Advertisement

- Canada

- /

- Consumer Finance

- /

- TSX:GSY

Does goeasy (TSX:GSY) CEO Succession Reinforce Its Credit-Focused Strategy Or Hint At Change?

Simply Wall St

Reviewed by Sasha Jovanovic

- goeasy Ltd. has announced that CEO Dan Rees will step down on December 31, 2025, due to a blood disorder, with Patrick Ens, currently President of easyfinancial, set to become CEO on January 1, 2026, and Rees serving as Special Advisor until June 30, 2026.

- This leadership change brings an externally identified, high-potential successor with deep consumer lending experience from Capital One Canada and strong recent results at easyfinancial into the top role, signaling an emphasis on continuity and credit-focused execution.

- We’ll now examine how Patrick Ens’ appointment as CEO, following his tenure leading easyfinancial, could influence goeasy’s existing investment narrative.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 26 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

goeasy Investment Narrative Recap

To own goeasy, you need to believe its non prime and secured lending platform can keep growing despite tighter regulation, credit risk and funding constraints. The CEO transition to Patrick Ens, with Dan Rees staying on as Special Advisor into mid 2026, appears structured for continuity and does not materially change the near term focus on credit quality and regulatory risk, which remain the key catalyst and the biggest concern for shareholders.

Among recent announcements, the 25% dividend increase to an annualized CA$5.84 per share in February 2025 stands out in light of the CEO change. While the leadership transition shifts attention to governance and execution, the higher dividend underscores how important earnings resilience, credit performance and regulatory outcomes will be in supporting shareholder returns under the new CEO.

Yet, while the leadership handover looks orderly, investors should still be aware that rising allowances for credit losses could...

Read the full narrative on goeasy (it's free!)

goeasy's narrative projects CA$2.7 billion revenue and CA$476.3 million earnings by 2028. This requires 48.7% yearly revenue growth and an earnings increase of about CA$191.6 million from CA$284.7 million today.

Uncover how goeasy's forecasts yield a CA$203.40 fair value, a 65% upside to its current price.

Exploring Other Perspectives

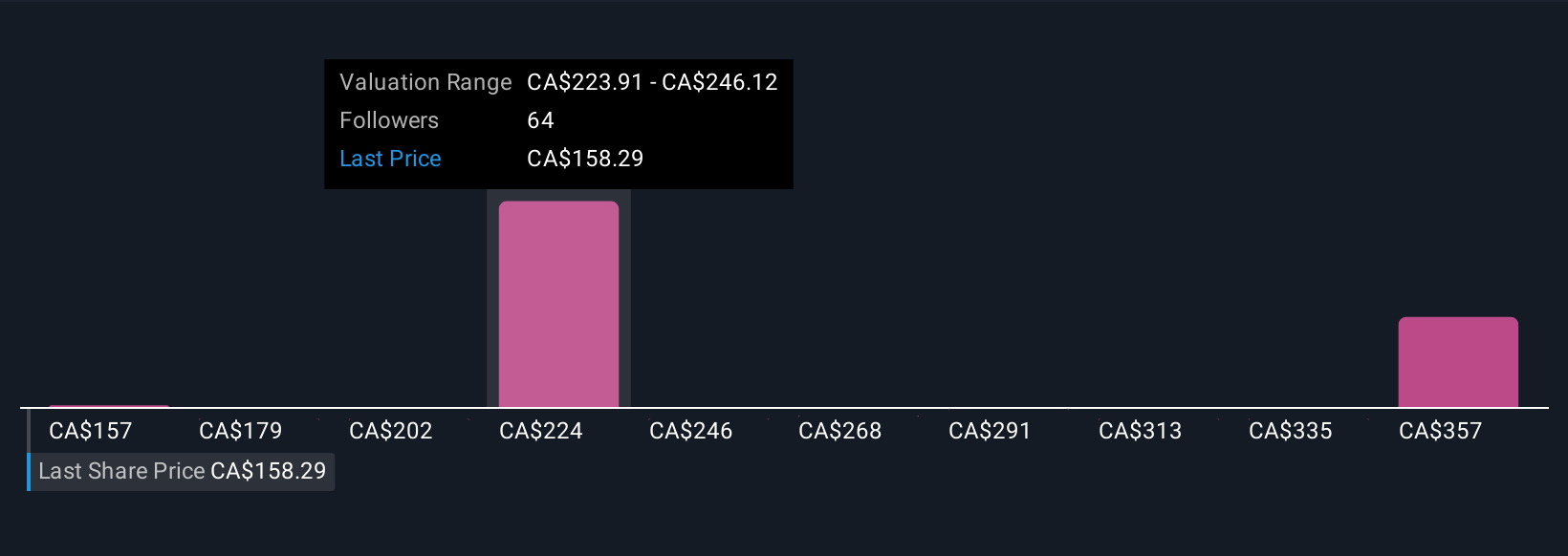

Twelve Simply Wall St Community valuations for goeasy range from CA$157.27 to CA$381.86, underscoring how far apart views on upside potential can be. When you weigh those against tightening regulatory rate caps and pressure on yields from a growing secured book, it becomes even more important to compare several perspectives before deciding how this business might fit in your portfolio.

Explore 12 other fair value estimates on goeasy - why the stock might be worth just CA$157.27!

Build Your Own goeasy Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your goeasy research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free goeasy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate goeasy's overall financial health at a glance.

No Opportunity In goeasy?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:GSY

goeasy

Provides non-prime leasing and lending services under the easyhome, easyfinancial, and LendCare brands to consumers in Canada.

Exceptional growth potential, undervalued and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

58 followersusers have followed this narrative

7 commentsusers have commented on this narrative

17 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

WO

woodworthfund on MGP Ingredients ·

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Fair Value:US$4035.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

davidlsander on Beam Therapeutics ·

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value:US$15081.9% undervalued

50 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

MO

mo7md on ADNOC Gas ·

ADNOC Gas future shines with a 21.4% revenue surge

Fair Value:د.إ3.728.9% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

117 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

959 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

58 followersusers have followed this narrative

7 commentsusers have commented on this narrative

17 likesusers have liked this narrative