Advertisement

- Canada

- /

- Real Estate

- /

- CNSX:PWR

Captiva Verde Wellness And 2 Other TSX Penny Stocks To Watch

Simply Wall St

Reviewed by Simply Wall St

The Canadian market has been grappling with slower consumer spending, influenced by a decline in the auto sector and sluggish population growth, while the U.S. faces uncertainty due to Federal Reserve policy decisions amidst disrupted economic data collection. Despite these challenges, penny stocks remain an intriguing investment area for those seeking opportunities in smaller or newer companies that offer potential growth at lower price points. By focusing on stocks with strong balance sheets and solid fundamentals, investors can uncover hidden gems that may provide stability and upside potential in today's complex market landscape.

Top 10 Penny Stocks In Canada

| Name | Share Price | Market Cap | Rewards & Risks |

| Westbridge Renewable Energy (TSXV:WEB) | CA$2.11 | CA$54.1M | ✅ 3 ⚠️ 4 View Analysis > |

| Zoomd Technologies (TSXV:ZOMD) | CA$2.00 | CA$199.57M | ✅ 4 ⚠️ 1 View Analysis > |

| Montero Mining and Exploration (TSXV:MON) | CA$0.43 | CA$3.59M | ✅ 2 ⚠️ 4 View Analysis > |

| CEMATRIX (TSX:CEMX) | CA$0.33 | CA$50.32M | ✅ 3 ⚠️ 1 View Analysis > |

| Monument Mining (TSXV:MMY) | CA$1.07 | CA$355.45M | ✅ 3 ⚠️ 1 View Analysis > |

| Thor Explorations (TSXV:THX) | CA$1.23 | CA$791.7M | ✅ 3 ⚠️ 2 View Analysis > |

| Automotive Finco (TSXV:AFCC.H) | CA$1.14 | CA$22.2M | ✅ 2 ⚠️ 4 View Analysis > |

| Pulse Seismic (TSX:PSD) | CA$2.77 | CA$140.59M | ✅ 2 ⚠️ 1 View Analysis > |

| Hemisphere Energy (TSXV:HME) | CA$1.96 | CA$185.61M | ✅ 3 ⚠️ 2 View Analysis > |

| Matachewan Consolidated Mines (TSXV:MCM.A) | CA$0.77 | CA$10.92M | ✅ 2 ⚠️ 3 View Analysis > |

Click here to see the full list of 402 stocks from our TSX Penny Stocks screener.

Let's review some notable picks from our screened stocks.

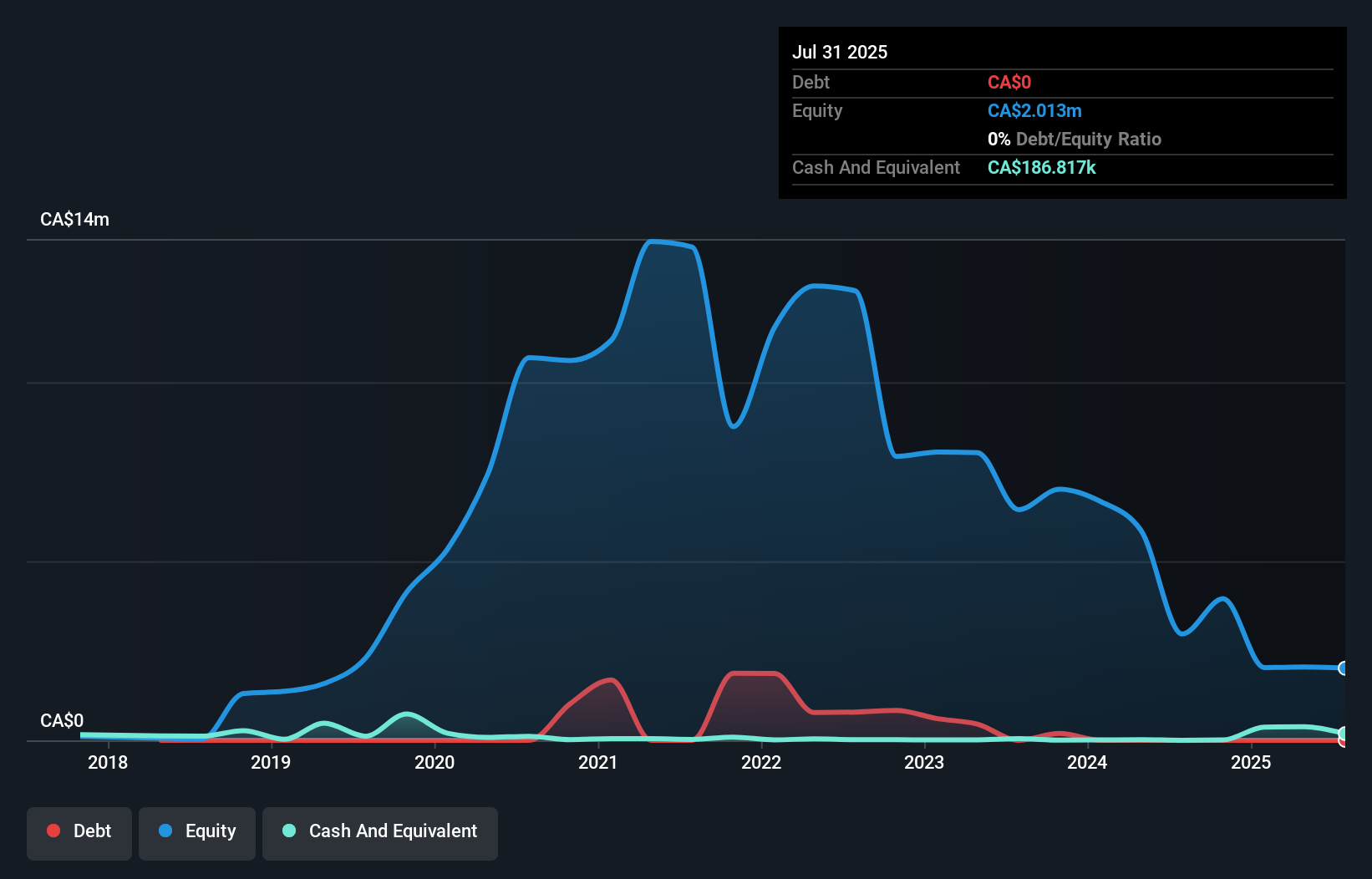

Captiva Verde Wellness (CNSX:PWR)

Simply Wall St Financial Health Rating: ★★★★★☆

Overview: Captiva Verde Wellness Corp. operates as a real estate company with a market cap of CA$9.04 million.

Operations: Captiva Verde Wellness Corp. does not have any reported revenue segments.

Market Cap: CA$9.04M

Captiva Verde Wellness Corp., with a market cap of CA$9.04 million, is pre-revenue and operates without debt or long-term liabilities, reducing financial risk. Despite its small size, the company has become profitable this year and boasts an outstanding return on equity of 96.8%. However, it faces challenges with short-term liabilities exceeding assets by CA$0.7 million and high share price volatility over the past three months. The company's Price-to-Earnings ratio of 6.2x suggests it may be undervalued compared to the broader Canadian market average of 16.1x, though investors should consider its high non-cash earnings level and inexperienced board before proceeding further.

- Click here and access our complete financial health analysis report to understand the dynamics of Captiva Verde Wellness.

- Understand Captiva Verde Wellness' track record by examining our performance history report.

Arrow Exploration (TSXV:AXL)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: Arrow Exploration Corp. is a junior oil and gas company involved in the acquisition, exploration, development, and production of oil and gas properties in Colombia and Western Canada with a market cap of CA$61.46 million.

Operations: The company's revenue is primarily derived from its oil and gas exploration and production activities, totaling $79.55 million.

Market Cap: CA$61.46M

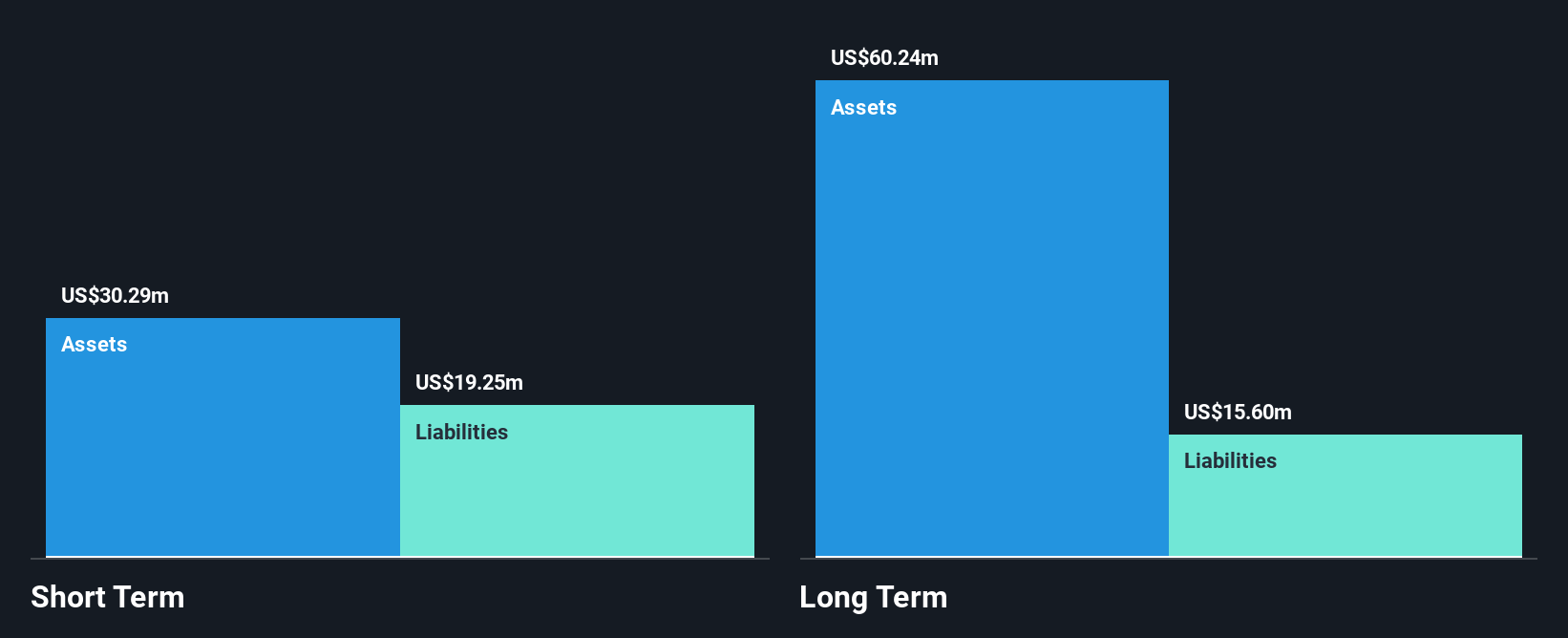

Arrow Exploration Corp., with a market cap of CA$61.46 million, showcases significant earnings growth, having increased by a very large amount over the past year. The company operates debt-free, alleviating concerns about interest coverage and financial leverage. Its short-term assets exceed both short and long-term liabilities, indicating sound liquidity management. Recent drilling activities in Colombia's Llanos Basin have shown promising hydrocarbon potential, though some wells were abandoned due to non-economic discoveries. Despite revenue declines in recent quarters, Arrow continues to expand its production capabilities with new wells expected online soon. Investors should note the company's high level of non-cash earnings when evaluating profitability metrics.

- Take a closer look at Arrow Exploration's potential here in our financial health report.

- Assess Arrow Exploration's future earnings estimates with our detailed growth reports.

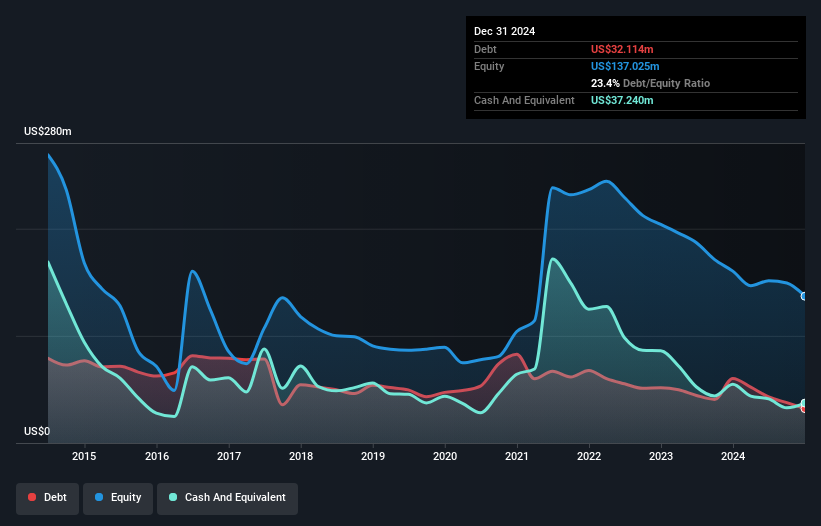

Westport Fuel Systems (TSX:WPRT)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: Westport Fuel Systems Inc. is involved in the engineering, manufacturing, and supplying of alternative fuel systems and components for transportation applications globally, with a market cap of CA$40.63 million.

Operations: The company's revenue is primarily derived from its Heavy-duty OEM segment, which generated $20.76 million, and its High-pressure Controls & Systems segment, contributing $7.38 million.

Market Cap: CA$40.63M

Westport Fuel Systems Inc., with a market cap of CA$40.63 million, is navigating challenges as it remains unprofitable and has seen increasing losses over recent years. Despite this, the company maintains strong liquidity, with short-term assets exceeding both short and long-term liabilities significantly. Recent developments include the launch of a new CNG solution for HPDI™ engines in collaboration with Volvo Group's joint venture Cespira, aiming to enhance heavy-duty truck performance while reducing emissions. Although Westport's revenue has declined sharply compared to last year, its cash runway suggests sustainability if current cash flow trends persist.

- Click here to discover the nuances of Westport Fuel Systems with our detailed analytical financial health report.

- Review our growth performance report to gain insights into Westport Fuel Systems' future.

Next Steps

- Investigate our full lineup of 402 TSX Penny Stocks right here.

- Ready For A Different Approach? Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About CNSX:PWR

Excellent balance sheet with slight risk.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k2.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

77 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

46 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

90 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

928 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative