Advertisement

Is Fairfax Financial a Bargain After 470% Five Year Surge and Global Acquisition Push?

Simply Wall St

Reviewed by Bailey Pemberton

- Wondering if Fairfax Financial Holdings is fairly priced or a hidden bargain? You are not alone, as many investors are watching closely to see if now is the right time to jump in or hold steady.

- The stock has delivered a steady 21.7% gain year-to-date, with a 6.8% bump in the last month and an eye-catching 470.0% return over five years, catching the attention of both long-term holders and newcomers.

- Recent headlines have highlighted Fairfax’s ongoing global acquisitions strategy. The company is expanding its international insurance footprint and drawing both praise and scrutiny from analysts. These deals, along with market chatter about sector consolidation, have contributed to a renewed debate around the company’s true worth.

- Right now, Fairfax scores 5 out of 6 on our valuation checks, suggesting it is undervalued across most key measures. However, as you will see, traditional ratios do not always tell the whole story, and there is an even better way to assess its value coming up later in the article.

Approach 1: Fairfax Financial Holdings Excess Returns Analysis

The Excess Returns valuation method estimates how much more profit a company generates on its invested capital compared to the minimum return required by shareholders, known as the cost of equity. This approach focuses on sustainable profitability and growth in book value to determine a company’s intrinsic worth.

For Fairfax Financial Holdings, analysts estimate a stable earnings per share (EPS) of CA$200.63, derived from future return on equity projections by six analysts. The company’s current book value per share stands at CA$1,203.65, with a cost of equity assessed at CA$82.57 per share. The resulting excess return is CA$118.07 per share, and the projected stable book value is CA$1,349.56 per share. The average return on equity is a healthy 14.87%, which is considered strong for the sector.

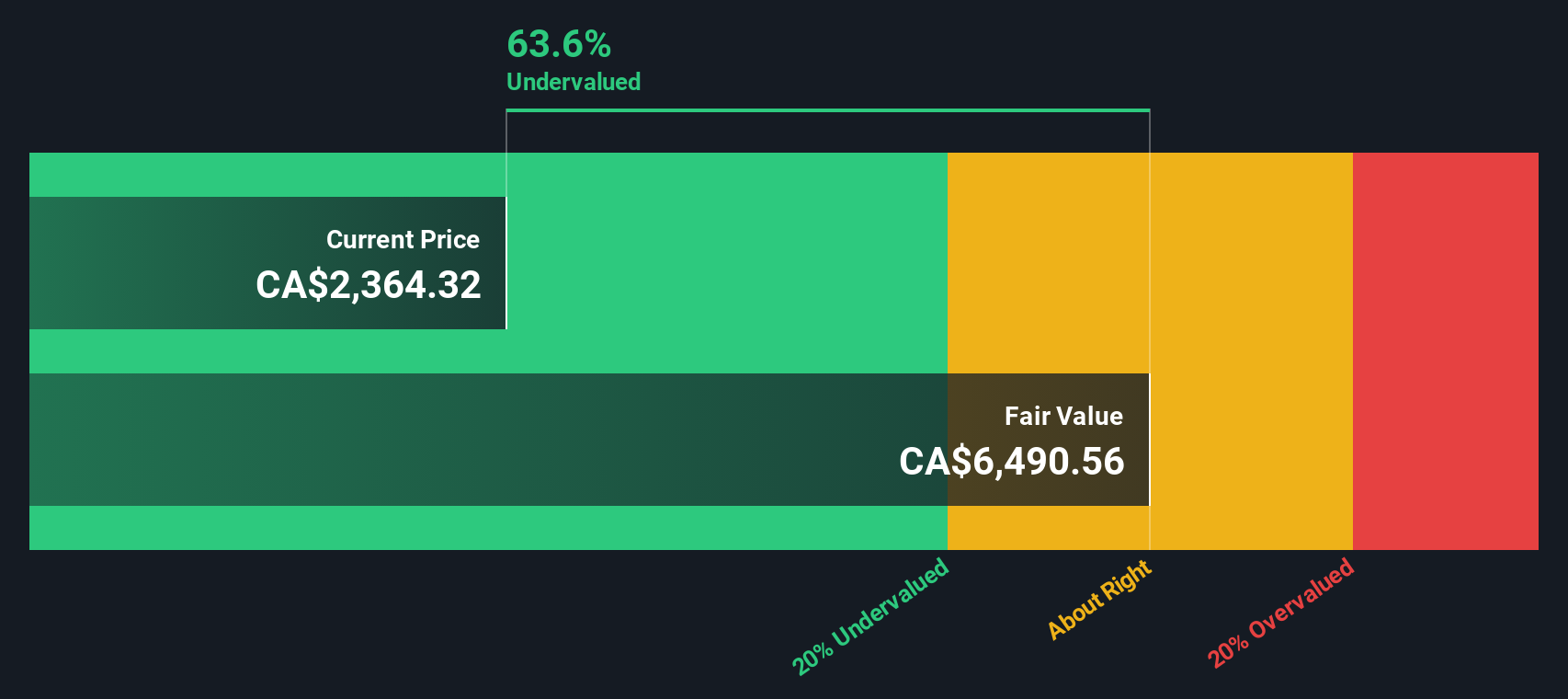

Based on these inputs, the Excess Returns model calculates the estimated intrinsic value of Fairfax Financial Holdings at 64.5% below its current share price. This suggests the shares are significantly undervalued compared to what the company should be worth if it maintains its current performance.

Result: UNDERVALUED

Our Excess Returns analysis suggests Fairfax Financial Holdings is undervalued by 64.5%. Track this in your watchlist or portfolio, or discover 920 more undervalued stocks based on cash flows.

Approach 2: Fairfax Financial Holdings Price vs Earnings

The price-to-earnings (PE) ratio is a widely used metric for assessing the value of profitable companies like Fairfax Financial Holdings. It relates the company’s current share price to its earnings per share, making it a practical tool for comparing a company’s valuation against its historical averages, peers, and the broader industry.

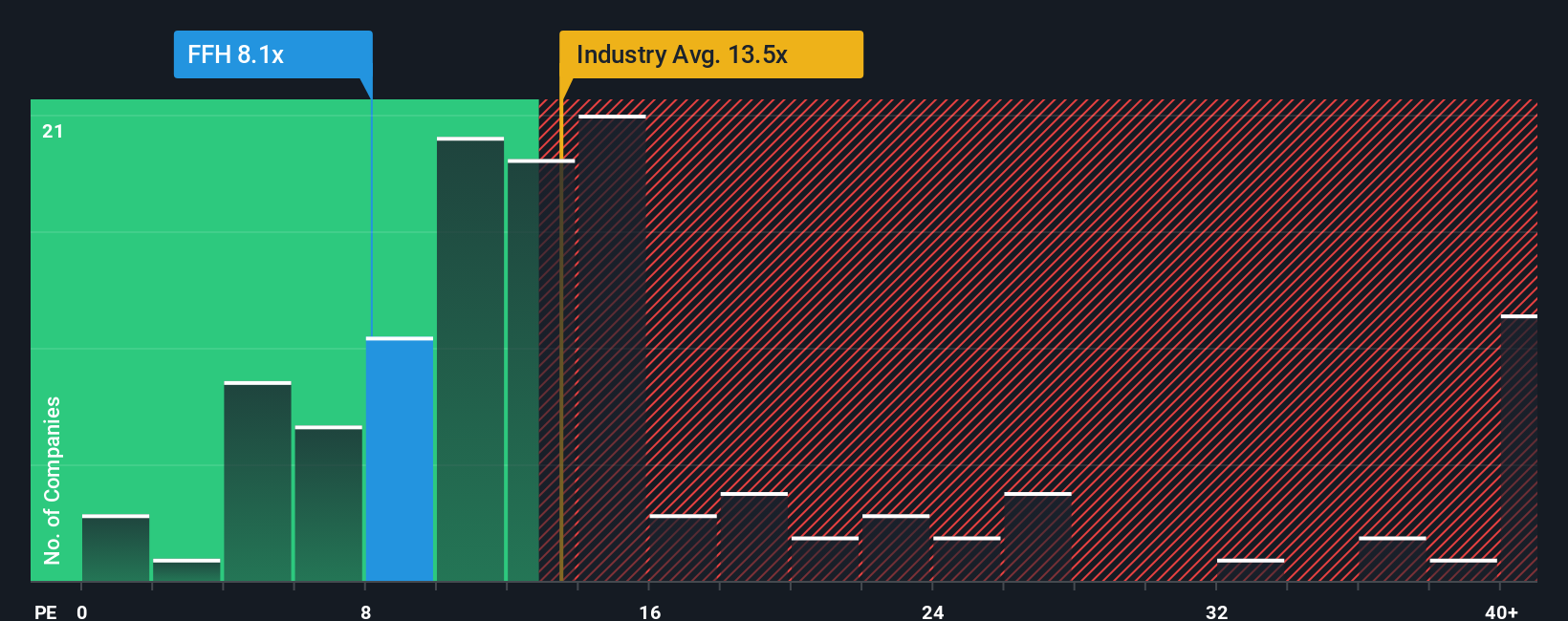

What counts as a “normal” or “fair” PE ratio depends on a company’s growth prospects and risk profile. Higher growth expectations or lower risk typically justify a higher PE, whereas mature or riskier businesses tend to command lower multiples. Currently, Fairfax trades at a PE ratio of 8.1x, which is well below both the insurance industry average of 11.7x and the peer group average of 16.6x. This suggests the market may be undervaluing the stock relative to broader benchmarks.

A more nuanced approach is to use the Simply Wall St “Fair Ratio,” which is calculated based on factors such as Fairfax’s earnings growth potential, profit margins, risks, size, and its place within the industry. This method goes beyond broad peer or industry comparisons by considering what is actually reasonable for Fairfax specifically. For Fairfax Financial Holdings, the Fair Ratio is set at 8.3x. Since this is just above the company’s current PE ratio, the stock appears to be priced about right based on its bespoke Fair Ratio.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1443 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Fairfax Financial Holdings Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is simply your story about a company, combining your perspective on its future prospects with your own assumptions about fair value, expected revenue, earnings, and profit margins. More than just numbers, Narratives connect the company’s bigger picture such as strategy, risks, growth drivers, and industry changes to your financial forecast, resulting in a unique fair value estimate.

Narratives are a flexible and accessible tool available to all investors through Simply Wall St’s platform, where millions contribute their perspectives in the Community page. By comparing your own Narrative-driven Fair Value with the current market price, you gain clarity on whether it is time to buy, hold, or sell. The Narrative is updated automatically whenever new information, such as earnings or news, emerges.

For example, one investor might take a cautious view due to currency risks and project a fair value of only CA$1,649 per share, while another sees long-term value creation from acquisitions and capital discipline, giving a bullish fair value above CA$2,990 per share. Your Narrative reflects what you believe, not just what analysts expect, making it a practical, dynamic guide for smarter decision making.

Do you think there's more to the story for Fairfax Financial Holdings? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:FFH

Fairfax Financial Holdings

Through its subsidiaries, provides property and casualty insurance and reinsurance, and investment management services in the United States, Canada, the Middle East, Asia, and internationally.

Undervalued with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7924.0% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative