Advertisement

- Canada

- /

- Oil and Gas

- /

- TSX:IPCO

Assessing International Petroleum (TSX:IPCO)’s Valuation After Its Newly Authorized Share Buyback Program

Simply Wall St

Reviewed by Simply Wall St

International Petroleum (TSX:IPCO) has launched a new share buyback, planning to repurchase and cancel up to about 6.5 million shares, roughly 6% of its float, over the next year.

See our latest analysis for International Petroleum.

The new buyback comes on top of a strong run. International Petroleum’s 30 day share price return of 10.04 percent has contributed to a 58.31 percent year to date gain and a 74.42 percent one year total shareholder return, suggesting momentum is still building as investors respond to its growth and capital return story.

If this kind of capital return story has your attention, it is also worth exploring fast growing stocks with high insider ownership for other fast growing companies where management has meaningful skin in the game.

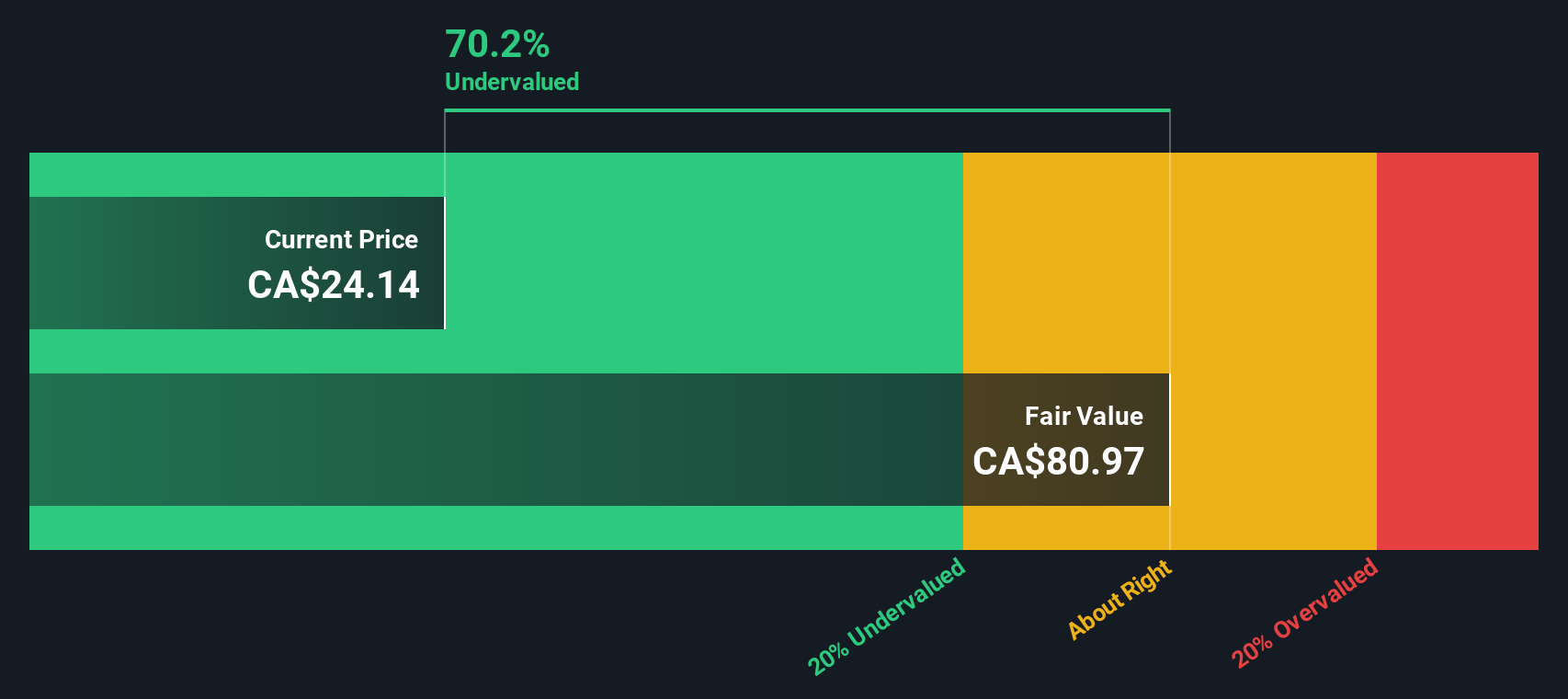

Yet with the share price already rallying hard and even trading above the average analyst target, the key question now is whether International Petroleum still looks undervalued or if the market is already pricing in its future growth.

Most Popular Narrative: 9.7% Overvalued

With the latest close above the narrative fair value estimate of CA$25.17, investors are weighing how much future growth is already in the price.

The analysts have a consensus price target of CA$24.946 for International Petroleum based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CA$28.03, and the most bearish reporting a price target of just CA$22.42.

Curious what kind of production ramp up, margin expansion and earnings jump would need to line up to support that outlook? The narrative reveals the full playbook.

Result: Fair Value of CA$25.17 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that optimistic playbook could yet be derailed by setbacks in executing Blackrod Phase 1 or by weaker oil prices that strain cash flows and reduce balance sheet flexibility.

Find out about the key risks to this International Petroleum narrative.

Another View: Cash Flows Tell a Different Story

While the consensus narrative now views International Petroleum as modestly overvalued, our DCF model presents a different perspective, with a fair value estimate of about CA$84.47 per share, which is roughly 67 percent above the current price. Could the market be underestimating Blackrod driven cash flows?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out International Petroleum for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 904 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own International Petroleum Narrative

If you see things differently or would rather dig into the numbers yourself, you can build a custom, data driven narrative in minutes, Do it your way.

A great starting point for your International Petroleum research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Before the next opportunity runs away from you, use Simply Wall Street’s powerful screener to identify stocks that align with your strategy, risk profile and return objectives.

- Focus on growing your capital by targeting high potential candidates using these 904 undervalued stocks based on cash flows that the market may not have fully priced in.

- Support long term income by reviewing these 15 dividend stocks with yields > 3% that combine consistent payouts with established underlying businesses.

- Consider positioning in emerging technology by scanning these 27 AI penny stocks involved in real world artificial intelligence adoption.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:IPCO

International Petroleum

Explores for, develops, and produces oil and gas.

High growth potential with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

67 followersusers have followed this narrative

7 commentsusers have commented on this narrative

20 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$123.9% undervalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

EN

Enemy on Halyk Bank of Kazakhstan ·

Halyk Bank of Kazakhstan will see revenue grow 11% as their future PE reaches 3.2x soon

Fair Value:US$52.2351.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IN

IncomeAssets on Magma Silver ·

Silver's Breakout to over $50US will make Magma’s future shine with drill sampling returning 115g/t Silver and 2.3 g/t Gold at its Peru Mine

Fair Value:CA$0.3534.3% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on SEGRO ·

SEGRO's Revenue to Rise 14.7% Amidst Optimistic Growth Plans

Fair Value:UK£9.3924.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

118 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

959 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

67 followersusers have followed this narrative

7 commentsusers have commented on this narrative

20 likesusers have liked this narrative