Advertisement

- Canada

- /

- Metals and Mining

- /

- TSXV:MJS

Majestic Gold (TSXV:MJS) Margin Decline Challenges Bulls Despite Revenue Growth in Q3 2025

Simply Wall St

Reviewed by Simply Wall St

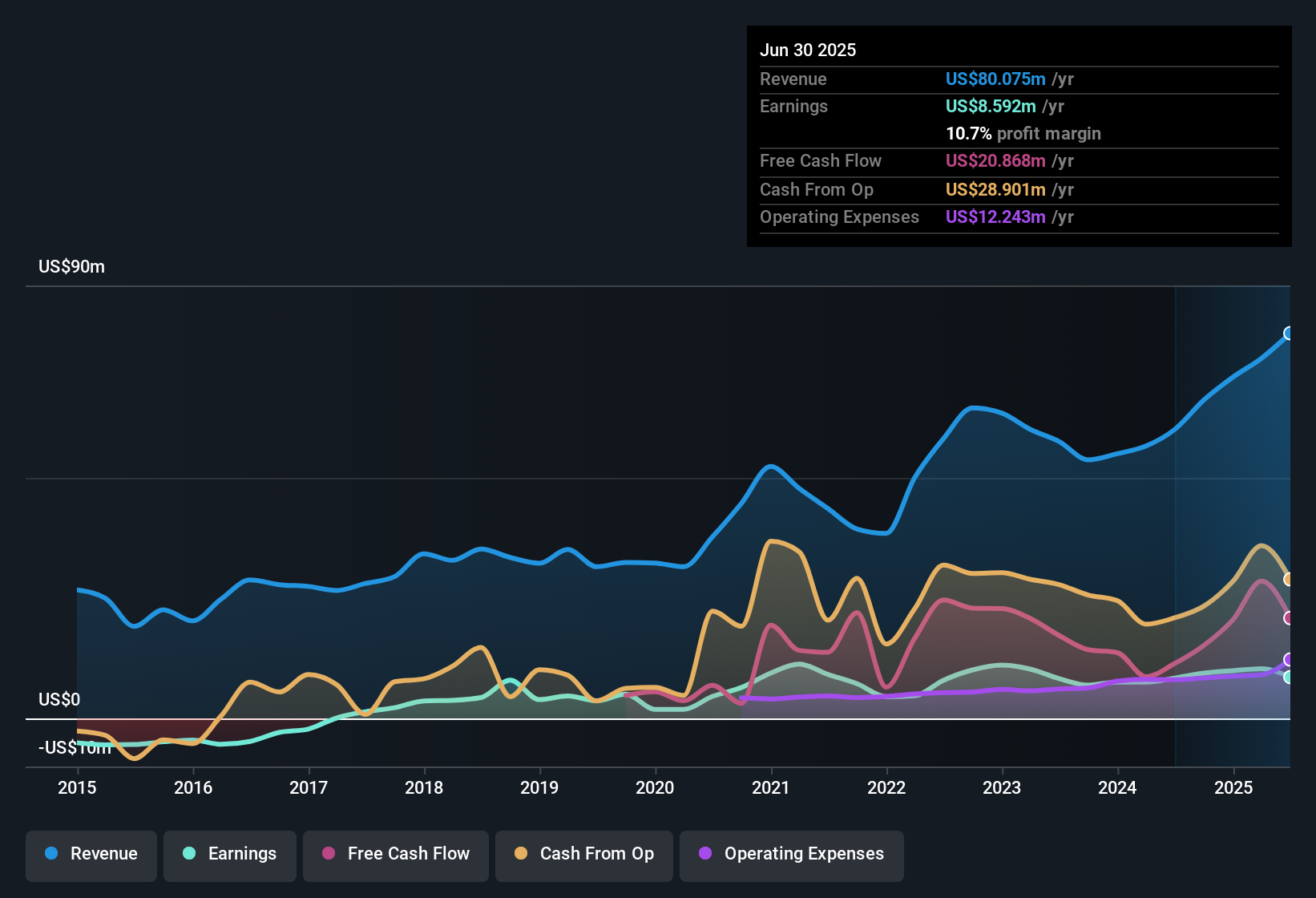

Majestic Gold (TSXV:MJS) has just released its Q3 2025 results, posting revenue of $23.3 million with basic EPS of $0.0011 and net income of $1.1 million. The company has seen revenue grow from $18.3 million in Q3 2024 to $23.3 million this quarter, while EPS moved from $0.0029 to $0.0011 over the same period. Margins took a hit this time around, so investors will be watching closely to see how this plays into the longer-term profitability story.

See our full analysis for Majestic Gold.Now, let's see how these results compare with the prevailing narratives about Majestic Gold, both from the market and the Simply Wall St community.

Curious how numbers become stories that shape markets? Explore Community Narratives

DCF Valuation Discount Stands Out

- At a current share price of $0.16, Majestic Gold trades 76.1% below the DCF fair value estimate of $0.67 per share.

- Investors attracted to undervalued stocks will notice that the company’s price-to-earnings ratio is just 13.9x, well under both the Canadian Metals and Mining industry average of 19.3x and the peer group’s 34.2x.

- This substantial discount strongly supports the argument that Majestic Gold could represent a value opportunity if the business can maintain stable or growing profits.

- Bulls point to steady earnings quality and a multi-year record of profit growth as adding weight to the view that the discount is not simply a reflection of risk.

Profit Margins Shrink Amid Rising Revenue

- Net profit margin fell to 10.7% for the latest twelve months, compared to 14% in the previous year, even as total revenue climbed to $80.1 million from $66.2 million year over year.

- While many see revenue gains as a good sign, the margin contraction highlights a core tension identified in prevailing market analysis: growth has come with profitability pressures.

- The opposing pull between top-line expansion and cost control presents a challenge to hopes for margin-driven earnings upside.

- Cautious investors will be observant to see if recent cost pressures persist or are just a temporary bump.

Earnings Growth Slows Below Historical Trend

- Earnings rose just 2.5% in the last twelve months, underperforming the company’s 3.1% five-year average annual growth rate.

- This moderation in the growth rate signals caution for those seeking acceleration and fits with the wider theme in market commentary: Majestic’s recent performance reflects consistency and durability more than breakout potential.

- For investors, the slower earnings trajectory emphasizes the value angle over high-octane growth stories.

- The latest results suggest steady, incremental gains rather than significant jumps in profitability or risk.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Majestic Gold's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Majestic Gold’s shrinking profit margins and slowing earnings growth reveal pressure on its ability to deliver high returns and expand profitability in the future.

If you want more consistent performance across ups and downs, check out stable growth stocks screener (2075 results) for companies that keep revenue and earnings growing steadily through different market cycles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSXV:MJS

Majestic Gold

A mining company, focuses on exploration, development, and operation of mining properties in China.

Excellent balance sheet and good value.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SW

swift11 on DXC Technology ·

CEO: We are winners in the long term in the AI world

Fair Value:US$17.4624.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7924.0% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative