

Laopu Gold (SEHK:6181)

Overview: Laopu Gold Co., Ltd. designs, manufactures, and sells jewelry products in Mainland China, Hong Kong, and Macau with a market capitalization of HK$33.08 billion.

Operations: The company's revenue primarily comes from its Jewelry & Watches segment, which generated CN¥5.28 billion.

Estimated Discount To Fair Value: 10.2%

Laopu Gold is trading at HK$196.5, below its fair value estimate of HK$218.74, indicating it may be undervalued based on cash flows. The company's earnings are forecast to grow significantly at 34.2% annually, outpacing the Hong Kong market's 11.3%. Revenue growth is also strong at 24.6% per year, surpassing market expectations of 7.7%. Recent amendments to its Articles of Association could impact governance but do not directly affect cash flow valuation metrics.

- Upon reviewing our latest growth report, Laopu Gold's projected financial performance appears quite optimistic.

- Take a closer look at Laopu Gold's balance sheet health here in our report.

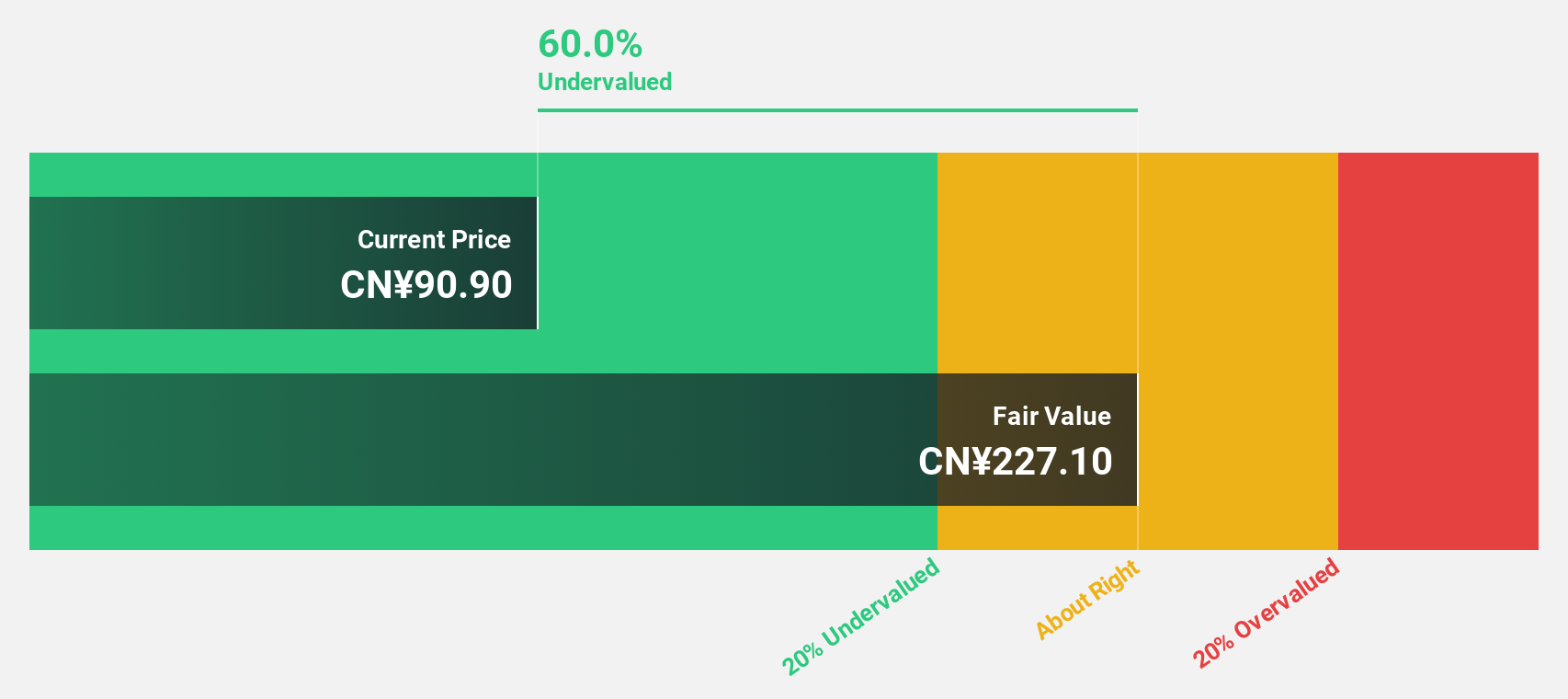

Asymchem Laboratories (Tianjin) (SZSE:002821)

Overview: Asymchem Laboratories (Tianjin) Co., Ltd. operates as a contract development and manufacturing organization (CDMO) providing services to the pharmaceutical industry, with a market cap of CN¥27.27 billion.

Operations: The company generates revenue from its Pharmaceutical Technology segment, amounting to CN¥5.57 billion.

Estimated Discount To Fair Value: 4%

Asymchem Laboratories (Tianjin) is trading slightly below its estimated fair value of CN¥88.45, with a current price of CN¥84.9, suggesting potential undervaluation based on cash flows. Despite recent earnings declines, with net income dropping to CNY 710.33 million from CNY 2,210.11 million year-on-year, the company's revenue and earnings are projected to grow faster than the Chinese market at 17.9% and 29.9% annually respectively, indicating robust future prospects despite current challenges.

- According our earnings growth report, there's an indication that Asymchem Laboratories (Tianjin) might be ready to expand.

- Click here to discover the nuances of Asymchem Laboratories (Tianjin) with our detailed financial health report.

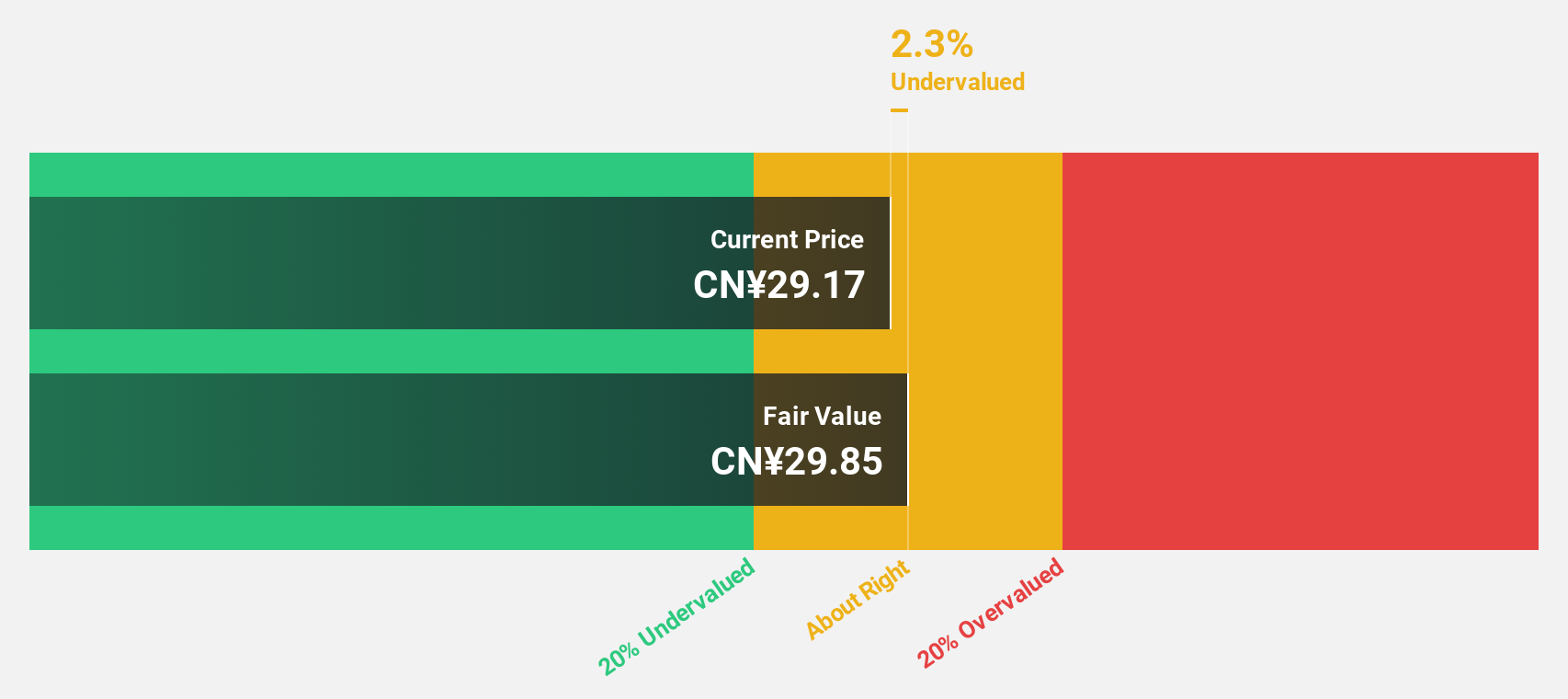

SonoScape Medical (SZSE:300633)

Overview: SonoScape Medical Corp. focuses on the research, development, production, and sales of medical diagnosis and treatment equipment both in China and internationally, with a market cap of CN¥14.73 billion.

Operations: The company generates revenue of CN¥2.05 billion from its medical device industry segment.

Estimated Discount To Fair Value: 15.7%

SonoScape Medical is trading at CN¥34.89, below its fair value estimate of CN¥41.39, reflecting potential undervaluation based on cash flows. Despite a decline in net income to CN¥108.99 million from CN¥320.62 million year-on-year, its earnings are forecast to grow significantly at 54.4% annually, outpacing the Chinese market's 26.2%. However, recent profit margins have decreased and dividends remain inadequately covered by free cash flows, posing potential risks for investors.

- Our growth report here indicates SonoScape Medical may be poised for an improving outlook.

- Get an in-depth perspective on SonoScape Medical's balance sheet by reading our health report here.

Next Steps

- Discover the full array of 889 Undervalued Stocks Based On Cash Flows right here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:300633

SonoScape Medical

Engages in the research and development, production, and sales of medical diagnosis and treatment equipment in China and internationally.

Flawless balance sheet with high growth potential.