Advertisement

- Switzerland

- /

- Food

- /

- SWX:NESN

Is There an Opportunity in Nestlé Shares After Recent Plant-Based Expansion?

Simply Wall St

Reviewed by Bailey Pemberton

- Wondering if now is the right time to buy or hold Nestlé stock? You are not alone, especially if you are searching for a genuinely good value in a market full of surprises.

- Nestlé's share price has seen some ups and downs lately. It slipped 1.2% over the past week but climbed 6.9% since the start of the year, and finished 8.1% higher over the last 12 months. This hints at growing optimism or shifting risk perceptions among investors.

- Recent headlines have focused on Nestlé's push into new product categories and sustainability initiatives. These efforts have caught the market's attention and provided fresh context for the price movements. Major investments in plant-based products and efforts to streamline its portfolio have also generated plenty of conversation about the company's future growth prospects.

- On our valuation checklist, Nestlé gets a score of 4 out of 6 for being undervalued across several metrics. We will break down how this score was reached with a closer look at common valuation methods, and later in the article, reveal why there may be an even smarter way to assess Nestlé's fair value.

Approach 1: Nestlé Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company’s intrinsic value by projecting its future cash flows and discounting them back to today’s value. This method weighs not just how much Nestlé generates right now, but also how its profits could grow in the years to come.

Nestlé’s most recent Free Cash Flow stands at CHF 8.8 Billion. According to available analyst estimates, this figure is expected to grow in the coming years, with forecasts reaching CHF 11.9 Billion by 2029. Since analysts only predict up to five years out, further projections rely on extrapolations by Simply Wall St, reflecting expectations for steady progress rather than dramatic spikes.

