Advertisement

- Canada

- /

- Oil and Gas

- /

- TSXV:HME

Hemisphere Energy (TSXV:HME) Margins Hold Above 38%, Defying Bearish Profitability Narratives

Simply Wall St

Reviewed by Simply Wall St

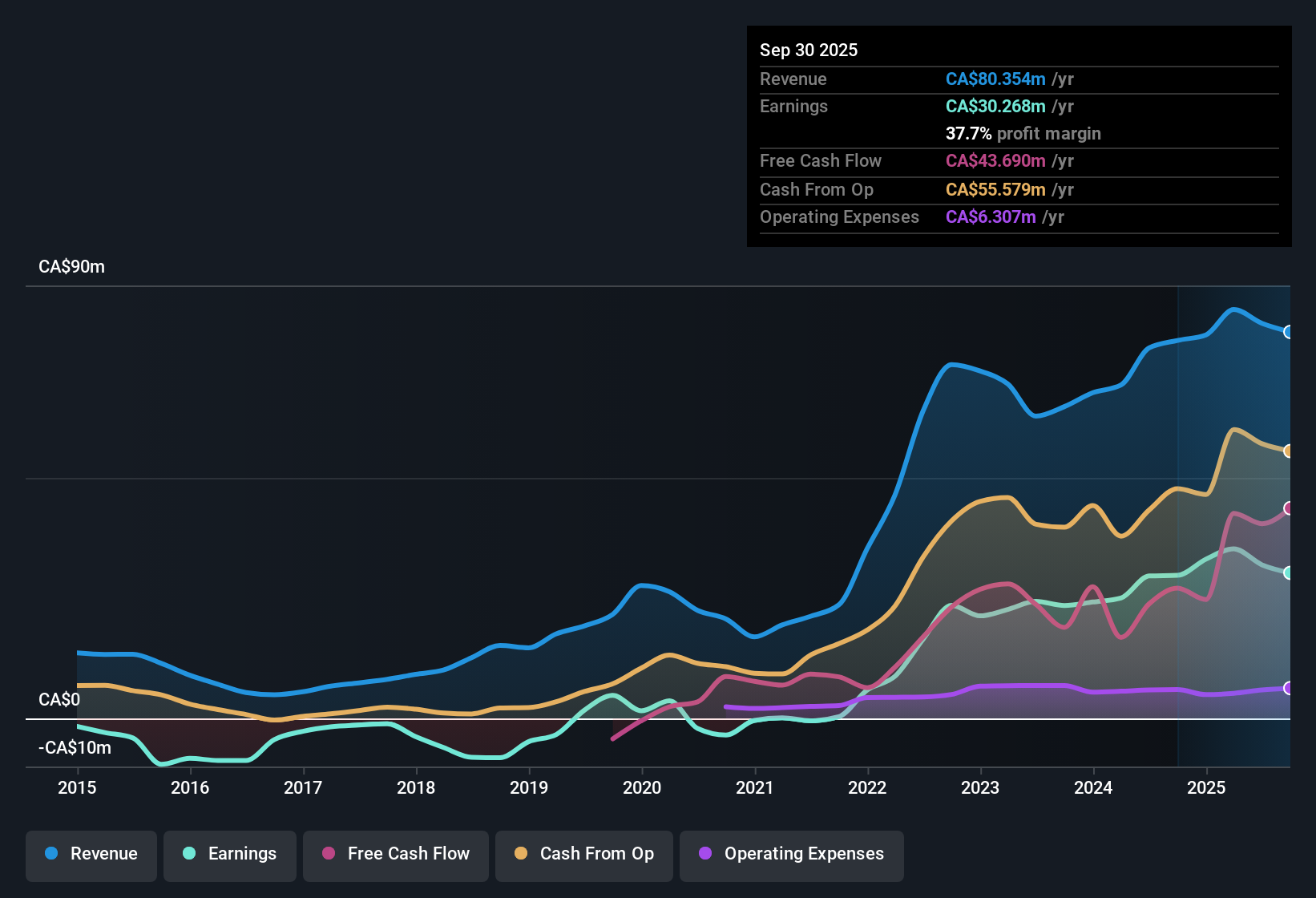

Hemisphere Energy (TSXV:HME) posted Q3 2025 results with total revenue of 19.1 million CAD and basic EPS of 0.07 CAD, alongside net income of 6.9 million CAD. Over the past twelve months, the company has seen revenue move from 79.0 million CAD to 79.7 million CAD while EPS grew from 0.30 CAD to 0.32 CAD, framing a stable trend for topline and earnings measures. With solid profit margins maintained, the latest report should give investors plenty to discuss around profitability and future expectations.

See our full analysis for Hemisphere Energy.Next, we will set these headline numbers side by side with the prevailing narratives. Some may get confirmed and others could be in for a shakeup.

Curious how numbers become stories that shape markets? Explore Community Narratives

Margins Top 38% as Costs Stay in Check

- Net profit margin stood at 38.3% over the past year, up from 37.9% the prior year, aided by production costs per BOE staying near 11.4 CAD in the latest quarter.

- What is notable is that even though realized oil prices in Q3 2025 dropped to 70.33 CAD per barrel (down from 79.58 CAD in Q1 2025), Hemisphere Energy continued to post strong margins, challenging any assumption that the company’s profitability is strictly dictated by commodity swings.

- This resilience supports the view that cost control remains a key lever.

- Consensus narrative notes that modest margin gains and controlled expenses underpin overall business stability, even as topline growth slows.

Low P/E Signals Deep Value vs Peers

- Hemisphere trades at a price-to-earnings ratio of 6.1x, undercutting the peer group average (8.1x), industry (14.7x), and Canadian market (16.1x).

- Analysts’ consensus view points out that this discount valuation looks attractive against recent net income of 30.3 million CAD for the last twelve months, but the current share price (1.96 CAD) is well above the DCF fair value of 0.74 CAD and concerns about future earnings declines may overshadow the value argument.

- The consensus highlights that while trailing multiples entice bargain hunters, future earning risks can limit upside potential.

- Comparing today’s 6.1x P/E to a DCF fair value well below market price, the market is perhaps more cautious than the headline multiple suggests.

Top-Line Growth Slows Amid Forecasted Profit Drop

- Over the past year, revenue inched up just 1.5% (from 79.0 million CAD to 79.7 million CAD), but forecasts now point to a 13% annual decline in earnings through 2028.

- Critics highlight a key concern: even with an impressive five-year average earnings growth of 42.8% per year, the looming prospect of negative earnings growth weighs heavily.

- Bears argue that recent momentum in margins and profits could quickly fade if analyst forecasts prove correct.

- Balanced narrative remarks that modest sales growth and pressured outlook sharpen the focus on future strategy and operating leverage.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Hemisphere Energy's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

With earnings forecast to decline and the share price sitting well above fair value, Hemisphere’s outlook appears challenged by valuation concerns and future growth risks.

To target better balance between price and prospect, check out these 926 undervalued stocks based on cash flows to immediately see which companies offer stronger value versus their fundamentals today.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Hemisphere Energy might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSXV:HME

Hemisphere Energy

Acquires, explores, develops, and produces petroleum and natural gas properties in Canada.

Flawless balance sheet with solid track record and pays a dividend.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

75 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8147.4% undervalued

9 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

89 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

926 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative