Advertisement

- Canada

- /

- Transportation

- /

- TSX:CNR

Is Canadian National Railway's Fresh Debt Issuance Shaping Its Financial Flexibility Story (TSX:CNR)?

Simply Wall St

Reviewed by Sasha Jovanovic

- Canadian National Railway Company recently completed a series of fixed-income offerings amounting to over US$690 million, while also releasing its 2025 Investor Fact Book outlining updated growth expectations and economic forecasts.

- This combination of debt issuance and forward-looking disclosure signals an active approach to capital management and transparency on how evolving macroeconomic trends could influence operational and financial outcomes.

- We'll assess how CN's recent funding through fixed-income offerings could impact its investment outlook and financial flexibility.

Find companies with promising cash flow potential yet trading below their fair value.

Canadian National Railway Investment Narrative Recap

To be comfortable as a Canadian National Railway shareholder, you need to believe in the long-term resilience of North American rail freight and CN’s ability to convert its expansive network into steady profit growth, even when demand appears muted. While CN’s recent US$690 million fixed-income offerings strengthen its financial flexibility, this capital action alone isn’t likely to shift the company’s key short-term catalyst, volume improvement across its core business lines, or fundamentally alter the biggest risk: persistent macroeconomic and trade-related headwinds keeping top-line growth in check.

In the context of recent news, the just-approved quarterly dividend of CA$0.8875 per share remains a relevant signal of CN’s ongoing commitment to regular shareholder returns, even as management continues to target improved efficiency and balanced capital allocation. The dividend affirmation underscores financial stability but does not eliminate uncertainty around volume recovery, which remains crucial to future earnings growth.

By contrast, investors should also be keenly aware of how global trade tensions and ongoing tariff risks could still affect CN’s ability to...

Read the full narrative on Canadian National Railway (it's free!)

Canadian National Railway's outlook forecasts CA$19.6 billion in revenue and CA$5.6 billion in earnings by 2028. This assumes annual revenue growth of 4.6% and a CA$1.0 billion increase in earnings from the current CA$4.6 billion.

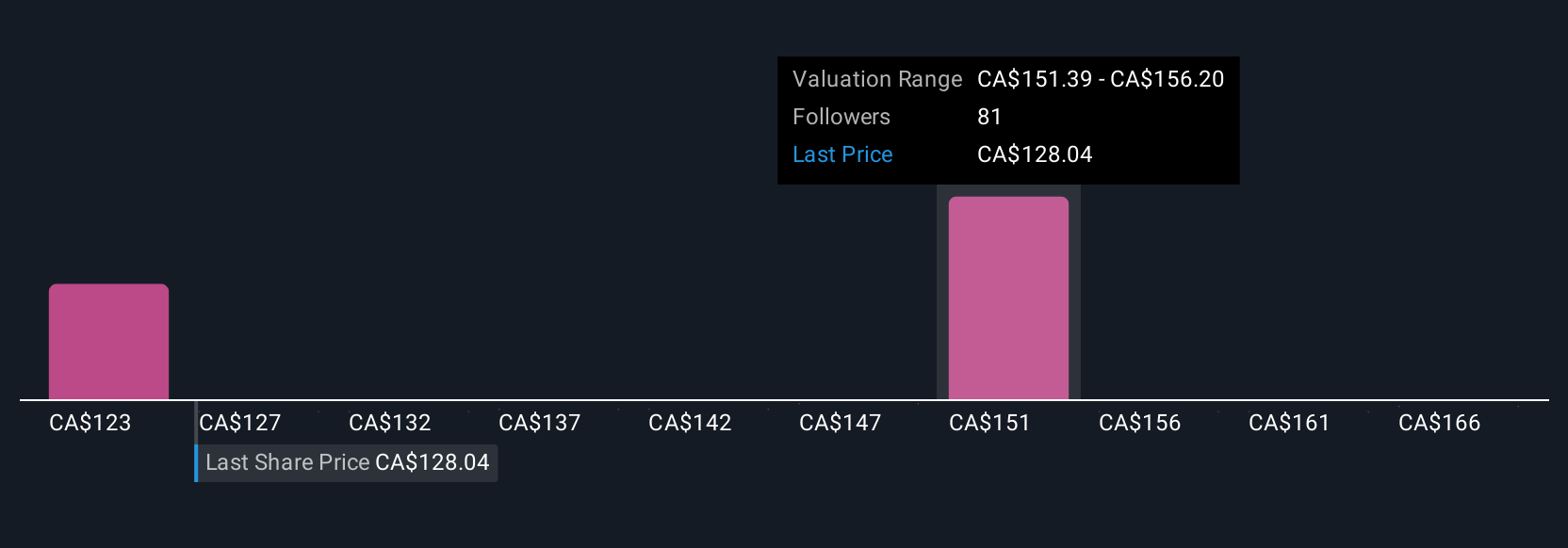

Uncover how Canadian National Railway's forecasts yield a CA$150.57 fair value, a 13% upside to its current price.

Exploring Other Perspectives

Fourteen members of the Simply Wall St Community estimate CN’s fair value between CA$116.67 and CA$156.78 per share. Amid these views, ongoing macroeconomic uncertainty remains a central challenge for future earnings, encouraging you to consider multiple opinions on risks and catalysts.

Explore 14 other fair value estimates on Canadian National Railway - why the stock might be worth as much as 18% more than the current price!

Build Your Own Canadian National Railway Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Canadian National Railway research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Canadian National Railway research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Canadian National Railway's overall financial health at a glance.

No Opportunity In Canadian National Railway?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- We've found 16 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:CNR

Canadian National Railway

Engages in the rail, intermodal, trucking, and related transportation businesses in Canada and the United States.

Established dividend payer and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|7.6% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.5% undervalued

YI

Community Contributor