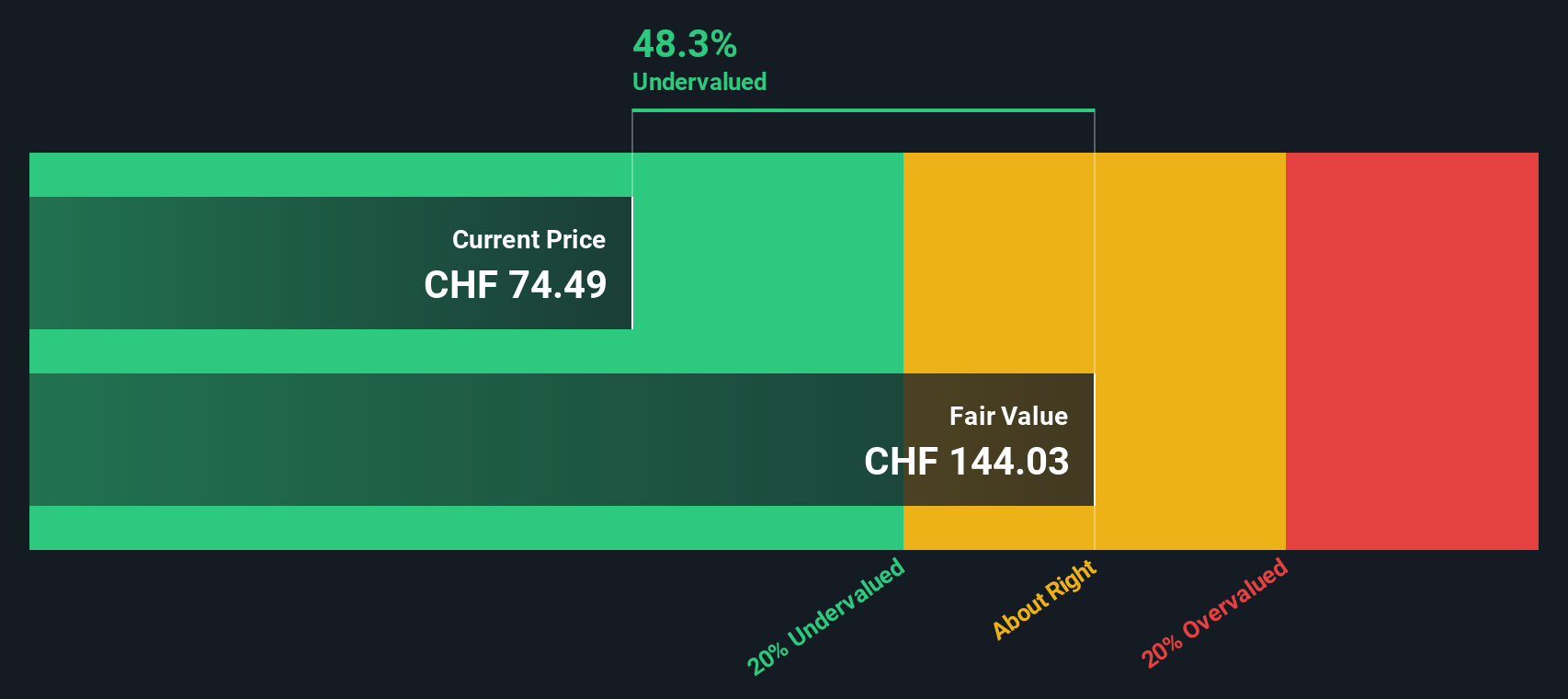

Running these cash flow figures through a 2 Stage Free Cash Flow to Equity model, the estimated fair value per share stands at CHF 142.81. This means that, based on these projections, Nestlé shares are trading at a 44.1% discount to their intrinsic value. This suggests the stock could be significantly undervalued relative to its long-term cash generating potential.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Nestlé is undervalued by 44.1%. Track this in your watchlist or portfolio, or discover 920 more undervalued stocks based on cash flows.

Approach 2: Nestlé Price vs Earnings

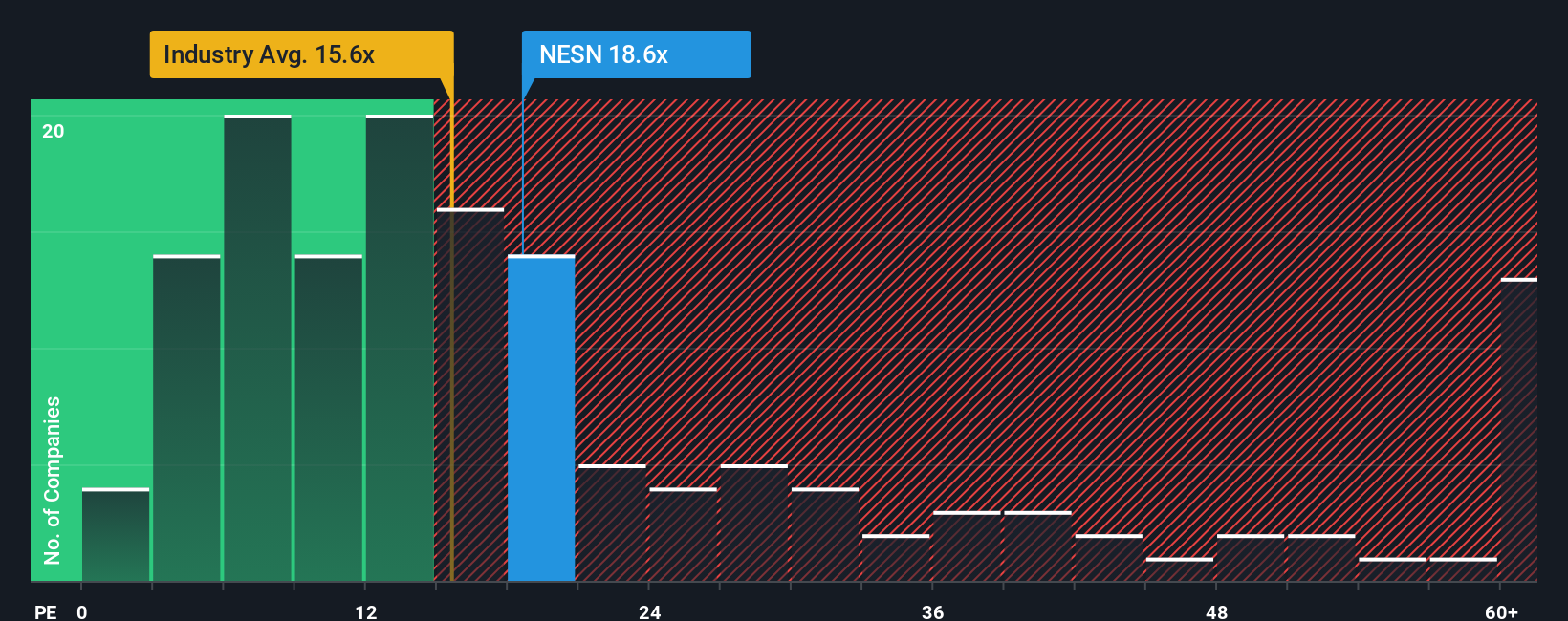

The Price-to-Earnings (PE) ratio is a widely used metric for valuing established, profitable companies like Nestlé. It tells investors how much they are paying for each franc of the company’s earnings and provides a straightforward way to compare stocks within the same industry.

The appropriate PE ratio for a business depends on several factors. Robust growth prospects or lower perceived risks tend to justify higher multipliers, while slower growth or higher uncertainty usually mean lower ones. In essence, the “right” PE reflects not only current performance but also future potential and stability.

Nestlé currently trades at a PE of 19.9x. For context, the average PE for its Food industry peers is 16.0x, and the selected peer group has an average of 27.7x. These reference points suggest that Nestlé is priced above the sector average but still below many of its closest competitors.

Beyond these basic benchmarks, Simply Wall St’s Fair Ratio model calculates a justifiable PE for Nestlé based on its unique combination of projected earnings growth, profit margin strength, position in the industry, market cap, and risk factors. This proprietary Fair Ratio for Nestlé is estimated at 27.2x, providing a more comprehensive view than broad sector or peer averages.

Comparing Nestlé’s actual PE of 19.9x with its Fair Ratio of 27.2x suggests that the stock is trading well below where it could be based on its fundamentals and prospects.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1443 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Nestlé Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is your own story of what you think will happen with a company—it is where you bring together your view on the business, key assumptions about future revenue, earnings, and margins, and arrive at a fair value that fits your perspective, not just the averages. Narratives connect the company’s story with dynamic financial forecasts, allowing you to see how your outlook translates into a fair value estimate.

With Narratives, available right within Simply Wall St’s Community page, you can easily make and refine your call as the market changes. Millions of investors use these as an accessible way to capture not just what the numbers say, but why they matter. When new information hits (like news, earnings, or CEO changes), your Narrative and its fair value update in real-time, helping you decide if it is a buy, hold, or sell at today’s price.

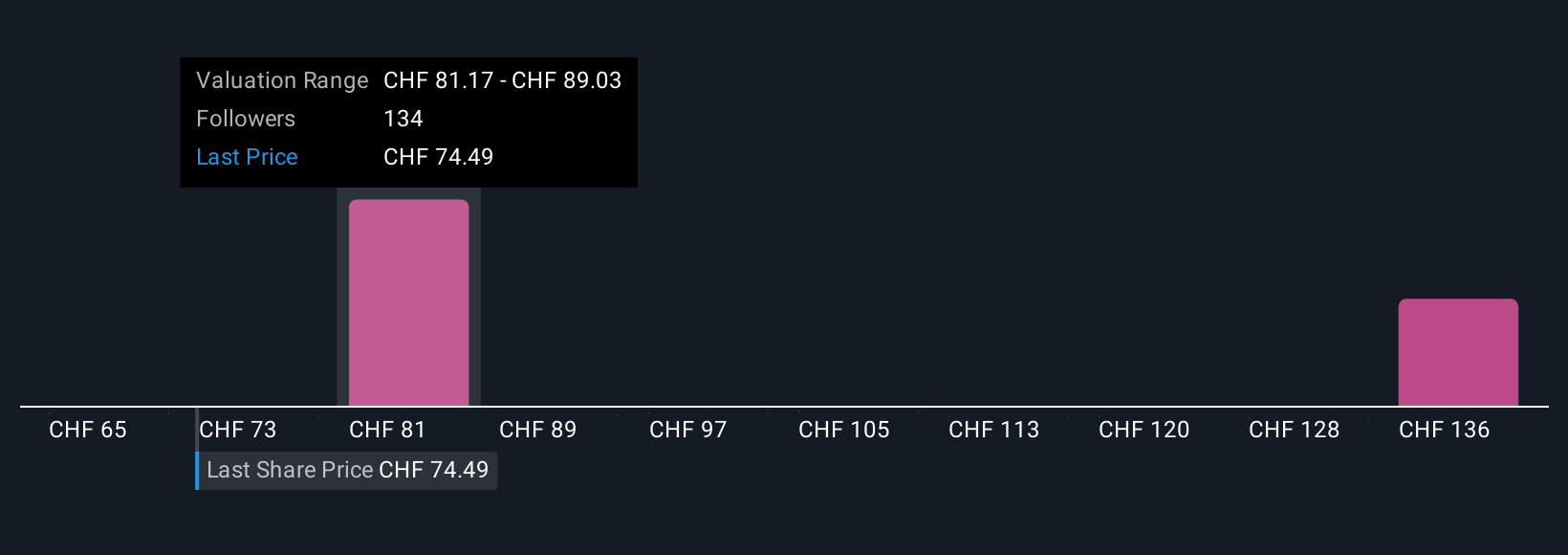

For Nestlé, some investors see premiumization and cost-cutting driving earnings growth and set targets above CHF 100, while others worry about weak demand and margin pressure, arriving closer to CHF 71. Your Narrative lets you choose the story, assumptions, and price that make sense to you.

Do you think there's more to the story for Nestlé? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Nestlé might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SWX:NESN

Established dividend payer and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative